The Royalty That Outlives the Patent#

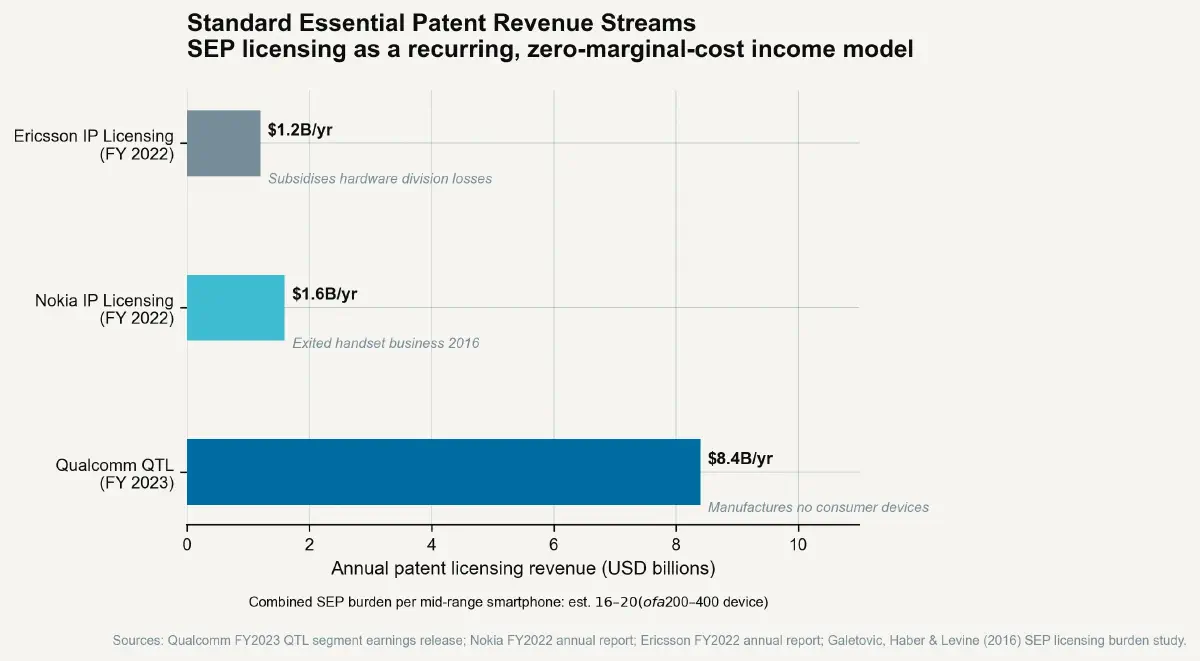

In 1999, Qualcomm Incorporated reported total revenue of approximately $3.3 billion. In fiscal year 2023, Qualcomm reported total revenue of approximately $35.8 billion — of which approximately $8.4 billion came from its Qualcomm Technology Licensing (QTL) division. QTL does not manufacture chips. It does not design handsets. It does not operate cellular networks. It holds patents that are standard-essential for building any 3G, 4G, or 5G cellular device, and it licenses those patents to every manufacturer of any such device sold anywhere in the world. The approximately $8.4 billion represents royalties paid by Apple, Samsung, Xiaomi, OPPO, Vivo, and essentially every consumer electronics company with a cellular radio in its product portfolio — regardless of whether those products contain a single Qualcomm chip.

The QTL revenue stream is the highest-resolution observable specimen of what the Standard Capture Index measures. Qualcomm’s cellular SEP position was built through active participation in 3GPP standards bodies during the WCDMA (3G) and LTE (4G) standardisation processes of the late 1990s and early 2000s. The technical contributions that became mandatory for standard compliance were submitted to ETSI with declarations of essentiality. The royalty rates that followed from those declarations — contested, litigated, renegotiated, and re-litigated — ultimately settled into a global licensing regime that generates revenues exceeding the annual GDP of many national economies, from patents whose core inventions are now two decades old.

The SEP Architecture#

What Makes a Patent Standard-Essential#

A patent is standard-essential if it is impossible to implement a technical standard without infringing the patent’s claims. The determination of essentiality is made initially by the patent holder, who self-declares essentiality to the relevant standards body (ETSI for European telecommunications standards, IEEE for Wi-Fi and Ethernet standards, ITU for certain international telecommunications standards). Standards bodies do not independently verify essentiality declarations — they require only that the declaring entity commit to licensing the declared SEP on FRAND (Fair, Reasonable, and Non-Discriminatory) terms.

This self-declaration architecture has predictable consequences. Studies by major patent analytics firms — including an IHS Markit analysis of 5G SEP declarations — have consistently found that 40–60% of patents declared essential to a major wireless standard are, upon detailed independent technical analysis, not actually essential to the standard. A patent declared essential may read on an optional feature of the standard, describe an implementation approach that is not the only approach taken by compliant devices, or have claim language sufficiently general that its essentiality depends on claim interpretation — a question ultimately resolved in litigation, not by the standards body.

