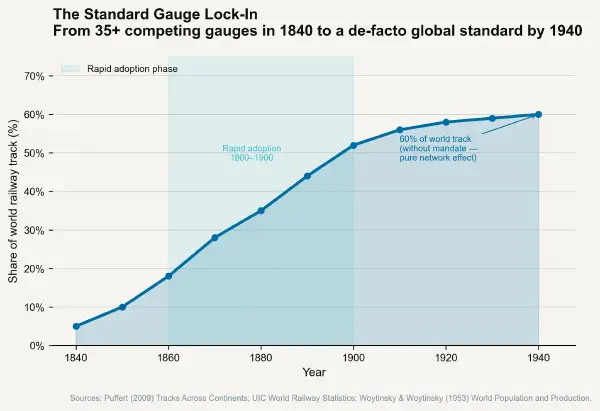

The Connector That Will Charge Everything#

In November 2022, Tesla announced that it would rename its proprietary charging connector standard the North American Charging Standard (NACS) and open it for adoption by third-party manufacturers. The announcement was strategically titled: by calling the standard NACS and submitting it to SAE International for formalisation as SAE J3400, Tesla simultaneously repositioned a proprietary connector (designed to serve Tesla vehicles exclusively on the Tesla Supercharger network) as an open technical standard positioned for universal adoption. In June 2023, Ford announced it would adopt NACS for its next-generation EVs. GM followed within a week. By the end of 2023, Rivian, Volvo, Polestar, Nissan, Honda, Toyota, and most other major North American EV manufacturers had announced NACS adoption.

The CCS (Combined Charging System) consortium — the incumbent standard backed by the SAE J1772 connector specification and adopted by every non-Tesla OEM in the prior generation — saw its standard rendered effectively obsolete for new North American vehicles in approximately 18 months. The European CCS standard (Combo 2) retains European regulatory backing and market position; the North American market has shifted to NACS in what is, in the language of standards economics, a complete standard displacement event.

Tesla’s SCI calculation from the NACS decision is instructional: by opening the connector specification while retaining ownership and operational control of the Supercharger network, Tesla converted a hardware lock (only Tesla cars use Tesla connectors as an original condition) into a network infrastructure position (all major North American EVs will use the Supercharger network, paying Tesla charging fees). The SCI of Supercharger network access is more valuable than the SCI of a connector patent, because network access fees are recurring operational revenue rather than one-time hardware royalties.

The Live Standards Competitions and Their SCI Stakes#

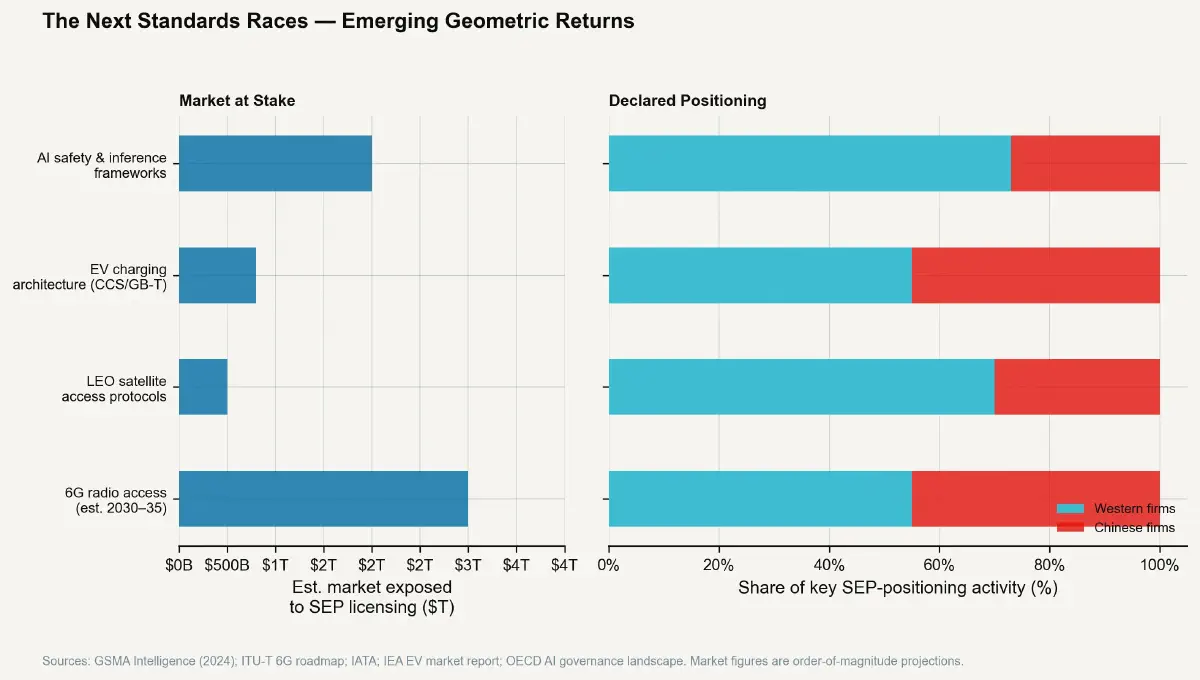

AI Safety and Evaluation Standards#

The most consequential live standards competition for SCI purposes may be one that is rarely described in patent terms: the emerging regulatory architecture for AI system evaluation, safety certification, and deployment authorisation. In the EU, the AI Act (adopted June 2024) establishes a risk-based regulatory framework that requires high-risk AI systems to undergo third-party conformity assessment — a process that requires demonstrable compliance with harmonised standards. The technical standards to which high-risk AI systems must conform have not yet been written. They are being developed by CEN-CENELEC (European standards body) and ISO/IEC JTC 1/SC 42 (the international AI standards committee).

