The room where the negotiation happened#

On February 28, 2022, the fifth session of the United Nations Environment Assembly (UNEA-5.2) adopted Resolution 5/14, mandating the development of a legally binding international agreement on plastic pollution by the end of 2024. The resolution passed by consensus — an unusually strong mandate for an international environmental negotiation — following pressure from a High Ambition Coalition of approximately 90 countries led by Norway and Rwanda and subsequently joined by the EU. The coalition had entered the session demanding a treaty; they left with a mandate. The mandate was the easy part.

The Intergovernmental Negotiating Committee (INC) convened for its first session in Punta del Este, Uruguay, in November 2022 — three hundred delegates from member states, flanked by observers from industry associations (the Global Partners for Plastics Circularity, representing major plastic producers and packaged goods brands), environmental NGOs, and scientific advisory bodies. The political geography was immediately apparent: on one side, the High Ambition Coalition advocating for a "full lifecycle" treaty that would address plastic production volumes; on the other, an oil-producing country bloc — Russia, Saudi Arabia, Iran, and several Gulf states — insisting that the treaty mandate refer exclusively to waste management and recycling, not production caps.

This fault line is the political expression of the Plastic Cost Coverage Ratio. A waste-management-only treaty would not change the numerator of the PCCR — total plastic production would continue at current or higher levels. It would at best improve waste collection infrastructure in the countries with lowest collection rates, reducing some fraction of ocean input while leaving the full external cost of production unaddressed. A production-side treaty that mandated reductions in virgin plastic production would directly constrain the upstream source of the PCCR's denominator, reducing both external costs and the denominator more quickly.

The policy arsenal that already exists#

Before the Global Plastics Treaty, a set of national and regional policy instruments had already begun to raise the PCCR from its floor of essentially zero. Their geographic scope, their ambition level, and their effectiveness in actually changing the Plastic Cost Coverage Ratio vary significantly:

The EU Plastics Strategy, launched in January 2018, is the most comprehensive existing policy framework for plastics. Its elements include: a ban on single-use plastics with freely available alternatives (implemented in 2021, covering items such as cotton bud sticks, straws, cutlery, and expanded polystyrene food containers); mandatory recycled content requirements for beverage bottles (25% by 2025 for PET bottles, 30% by 2030 for all plastic bottles); deposit-return scheme requirements for beverage containers to be operational across all member states by 2029; and a packaging levy starting at $0.80/kg on non-recycled plastic packaging waste under the EU budget mechanism (essentially shifting a portion of the external cost to member states, which in turn pass it to the packaging industry).

The combined effect of these measures, when fully implemented, is to raise the PCCR for plastic packaging in the EU from approximately 0.02–0.04 toward an estimated 0.08–0.12 — still below the full external cost, but a meaningful improvement that demonstrates the policy mechanism is functional. The key unresolved limitation of the EU approach is that it applies only to plastic placed on the EU market; it does not apply to plastic produced in the EU for export, and it does not address the health externality component beyond the ocean damage cost.

The EPR landscape#

Extended Producer Responsibility for plastic packaging is now mandatory in approximately 40 countries, up from approximately 18 countries in 2018. The EPR systems vary enormously in design, ambition, and effectiveness. The highest-functioning systems — the German Grüner Punkt (Green Dot) system, the French filière emballages, and the Belgian Fost-Plus scheme — require producers to join producer responsibility organisations, pay fees proportional to the packaging they place on the market, and fund post-consumer collection and recycling at rates that approach the cost of operating those services.

The limitation of current EPR systems is that they fund waste management costs — the cost of collecting and recycling or disposing of the packaging — not the full external cost. The difference is significant: the cost of operating a kerbside collection and recycling system for plastic packaging in a European city is approximately $50–150/tonne. The external cost of plastic pollution per tonne produced is, on OECD estimates, approximately $300–400+/tonne, of which waste management costs represent perhaps 10–15%. A fees-covering-collection-costs EPR system captures a PCCR of approximately 0.05–0.08, not the 0.80–1.0 required for full cost internalisation.

