The Width of a Horse#

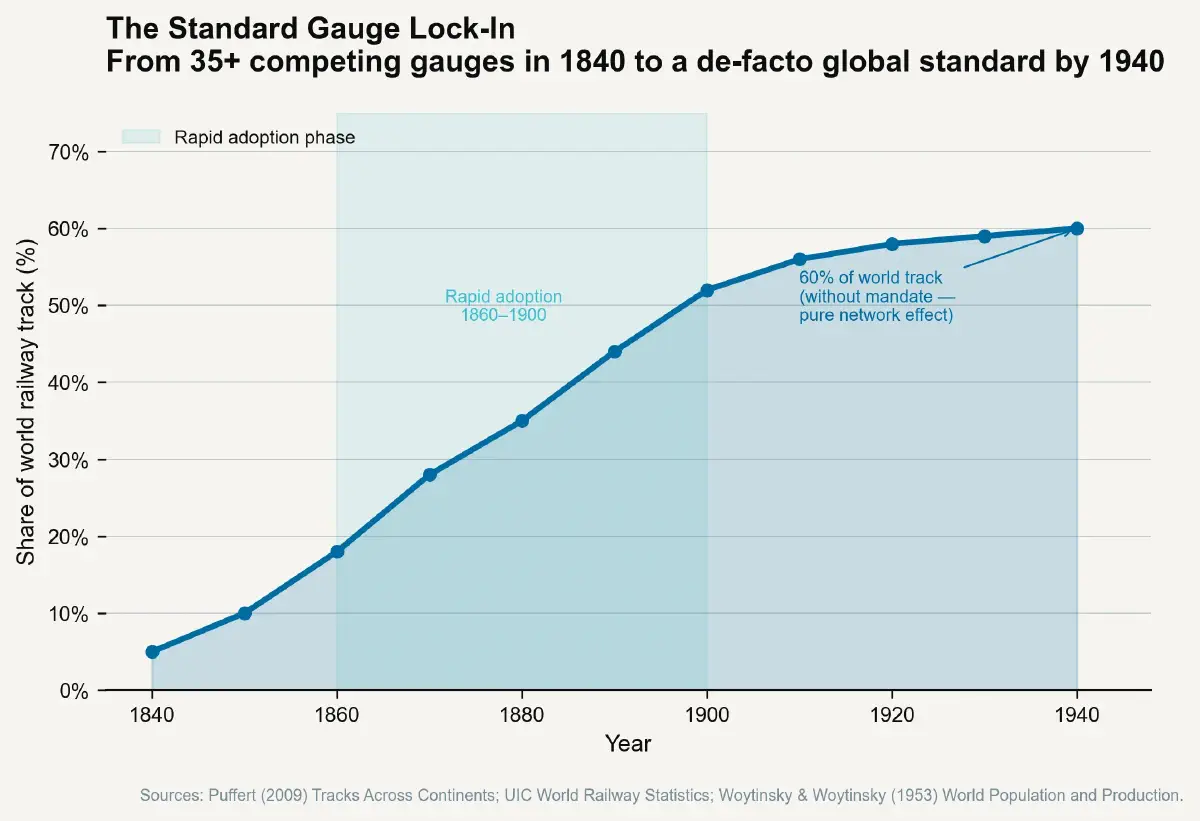

In 1830, the Stockton and Darlington Railway — generally considered the first public steam railway — operated its locomotives on tracks with a gauge of 4 feet and 8.5 inches between the rails. This measurement was not derived from any theoretical analysis of optimal track geometry. It was adopted because the wagons of the collieries in northeast England that the railway served had been built to fit horse-drawn tramway ruts of approximately that width, and those ruts had been worn into road surfaces by Roman carts whose wheel spacing was determined by the width of two horses harnessed side by side. George Stephenson used the same gauge for later railways, including the Liverpool and Manchester, and when Stephenson’s locomotives became the dominant commercial product of early British railway expansion, 4 feet 8.5 inches propagated across the British network, then across British colonial railways worldwide, then — through rail technology transfer — into the United States, Canada, and large parts of continental Europe.

By 1880, the world had approximately 35 distinct rail gauges in use across different national networks. By 1940, the standard gauge of 4'8.5" accounted for approximately 60% of all track worldwide — not because it was the optimal theoretical gauge for freight capacity and speed (5'3" or wider gauges have superior stability and freight volume properties), but because the historical weight of prior decisions, the interoperability costs of gauge changes at junctions, and the capital commitments of existing rolling stock made conversion prohibitively expensive. The standard won not through technical superiority but through adoption momentum. The SCI of the historical standard-gauge decision was effectively infinite: the economic value of not being the odd gauge out — of having your rolling stock operate on most of the world’s track — compounded over 175 years of global rail freight.

The Lock-In Mechanism Is Always the Same#

The standard gauge story contains every element of the lock-in mechanism that governs standards competition in every subsequent technology domain. First, an early technical decision — made for reasons of convenience, compatibility with prior art, or commercial availability rather than technical optimality — establishes a baseline. Second, a network of complementary investments (rolling stock, stations, bridges, maintenance workshops) is built to that baseline. Third, the cost of switching from the established baseline becomes a function of all those complementary investments, not merely the direct cost of changing the nominal parameter. Fourth, the entity whose technology definition becomes the baseline extracts economic benefit proportional to the size of the network built around it — what economists call network externalities.

