A framework built in one weekend#

In December 2022, delegates from 188 countries gathered in Montreal, Canada, for COP15 — the fifteenth meeting of the Conference of the Parties to the Convention on Biological Diversity. The negotiations had been delayed two years by the COVID-19 pandemic and moved from Kunming, China (which remained the nominal host) to Montreal at the last minute due to visa complications. What emerged at 3:15 am on December 19, 2022, after a 48-hour final negotiating session, was the Kunming-Montreal Global Biodiversity Framework: a 23-target framework that included, as its headline commitment, a binding pledge to protect 30% of the world's land and ocean areas by 2030.

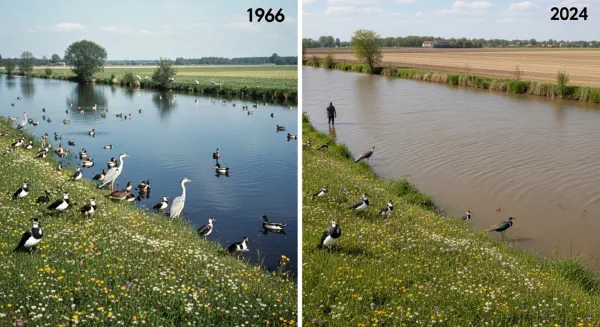

The 30×30 commitment is the most ambitious protected area expansion in the history of international conservation. From a starting point of approximately 17% of land and 8% of ocean under some form of protection in 2022, reaching 30×30 requires protecting an additional area roughly equivalent to two Australias. The financial requirement estimated in a 2020 analysis commissioned by the Campaign for Nature — led by Waldron and colleagues using systematic habitat priority mapping — was approximately $140–175 billion per year for effective protected area management globally. The current investment level was approximately $20–25 billion per year.

The gap between what was committed and what was financed was approximately $115–150 billion per year. The final GBF text included a commitment to "mobilise at least $200 billion per year from domestic and international sources for biodiversity by 2030," including a commitment to increase international biodiversity finance to developing countries to at least $20 billion per year by 2025 and $30 billion by 2030. Neither commitment was binding in the treaty law sense, and neither has a clear accountability mechanism.

The architecture of a solution#

The GBF's financial framework sits within a broader architecture of biodiversity finance mechanisms that has been under development for approximately three decades. The Ecosystem Dependency Ratio provides a diagnostic framework for evaluating whether this architecture is addressing the gap between what the economy extracts from natural systems and what it invests in their maintenance. The current architecture has several components:

Public protected area budgets represent the largest current flow of biodiversity finance — approximately $20–25 billion per year globally, managed through national protected area networks, national parks budgets, and conservation agencies. These budgets have in most countries been flat or declining in real terms over the period when the GBF's targets were being developed, while the protected area estate being managed expanded.

Development aid with biodiversity objectives flows through multilateral development banks, bilateral aid agencies, and the Global Environment Facility (GEF, the principal multilateral fund for biodiversity finance). The GEF has distributed approximately $21.5 billion in grants since 1991, leveraging $117 billion in co-financing — meaningful but small relative to the identified need. The GBF established a new Global Biodiversity Framework Fund (GBFF) administered through the GEF; its capitalisation at launch was approximately $245 million — less than 0.2% of the annual gap it is designed to help address.

Biodiversity offsets — the mechanism by which development projects pay for conservation activities measured to compensate for the biodiversity damage of the project — have grown significantly in regulated contexts, particularly for infrastructure projects in Europe, Australia, and the US (under federal mitigation banking rules). The global biodiversity offset market was estimated at approximately $6–9 billion per year by the Business and Biodiversity Offsets Programme. The environmental effectiveness of offsets is contested in the academic literature: if offsets do not achieve genuine "no net loss" of biodiversity value, they provide a finance mechanism without delivering the conservation outcome that justifies the mechanism.

Debt-for-nature swaps: the Ecuador case#

Debt-for-nature swaps — the conversion of sovereign debt into conservation commitments — represent one of the most significant innovations in conservation finance in the 2020s. The mechanism: a country with outstanding foreign debt negotiates a partial debt cancellation with its creditors; in exchange, it commits to directing the reduced debt service payments into domestic conservation programmes. The arrangement reduces the sovereign's financial burden while directing funds toward biodiversity conservation; the creditor may accept a haircut on the debt principal but receives a financial instrument linked to a conservation outcome.