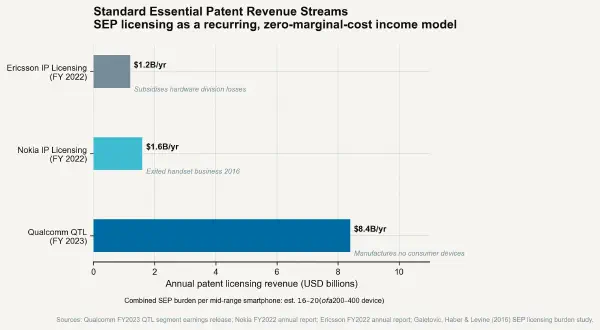

The SCI dynamics of AI safety standards are different from cellular SEP in structure but comparable in consequence. The AI standards process is not patent-mediated in the same way 5G NR is — the relevant standards are testing methodologies, evaluation benchmarks, and documentation requirements rather than technical implementation specifications. The SCI of participation in AI safety standards takes the form of first-mover regulatory intelligence, product certification cost advantages for companies whose development practices are aligned with standards they helped write, and — for testing and certification organisations — the creation of mandatory third-party certification markets in which certified evaluators extract fees from every compliant AI system deployment.

The NIST AI Risk Management Framework (AI RMF), published in January 2023, is the US government’s current contribution to AI safety standardisation. It is not a mandatory regulatory requirement but a voluntary framework with strong institutional adoption. Its categories and terminology are already migrating into regulatory use in federal procurement requirements and are likely to influence future mandatory regulatory frameworks. The organisations that have most actively engaged with NIST AI RMF development — through comment contributions, public workshops, and working group participation — are positioning themselves as the technical authorities who understand and can certify compliance with whatever regulatory regime emerges from the framework.

EV Charging Architecture: The Battle Continues Internationally#

The NACS displacement of CCS in North America does not represent a global resolution of the EV charging standards competition. In China, the GB/T charging standard — developed by the Standardisation Administration of China and adopted as mandatory for domestic EV charging — covers approximately 45% of the world’s EV fleet by unit count. The GB/T standard is incompatible with both CCS and NACS. Chinese EV manufacturers exporting to international markets (BYD, NIO, SAIC-MG) must accommodate the local charging standards of target markets, adding adapter or multi-standard capability costs to vehicles intended for export.

The International Electrotechnical Commission (IEC) has been working toward a globally harmonised EV charging connector standard (IEC 63110 for the communication protocol layer), but national and regional standards bodies have moved independently, and the GB/T installed base in China — serving a fleet of over 20 million BEVs and growing — creates a scale argument for GB/T adoption in markets where Chinese EVs are commercially significant. The SCI competition in EV charging architecture is not concluded; it is entering its international phase, and the outcome will determine charging network investment returns for the 2030s.

Satellite Communications and Spectrum Allocation#

Low-Earth-orbit (LEO) satellite communications — Starlink (SpaceX), OneWeb (Eutelsat), Amazon Kuiper, and various national equivalents — are competing for spectrum allocations, orbital slots, and inter-system interoperability protocols through the ITU (International Telecommunication Union) Radio Regulations process. Spectrum allocation is a standards process in the most literal sense: the ITU coordination and registration system determines which orbital slots and frequency bands a satellite system has priority rights over, and those rights, once established, persist for the duration of the system’s operational life.

SpaceX’s Starlink, which had filed ITU coordination requests for over 42,000 satellite positions across multiple orbital shells by 2023, holds one of the largest pending spectrum coordination positions in telecommunications history. The SCI equivalent for spectrum coordination is the lifetime value of exclusive or priority access to frequency bands in orbital slots whose capacity — for broadband provision to underserved markets, maritime and aviation connectivity, and direct-to-device cellular supplementation — is substantial. The ITU coordination process is not a patent competition; it is a priority queue, and Starlink’s aggressive filing strategy has occupied positions in ways that require later entrants to coordinate (and potentially defer) around existing registrations.

China’s national commercial satellite operator (China Satellite Network Group, incorporating the Musk-rival Guowang constellation) has filed ITU coordination requests for approximately 13,000 satellites in orbital shells designed in part to pre-empt Starlink expansion. The spectral and orbital coordination competition between Starlink and Guowang is being argued technically at the ITU level while being driven commercially and strategically by the same SCI logic that governs any standards race: the entity that secures priority coordination rights captures a perpetual operational advantage over later entrants.

Writing the Future Standard#

The consistent lesson across railroad gauges, USB-C, 5G NR, AI safety frameworks, EV charging, and LEO spectrum is that the highest-return engineering investment is presence at the table when the rule is being written, not excellence in building products that comply with the rule after it is written. The standard-essential patent position, the regulatory certification first-mover advantage, the spectrum coordination priority — each represents a conversion of early technical investment into a structural competitive position that is difficult or impossible for later entrants to replicate at the same cost, regardless of their technical quality.

The SCI is not a metric that rewards technical superiority. It rewards strategic timing, standards-body engagement, and the disciplined pursuit of intellectual property positions whose value is unlocked by the mandatory nature of compliance rather than the voluntary preference of customers. The firms that will dominate the AI era’s technology licensing landscape are not necessarily the firms building the most capable AI today. They are the firms drafting the technical requirements documents that will define what “capable” means for regulatory purposes — and lodging the patents that make compliance with those definitions mandatory.