The Vote That Was About Something Else#

In October 2016, at a 3GPP RAN1 #86 working group meeting in Lisbon, a technical working group voted on the coding scheme for the 5G NR (New Radio) control channel. The competing proposals were LDPC (Low-Density Parity-Check codes) and Polar codes. LDPC was backed primarily by Qualcomm, which held a substantial patent position in LDPC implementations. Polar codes were backed primarily by Huawei, which had made significant patent investments in Polar code algorithms since the 2010 disclosure of the Polar coding theoretical framework by Erdal Arıkan.

The working group adopted LDPC for the data channel and Polar codes for the control channel. The final vote was not a close technical call — the 3GPP body has formal procedures for resolving competing proposals through technical evaluation criteria. The outcome was a negotiated compromise that reflected not primarily the comparative technical merits of LDPC versus Polar codes (a question on which serious technical opinions diverged) but the political arithmetic of the voting blocs present in the room — where Chinese firms including Huawei, ZTE, and various Chinese operators held a meaningful fraction of the voting positions. The control channel Polar code adoption was a direct conversion of Huawei’s standards-body investment into a partial standard-essential patent position.

The Lisbon vote was significant less as a technical decision than as a demonstration that the 5G standards process was already a commercial and geopolitical competition whose outcomes were patent portfolios, not merely specifications.

The 5G SEP Race: Scale and Stakes#

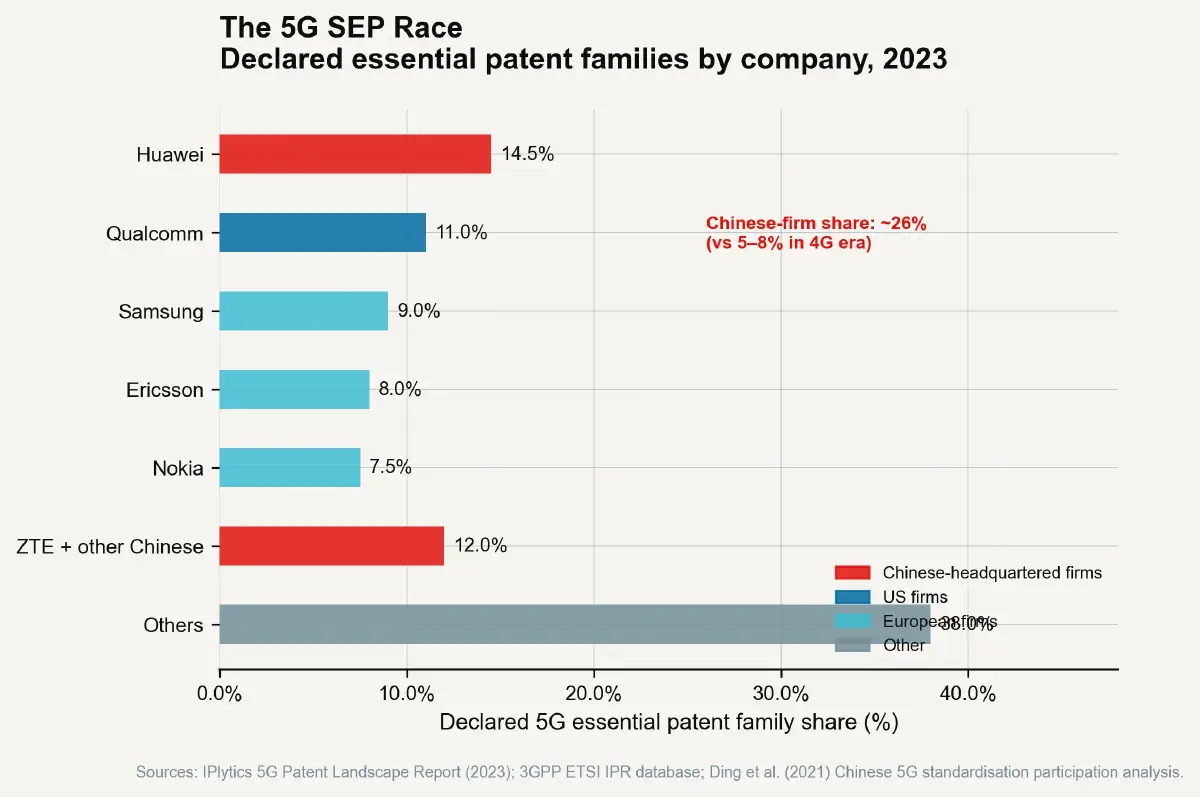

The International Telecommunication Union defines 5G specifications at the IMT-2020 level; the technical implementation is detailed at 3GPP, which produces the NR Release sequence (Release 15 through Release 18 current). The SEP declarations associated with 5G NR surpassed those of any prior wireless generation in declared volume. By 2023, IP analytics firm IPlytics had identified over 20,000 patent families declared essential to 5G NR standards, representing a total declared-essential volume approximately 3–4 times larger than 4G LTE at equivalent stages of the standards cycle.

The distribution of these declarations by firm is the scorecard of the 5G standards race:

- Huawei: approximately 14–15% of all 5G patent families declared essential (IPlytics, 2023 data), making it the largest single holder of declared-essential 5G patents.

- Qualcomm: approximately 10–12%, concentrated in the radio access layer where CDMA and LDPC heritage is strongest.

- Samsung: approximately 8–10%, reflecting aggressive 5G investment across antenna technology and encoding.

- Ericsson: approximately 8%, concentrated in radio access layer and scheduling algorithms.

- Nokia: approximately 7–8%, concentrated in radio access and network architecture layers.