The step from collection-cost recovery to full-externality recovery requires extending the EPR fee to include ocean damage, health cost, carbon externality, and ecological service loss — cost categories that EPR schemes do not currently calculate or charge. Doing so is technically possible; it is politically opposed by the industry associations that negotiate EPR standards in most jurisdictions.

The Global Plastics Treaty endgame#

By INC-5 in Busan, South Korea in November 2024 — the session that was supposed to finalise the treaty — consensus had not been reached on the critical production-side measures. The High Ambition Coalition's draft text included: mandatory reductions in primary plastic polymer production over a defined timeframe; mandatory elimination of "problematic" polymer-chemical combinations (additives with known endocrine-disrupting or carcinogenic profiles); mandatory full-lifecycle EPR schemes in all signatory states; and a financial mechanism to fund waste infrastructure in lower-income countries.

The producing-country bloc's counter-position rejected production caps entirely, proposing instead a treaty focused on waste collection infrastructure, sustainable materials management standards, and voluntary targets for recyclability. The gap between these positions defined whether the treaty would change the PCCR's denominator (by capping the volume of external cost produced) or attempt modestly to improve the numerator (by funding waste collection in countries where it is lowest).

Several middle positions were under active negotiation: a phased production cap with differentiated timescales for developed and developing economies, modelled on the HCFC phase-out under the Montreal Protocol; sector-specific targets for single-use plastic categories rather than aggregate production limits; and a "chemicals of concern" annexe that would standardise the phaseout of specific high-risk additives independent of polymer production level.

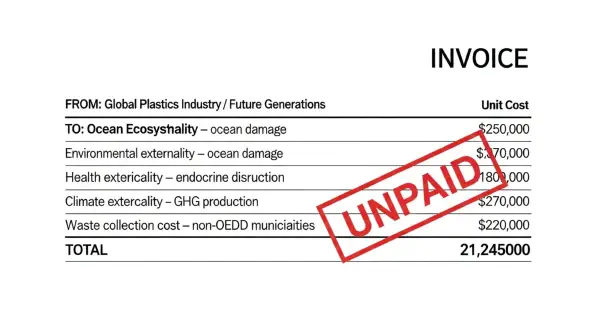

The arithmetic of who benefits from delay#

The delay in the Global Plastics Treaty is economically rational from the perspective of the actors who benefit from the current PCCR. The petrochemical sector's planned capacity expansion for plastic production between 2020 and 2030 represents approximately $300 billion in capital investment, predicated on continued growth in plastic demand. A production-cap treaty that reduces the volume of plastic produced reduces the revenue from that capital investment in direct proportion. The incentive to delay, weaken, or eliminate production-cap provisions is financially straightforward.

The incentive from the other side of the ratio is equally straightforward but structurally different. The external cost is borne by parties who are not in the negotiating room: marine ecosystems, future generations of children exposed to endocrine-disrupting additives, coastal communities whose fisheries are contaminated, and the 2 billion people who lack reliable access to waste collection and therefore serve as the default disposal system for plastic produced elsewhere in the global supply chain. These parties' interests are represented by NGO observers at the INC — not by delegations with legal standing to block consensus.

The Plastic Cost Coverage Ratio, like the Ocean's Marine Extraction Ratio and nuclear power's Lifetime Risk-Adjusted Carbon Score, is ultimately a diagnostic of a governance failure rather than a technical problem. The technology to reduce plastic production, improve its recyclability, eliminate its most hazardous additives, and fund post-consumer collection infrastructure in the most underserved markets exists and is commercially deployable. The barrier is not technological capacity — it is the allocation of costs that are currently externalised to the environment, future generations, and the world's poorest communities. The Global Plastics Treaty, whatever its final form, will determine for the next generation whether that allocation begins to be corrected.