The Mexican IMMEX model did not emerge in isolation. It is one variant of a global policy template promoted by international financial institutions, bilateral donors, and development agencies since the 1980s. Today, dozens of countries operate Special Economic Zones (SEZs) and export‑processing zones (EPZs) that offer foreign investors the same deal: duty‑free imports, tax holidays, weak labour protections, and unrestricted profit repatriation. In exchange, they receive jobs – but rarely the kind of industrial deepening that builds self‑sustaining economies.

This part surveys nine countries across Asia, Africa, and Latin America that have embraced this model. The pattern is consistent: large FDI inflows, very low wages, generous tax breaks, minimal local linkages, and persistent profit outflows.

The Scale of FDI Inflows#

The nine countries have attracted substantial foreign investment. Vietnam leads the pack, targeting $25–30 billion annually by 2025, driven by a shift of supply chains away from China. Cambodia recorded $5.2 billion in 2025, up 18% from the previous year, with China accounting for over 70% of inflows. Indonesia attracted $4.2 billion (H1 2025 alone from Singapore in Batam). The Philippines, Ethiopia, Bangladesh, and Honduras follow with smaller but significant amounts.

Yet these inflows, when compared to GDP or population, do not translate into proportional development gains. As Figure 6 shows, the largest recipients are not necessarily the ones that have escaped low‑wage, low‑value‑added traps.

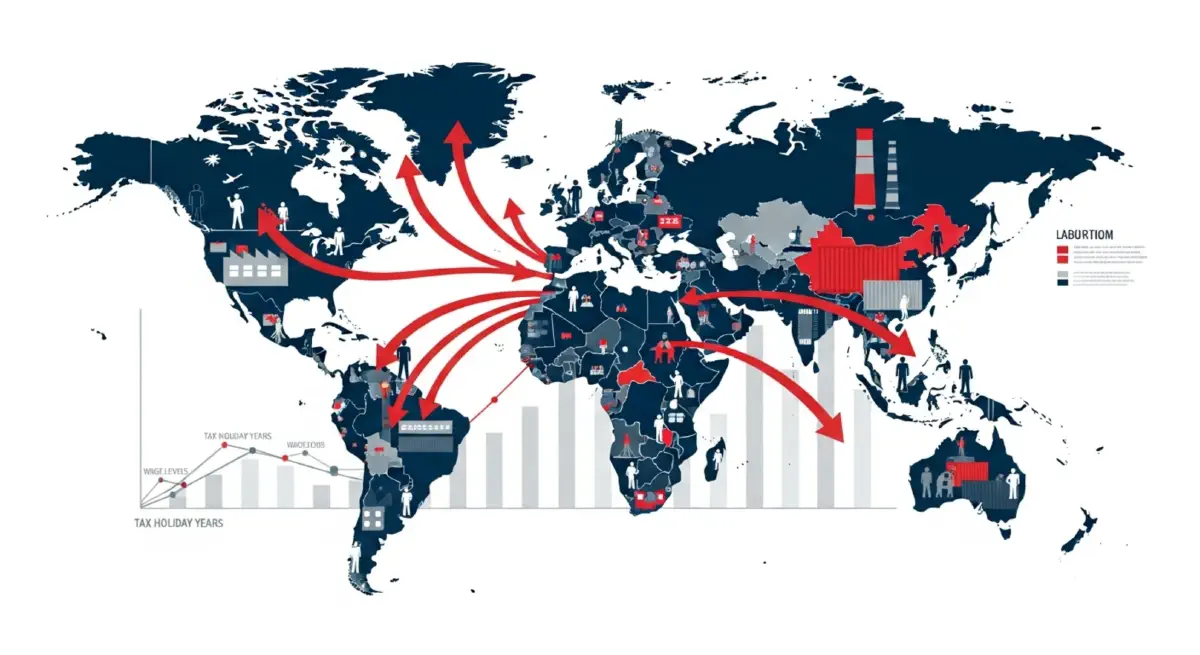

The Race to the Bottom: Wages and Tax Holidays#

A defining feature of the modern FDI model is the inverse relationship between wage levels and the generosity of tax incentives. Countries that offer longer tax holidays tend to have lower wages – because they compete primarily on cost, not on productivity or market access.

Figure 5 plots monthly wages against tax holiday length for six of the nine countries. Sri Lanka’s Colombo Port City offers an extreme 25‑year tax holiday at a monthly wage of about $200. Cambodia offers 9 years at $210. Ethiopia offers 7 years at just $65 – the lowest wage in the sample. Vietnam offers only 4 years but pays $350, reflecting slightly stronger bargaining power. The Philippines’ PEZA zones offer 4–7 years at $350.

This correlation is not coincidental. Tax holidays are a signal that a country has few other assets to attract FDI. They also reduce the fiscal revenue available for public investment – education, health, infrastructure – that could raise productivity and wages over time. The result is a self‑reinforcing trap: low wages attract footloose investors, who demand tax breaks, which starve the state of resources, which keeps wages low.