- ZTE, OPPO, and other Chinese firms collectively: approximately 10–15% additional.

The Chinese firm aggregate — led by Huawei but substantial across multiple entities — represents a qualitative shift from the 4G era, when Chinese declared-essential shares were minimal. Between 4G and 5G, China’s declared SEP share in mobile standards increased from approximately 5–8% to approximately 25–30%. This shift is the direct product of a deliberate national strategy: China’s Made in China 2025 initiative and subsequent National Intellectual Property Strategy explicitly identified cellular standard-essential patent acquisition as a strategic objective, with state-funded research institutions and commercial firms aligned toward 3GPP participation as a priority.

The Geopolitics of Standards#

FRAND as a Competitive Weapon#

The FRAND obligation that governs all SEP licensing was designed as a floor for anti-competitive behaviour — a commitment that SEP holders will license their patents to any implementer at reasonable, non-discriminatory rates, preventing standard-essential monopoly leverage from blocking market entry. In the 5G era, FRAND has become a geopolitical instrument deployed by multiple state actors in different directions.

The US government’s export controls on Huawei, imposed from 2019 onward, prohibited US firms from supplying Huawei with semiconductor fabrication services, electronic design automation software, and (through foreign direct product rules) chips manufactured anywhere with US technology. These controls significantly impaired Huawei’s ability to manufacture its Kirin chipsets, reducing its mobile handset market share from approximately 20% globally in 2019 to under 5% by 2021. They did not, however, affect Huawei’s patent licensing revenues or its 3GPP participation. The SEP portfolio and the standards participation right are not subject to semiconductor export controls. Huawei continues to declare SEPs, continues to collect licensing revenues from the global 5G ecosystem, and continues to participate in 6G standards working groups — activities that a chip supply chain export control cannot reach by design.

The European approach to Huawei SEP licensing has been more contested. A series of FRAND determination cases — most notably the German court rulings in Huawei v. ZTE (European Court of Justice, 2015) and subsequent national implementations — established that SEP holders may seek injunctions against standard implementers who refuse to negotiate FRAND licenses in good faith, but cannot seek injunctions against good-faith licensees who contest the royalty rate. The practical effect has been to produce a negotiation regime where Huawei’s licensees pay royalties into escrow while rate disputes are litigated — a regime that validates Huawei SEP licensing as a revenue-generating activity independent of US restrictions on its hardware business.

China has pursued a parallel strategy through the standard-setting process itself. China’s MIIT (Ministry of Industry and Information Technology) has promoted homegrown standards — including IMT-2020 5G specifications with differentiated technical parameters for domestic deployment — and has encouraged Chinese firms to develop standards for markets where Western and US influence is limited. The Chinese-developed NB-IoT (Narrowband Internet of Things) standard, standardised through 3GPP but with foundational contributions from Chinese firms and extensive Chinese deployment, represents an early success in this approach.

The BRI Standards Corridor#

China’s Belt and Road Initiative has acquired a secondary dimension in standards policy. In markets where BRI infrastructure investment is substantial — sub-Saharan Africa, Southeast Asia, Central Asia, parts of Latin America — Chinese equipment suppliers (Huawei, ZTE) have deployed 4G and 5G infrastructure that is optimised for Chinese-origin standards implementations. Network management systems, operations and maintenance interfaces, and equipment software stacks in BRI-recipient networks are substantially Chinese technology. The technical dependency created by Chinese equipment deployment creates a path dependency on Chinese-origin standard extensions and feature sets in future generations.

This is the standards strategy applied at infrastructure level: use equipment supply relationships to create installed-base commitments to proprietary technical approaches, then standardise those approaches through the bodies where your participation is now significant. The SCI calculation extends beyond patent royalties to the competitive advantages in future equipment bids that standard familiarity creates.

The Practical SCI Outcome for 5G#

The SCI implications of the 5G SEP distribution are significant for three different actors.

For Western SEP incumbents (Qualcomm, Ericsson, Nokia), the 5G SEP landscape is substantially less favourable than 4G: their cumulative share of essential patents is lower, the absolute royalty pool is distributed across a larger number of significant holders, and the FRAND rate determination for 5G has become more contentious as Huawei and Chinese firms press their licensing claims with increasing legal sophistication. The expected SCI for a Western 5G SEP portfolio is lower than the historical SCI of their 4G portfolios, though still positive.

For Huawei specifically, the 5G SEP portfolio represents a hedge against the hardware business constraints imposed by export controls — a licensing revenue stream that is structurally uncorrelated with the semiconductor supply chain restrictions. This was almost certainly a deliberate strategic calculation: building an SEP position creates durable revenue that cannot be export-controlled.

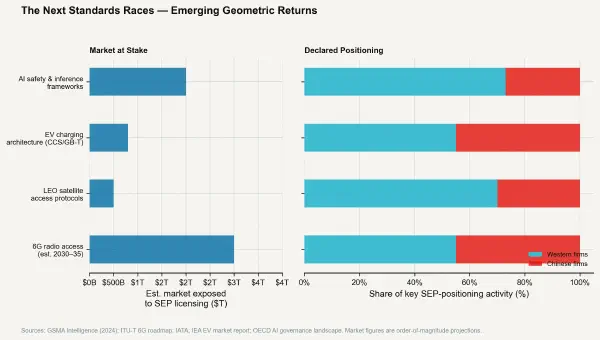

The next post examines the next generation of standards competitions — AI safety frameworks, EV charging architecture, and satellite spectrum allocation — where the SCI outcomes are not yet determined, and where the decisions being made in 2024–2026 will govern the next decade of technology licensing revenue.