In May 2023, Ecuador finalised the largest debt-for-nature swap in history: a $1.6 billion refinancing of Ecuadorian Galápagos district sovereign debt through a Credit Suisse blue bond underwritten by the US International Development Finance Corporation. The swap converted high-cost Ecuadorian sovereign debt into lower-cost conservation bonds; the interest savings — approximately $323 million over 19 years — are committed to conservation spending in the Galápagos Marine Reserve and the surrounding continental shelf. Conservation monitoring and reporting requirements are among the bond's covenants; failure to meet conservation benchmarks triggers financial penalties.

The Ecuador swap demonstrated feasibility at scale for the sovereign debt-conservation finance mechanism. Belize had demonstrated the concept at smaller scale in 2021 ($364 million, directing funds to Belize Barrier Reef conservation). Gabon, Barbados, the Cape Verde archipelago, and other biodiversity-rich, debt-stressed sovereign states have been in active discussions for similar instruments. The structural innovation — using the credit market discipline of debt covenant compliance, rather than either grant aid or subsidy, to enforce conservation outcomes — represents a more sustainable finance model than grant-dependent conservation programming.

Natural capital accounting at the national level#

The System of Environmental-Economic Accounting (SEEA), endorsed by the UN Statistical Commission as a statistical standard in 2012, provides a framework for extending national accounts to include the value of natural capital stocks and ecosystem service flows. Under SEEA reporting, a country can track the depletion of its forest stock, fishery stock, mineral reserves, and ecosystem service values alongside its conventional national income accounts — providing the national ledger equivalent of the EDR framework.

The SEEA has been piloted or formally implemented in over 90 countries. The UK Natural Capital Accounts, published by the ONS since 2017, place a monetary value on UK ecosystem assets and track year-on-year changes. The World Bank's Wealth of Nations accounts include natural capital alongside produced capital and human capital in a comprehensive national wealth assessment. These accounting frameworks make ecosystem service flows visible in the national accounts; they do not yet create direct policy linkages or mandatory reporting requirements comparable to the Integrated Reporting frameworks being developed for corporate environmental disclosure.

The TNFD (Taskforce on Nature-related Financial Disclosures), which released its final recommendations in September 2023, extends the natural capital accounting framework to the corporate level. Modelled on the TCFD climate disclosure framework, the TNFD requires companies to assess and disclose their dependencies on, and impacts on, natural capital — providing the corporate-level EDR measurement that investors and creditors need to price nature-related risk in their portfolios. Adoption is currently voluntary, with a small number of pioneering companies having been involved in the pilot phase.

What the EDR tells us about the current architecture#

The Ecosystem Dependency Ratio, applied honestly to the current architecture, produces an uncomfortable result. The GBF committed to mobilise $200 billion per year by 2030; the current level is approximately $100–130 billion per year; the needed level is approximately $700–900 billion per year (using the OECD's comprehensive biodiversity finance gap analysis including indirect harmful subsidies to be redirected). Against an EDR numerator of $44–145 trillion per year in ecosystem-dependent economic output, the required investment represents approximately 0.5–2% of the output it is supposed to protect.

No corporation that discovered its primary supply chain was failing at a rate of 1–2% per year would tolerate investing 0.05% of its revenue in supply chain maintenance. The structural dissonance is not between what is needed and what is possible — the $700–900 billion investment required, while large, represents approximately 1% of global GDP. It is between what is needed and what the political economy of national governments, subject to near-term budget pressures and long-term legacy costs, has been willing to generate.

The account must be closed before the capital is gone#

The biodiversity budget has one property that distinguishes it from most financial accountability problems: the asset being drawn down cannot be reconstructed once destroyed. A bankrupt corporation can be recapitalised; a depleted aquifer eventually recharges; a degraded soil can be regenerated with sufficient time. An extinct species is permanently absent from the compound library, the pollination network, the food web structure, and the genetic archive. The extinction debt already committed — the species not yet extinct but ecologically committed to extinction by habitat loss already occurred — means that some portion of the asset diminution is already irreversible regardless of decisions made today.

The Ecosystem Dependency Ratio is ultimately a metric of how close to the edge the economy is operating on the biodiversity budget. At an EDR of 1,000, a 1% decline in the capital stock generating ecosystem services removes approximately $1.44 trillion from the flows that the economy depends on. The current rate of ecosystem service value loss — estimated at $4–20 trillion per year from land use change alone — represents a 3–15% annual diminution of the capital at the upper end of estimates. The economy is not operating on the interest from a healthy capital stock. It is liquidating a capital stock that took billions of years to accumulate, at a rate that requires the accounting to be done before the account is exhausted.

The policy architecture — the GBF, the TNFD, debt-for-nature swaps, natural capital accounting — represents the beginning of a rational response. The investment level it has generated represents a small fraction of a rational response. The distance between the beginning and the sufficient is, on any honest reading, the most important number in international environmental policy that is not yet being treated as the financial emergency it constitutes.