The overstatement of essentiality has strategic value. A large declared SEP portfolio signals technical leadership in the standard and strengthens licensing negotiating positions. Patent holders with large declared-essential portfolios can credibly threaten infringement actions that are expensive to defend even when the specific patents in suit are marginally essential. The FRAND commitment, which requires good-faith licensing at reasonable rates, does not prevent litigation — it provides a defence to injunction claims, but the definition of what rate is “reasonable” under FRAND has been under active litigation across US, European, and Asian courts for twenty years without producing a consistent global answer.

The FRAND Ambiguity Machine#

FRAND licensing, intended to balance the SEP holder’s right to reward for technical contribution against the standard implementers’ right to access mandatory technology at proportionate cost, has instead become one of the most expensive ongoing commercial disputes in global intellectual property law. The absence of a defined methodology for calculating a FRAND rate — in contrast to, say, the compulsory licensing rates established under pharmaceutical patent law — has created space for SEP holders to pursue royalty rates significantly above any reasonable estimate of their patents’ proportionate contribution to a standard’s value, while implementers pursue rates below what is required to sustain investment in future standards participation.

The cumulative royalty burden on a global smartphone is instructive. A study by Galetovic, Haber, and Zaretzki (2016) estimated the aggregate SEP royalty burden on a mid-range 4G smartphone at approximately $16–20 per unit, shared across all cellular SEP holders. Another study by RPX Corporation estimated the total licensing burden (including non-SEP patent royalties) on a mid-range Android smartphone at $30–50 per unit. On a device that retails for $300–400, 10–15% of the sale price flows to patent licensing fees. The consumer pays for patents most of them have never heard of, held by firms whose names do not appear anywhere on the device.

For a tier-one smartphone OEM selling 200 million units per year at mid-range price points, the licensing cost of cellular SEPs alone runs to $4–10 billion annually. This is the mandatory cost of participating in a communications standard. It does not correspond to a new product, a new capability, or a new service. It is the annual payment to entities that were present at the standards table decades ago and lodged patents at the right moment.

The SCI in Practice: Numerical Illustration#

Qualcomm’s QTL division provides the most transparent public data available for SCI calculation. The cumulative R&D investment that produced Qualcomm’s cellular SEP portfolio — spanning from CDMA development in the 1980s through active 5G standards participation — can be approximated from the company’s R&D expenditure disclosures. Qualcomm’s total reported R&D expenditure from 1999 to 2023 was approximately $62 billion, but this includes substantial investment in chip design (QCT — Qualcomm CDMA Technologies), which is attributable to product development rather than standards positioning. The standards-participation and patent prosecution investment attributable specifically to SEP generation is a fraction of total R&D — industry analysts typically estimate 15–20% of semiconductor R&D as standards-directed.

Using a conservative allocation of $10–15 billion in cumulative SEP-generating R&D against annual QTL revenues of $8–9 billion, the SCI for Qualcomm’s cellular SEP portfolio exceeds 0.5 — meaning the annual return from the licensing investment is more than 50% of the total investment made, recurring annually, indefinitely. No comparable return profile exists in manufacturing capital investment, commercial real estate, or financial instruments at equivalent scale. The SCI of successful SEP positions is structurally superior to any alternative deployment of similar research capital, which is why firms with the size and standards-body access to pursue them do so as a primary strategic objective.

Nokia, Ericsson, and the SEP Industry#

Qualcomm’s licensing model is the most discussed, but it is not unique. Nokia — which exited the mobile handset manufacturing business entirely in 2016 when it sold the remnant of its handset operation to HMD Global — retained its full patent portfolio, including thousands of declared-standard-essential patents in 2G, 3G, 4G, and 5G. Nokia’s patent licensing revenue in 2022 was approximately $1.6 billion — generated by a company that manufactures no consumer devices. The Nokia patent portfolio is, in effect, the residual asset of a mobile industry pioneer that has been converted into a permanent licensing stream.

Ericsson, which remains an active telecommunications equipment manufacturer, generated approximately $1.2 billion in intellectual property revenues in 2022 — a contribution to total group revenues that significantly exceeds the profitability of its network equipment divisions in markets facing price pressure from Huawei. The IP revenue stream, generated by historical SEP positions in 4G and 5G, subsidises competitive equipment pricing in a market where the company would otherwise struggle to match the cost structure of state-supported competition.

The structural implication is that the SCI calculation is not merely a retrospective valuation exercise. It is a forward-looking R&D allocation guide: for companies with standards-body participation capability, investment in 6G standards positioning beginning now will determine licensing revenues for the 2030s and 2040s. The ante to secure that position is technical credibility, active 3GPP participation, and a disciplined patent prosecution strategy — a cost measured in hundreds of millions of dollars and years of engineering talent commitment. The return, for the winners, is perpetual. The next post examines the 5G standards competition as a live geopolitical contest, and what Huawei’s strategy reveals about the SCI stakes for the next generation of wireless standards.