Country Snapshots: Variations on a Theme#

🇻🇳 Vietnam#

Vietnam has been the most successful at climbing the value chain, moving from textiles to electronics and now semiconductors. It offers 4‑year tax holidays (0% CIT) followed by 9 years at 5% and 10% thereafter. Wages average $300–400 per month. Profit repatriation is allowed after audited statements, with a 5% withholding tax on dividends. However, local linkages remain weak; most high‑value components are still imported.

🇧🇩 Bangladesh#

Bangladesh’s EPZs employ about 550,000 workers, mostly in garments. The minimum wage is $200 per month. Tax holidays range up to 10 years depending on location. Yet the International Trade Union Confederation (ITUC) has ranked Bangladesh among the world’s 10 worst countries for workers’ rights for nine consecutive years. Profit repatriation is often delayed due to dollar shortages, a symptom of the country’s chronic balance‑of‑payments pressure.

🇰🇭 Cambodia#

Cambodia offers up to 9 years of profit tax exemption for Qualified Investment Projects (QIPs). The 2026 minimum wage is $210 per month. China accounts for over 70% of FDI. There are no restrictions on profit repatriation. Labour inspections exist but are underfunded. The economy remains heavily dependent on garment exports with minimal local fabric production.

🇪🇹 Ethiopia#

Ethiopia’s industrial parks – built with Chinese and Turkish finance – offer 2‑7 year tax holidays, duty waivers, and cheap land. Wages in the textile sector are as low as $50–80 per month. A 2025 amendment imposes a 15% tax on profits repatriated by non‑resident entities, a rare attempt to capture some value. However, labour rights are severely constrained, and attrition rates are high. The Friedrich‑Ebert‑Stiftung notes a wide gap between global frameworks and on‑the‑ground realities.

🇭🇳 Honduras#

Honduras’ maquila sector generates $1.5 billion in foreign exchange annually – about half the country’s exports. The minimum wage for maquila workers was adjusted to $399 per month in 2025, the second‑lowest in the economy. The workforce is predominantly female. However, the sector is notoriously footloose; plants have relocated to even lower‑cost countries like Nicaragua or Vietnam. The ILO has repeatedly raised concerns about freedom of association.

🇱🇰 Sri Lanka#

The Colombo Port City – a massive Chinese‑backed SEZ – offers a 25‑year tax holiday followed by 10 years at 50% reduction. Dividends to non‑residents are exempt from withholding tax. Wages in manufacturing are around $150–250 per month. To encourage local linkages, the government offers supplier development tax credits, but implementation is weak.

🇵🇰 Pakistan#

Under CPEC Phase II (launched 2025), China is leading the development of SEZs. One such zone attracted $100 million in initial investment. Tax policies are preferential, and profit repatriation is allowed subject to central bank approval. Wages in textiles are about $150–200 per month. The long‑term impact on local industrial capacity remains uncertain.

🇮🇩 Indonesia#

Indonesia has adopted a “downstreaming” policy to force more value addition, particularly in nickel processing. SEZs offer 10‑20 year tax holidays depending on investment size. Wages average $300–400 per month. The Batam SEZ, close to Singapore, attracted $617 million from Singapore alone in H1 2025. Profit repatriation is allowed but subject to approval. Indonesia’s approach is more assertive than most, yet local content requirements are often bypassed.

🇵🇭 Philippines#

The Philippine Economic Zone Authority (PEZA) offers 4‑7 year income tax holidays followed by a special 20% CIT (standard is 25%) for firms that choose enhanced deductions. Wages are $300–400 per month. PEZA promotes “sustainable development” and some local content, but foreign firms often operate as export enclaves. Profit repatriation is freely allowed.

The Persistent Drain: Profit Outflows#

All nine countries allow profit repatriation with few restrictions (Ethiopia’s 15% tax is a rare exception). The result is that a significant portion of FDI inflows immediately flows back out as dividends, interest, royalties, and management fees. Globally, developing countries lose $675 billion annually to such outflows (Figure 3). For these nine countries, the net contribution to local investment is far smaller than gross inflows suggest.

Conclusion: A Global Plantation System#

The nine countries span three continents, but their FDI policies are strikingly similar: low wages, long tax holidays, weak labour protections, and open capital accounts that allow profits to leave freely. This is not a collection of national failures; it is a global system in which countries compete to offer the most attractive conditions to foreign capital. The winners are multinational corporations, which capture the difference between local costs and global prices. The losers are workers, local suppliers, and long‑term industrial development.

But some countries have escaped this trap. In Part IV, we will examine how South Korea, Taiwan, and China imposed conditions on FDI – and how developing countries today could reclaim their policy space.

Next: Part IV – The Path Forward: Rejecting the Plantation Model