The 20th and 21st centuries have replicated this structure at shorter time scales and higher economic intensity across every technology platform. The IBM PC architecture became a standard in 1981 — not because it was technically superior to the Apple II or the CP/M ecosystem, but because IBM’s brand credibility led corporate buyers to adopt it, and the decision to use third-party components with published specifications enabled compatible clone manufacturers to lower prices and expand the installed base faster than any vertically integrated competitor could. The SCI for Intel’s x86 instruction set architecture and Microsoft’s DOS/Windows operating systems — the two firms whose technologies became mandatory components of every IBM-compatible PC — is measurable in trillions of dollars of cumulative licensing and product revenue.

The Standard Capture Index as a Measurement Tool#

The Standard Capture Index (SCI) is defined as the annual economic value of licensing fees that are mandatory for compliance with a standard — Standard-Essential Patent (SEP) royalties — divided by the total investment required to achieve the SEP position that generates them. It is not a perfect metric: the denominator includes R&D investment whose purpose was not solely standard capture, and the numerator is contested in FRAND litigation across every major technology market. But as an approximation of the return on investment from standards participation, it reveals a consistent pattern: the SCI of successful standard-essential patent portfolios is among the highest in any investment category in the technology industry.

The calculation requires understanding two components: what makes a patent standard-essential, and what determines the licensing revenue from SEP ownership.

A standard-essential patent is a patent that covers technology whose implementation is mandatory for compliance with a technical standard. If a wireless device must implement the 5G NR (New Radio) standard to use 5G networks, and if a 5G NR transmitter cannot be built without practising a particular patent’s claims, that patent is standard-essential. The SEP’s owner may then license it to every manufacturer of 5G devices — which is, in 2024, every mobile phone manufacturer, every wireless module maker, every automotive OEM installing connected telematics systems, and a rapidly expanding set of IoT device manufacturers. The licensor does not manufacture anything. It charges a royalty on the commercial value of everyone else’s manufacturing.

From Telegraph to Wi-Fi: The Persistent Structure#

The telegraph standard battles of the 1850s–1880s — particularly the competition between American telegraph companies over pole-line routing rights and interconnect pricing — established legal frameworks for standardised interconnect compensation that directly influenced the telephony interconnect regimes of the 20th century. When AT&T’s Bell System held a near-monopoly on US telephone infrastructure from the 1870s through the 1984 divestiture, the economic structure was essentially an SCI calculation: Bell’s basic telephony patents expired in 1893-94, triggering an explosion of competitive local phone companies; but AT&T retained control of the long-distance interconnect, forcing all local carriers to pay access fees for long-distance call completion. The standard for long-distance interconnect was AT&T’s network, and the mandatory nature of using that network generated regulated revenue until 1984.

The modern wireless era has compressed these dynamics significantly. The 2G GSM standard, finalised in 1990–1991, created the first large-scale SEP portfolio competition in mobile communications. Ericsson and Nokia — both participants in the GSM standards body (ETSI — European Telecommunications Standards Institute) — built patent positions in GSM encoding and radio access technology. When GSM became the dominant global cellular standard, their SEP portfolios generated licensing revenues that subsidised a generation of R&D investment. Qualcomm, which held a smaller position in GSM but a dominant position in the competing CDMA standard through US carrier deployment, applied its understanding of SEP economics to invest heavily in 3G WCDMA standardisation. The 3G standard incorporated CDMA technology at the radio access layer — a decision that gave Qualcomm’s patents standard-essential status in every 3G device manufactured worldwide.

USB-C and the Modern Standard Tax#

The USB-C connector standard, mandated by the European Union for all consumer electronics sold in EU markets from 2024–2026, represents the most recent large-scale government intervention into standards competition. The EU’s motivation was consumer interoperability and reduction of electronic waste — charger standardisation reduces the volume of redundant charging accessories disposed of annually. The consequential side effect of the USB-C mandate is that it has designated a specific connector specification as mandatory for EU market access, and the intellectual property embedded in that specification is owned by the USB Implementers Forum — a consortium including Apple, Intel, Microsoft, HP, and others.

The USB-C mandate is, in SCI terms, a government-administered standard capture event. But the analysis is more complex than the cellular SEP case, because the USB-IF licensing model for USB-C is royalty-free for certified implementers. The economic benefit of USB-C standardisation flows primarily to companies whose broader product ecosystems benefit from USB-C adoption — accessory manufacturers, charger manufacturers, cable manufacturers who can now sell one product into the entire market rather than maintaining separate product lines for different connector standards.

Apple’s resistance to the USB-C transition from Lightning — ultimately overridden by EU regulation — was itself a SCI calculation: Lightning was Apple’s proprietary standard, and every iPhone accessory manufacturer in the world paid Apple certification fees and sourcing requirements. Apple’s Lightning SCI was positive and sustainable as long as its installed base was large enough to make Lightning certification economically rational. The EU mandate terminated that calculation by making Lightning non-compliant with EU market access requirements.

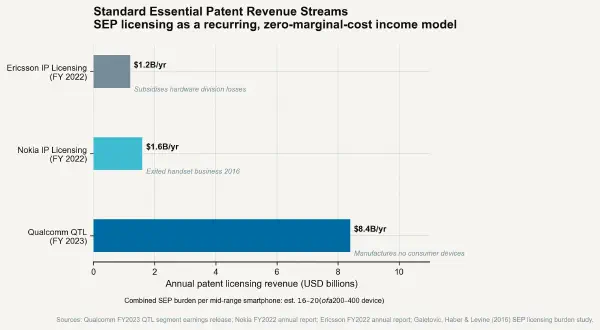

The standard bearer in the railroad era won by getting there first and making switching too expensive. The standard bearer in the wireless era wins by embedding patents in the standard before ratification. The standard bearer in the USB era lost to regulation. The mechanism differs; the economic logic is unchanged. The next post examines where the largest current SCI positions sit — and how $8 billion per year in annual royalties can flow from a patent position created 20 years ago.