Back to Westminster#

In the autumn of 2025, the UK National Archives completed the digitization of an additional tranche of colonial administrative records from the India Office and the Colonial Office, making accessible, for the first time in fully searchable form, several decades of Home Charges correspondence that had previously required a physical visit to Kew to examine. Among researchers who work in British imperial economic history, this was a welcome development. Among politicians, journalists, and the wider public, it was not noticed.

This is the condition in which the question Parliament avoided in 1879 still stands: the evidence is available, increasing in volume and accessibility, and the political community has maintained the same incuriosity about it that characterized the three evenings in June 1879 when Gladstone and Smollett made their arguments to an audience that agreed with them and did nothing.

This final post assembles the four previous posts into a consolidated verdict. It does not resolve the moral arguments about colonialism — those are not its territory. It addresses the narrower and more tractable question: as a matter of fiscal structure, who paid for the British Empire, who received its gains, and what was the mechanism that maintained the gap between these two populations across the full century of the empire’s mature operation?

Assembling the Balance Sheet#

The Four Findings#

The previous posts established four findings, each independently documented from primary sources, that form a coherent account when read together.

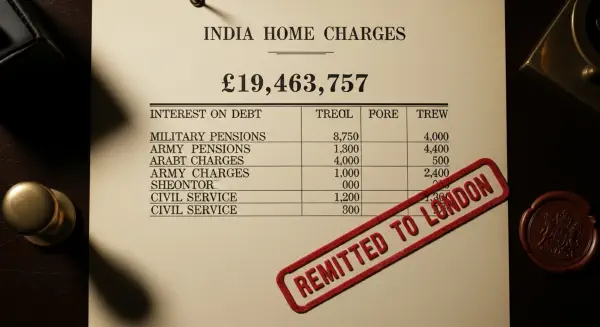

The first is that India transferred approximately £19.5 million per year to Britain in formally documented Home Charges by 1904–05, a figure that had grown 122% between 1868 and 1879 alone and that had consumed, by 1879, the full equivalent of India’s net land revenue. This transfer was not illegal, not secret, and not the result of any single policy decision — it was the accumulated product of administrative structures established over the preceding century and maintained through the combined authority of the India Office in Whitehall and the colonial government in Calcutta, with no effective parliamentary check on its rate.

The second is that Davis and Huttenback’s 1986 analysis of 482 imperial companies found that the dependent empire — Crown India and British Africa — attracted approximately 3% of British private capital across the 1865–1914 period, and that imperial investment on average produced lower returns than domestic investment. The empire was not a profitable investment vehicle for British capital in aggregate. It was, in Davis and Huttenback’s precise finding, “bad business for the nation” — with the qualification that follows.

The third is that the British middle-class taxpayer subsidized imperial defense, through a military budget that protected imperial investment routes and reduced the political risk premium on imperial securities, while the returns on those securities flowed to the small investor class holding India Office stock and imperial corporate bonds. The defense subsidy effectively transferred wealth from the taxpaying population to the investing class, with no mechanism for accountability because the two transactions — tax collection and investment return — occurred in separate columns of separate ledgers.

The fourth is that peripheral colonial territories like Basutoland ran fiscal deficits that British Treasury grants covered, while their administrations maintained European-standard salaries for European staff and administered wage scales that kept native workers below the entry level of the European professional hierarchy regardless of competence or seniority. These territories were not generating national profit for Britain; they were generating private income for a specific class of British administrators and the families from which that class was recruited.

The Qualification That Changes Everything#

The qualification that Davis and Huttenback attach to their finding — “bad business for the nation, good business for certain classes” — is the key that unlocks the entire structure. If the empire produced lower-than-domestic-average returns on investment, why did it continue to exist? Why did British political energy pour into imperial expansion during a period when rational capital allocation should have directed it elsewhere?

The answer is that the relevant decision-makers — the Members of Parliament with connections to the City of London and the India Office, the colonial administrators whose careers depended on the empire’s institutional continuity, the newspaper proprietors whose readership of imperial adventure produced circulation — were not the beneficiaries of the average return. They were the beneficiaries of the distribution. The insider return, for the class with access to privileged information, government contracts, and the ear of the Viceroy, was considerably above average. The outsider return — for the small investor who bought India Office stock on the open market because it was “safe” — reproduced the mediocre aggregate. The system was designed to concentrate information and access, which is to say, it was designed as an extractive hierarchy, not a productive economy.

The Fiscal Extraction Index#

A Metric for Transfer#

The previous post in this series introduced the Human Cost Index as an analogy — a metric that expresses the cumulative cost of armed conflict relative to population size. The same logic can be applied to fiscal extraction. Define the Fiscal Extraction Index as the annual Home Charges transfer per capita of the colonial population, expressed in current-year purchasing power. For India in 1904–05, the calculation is: £19,463,757 divided by approximately 250 million people equals approximately £0.078 per person per year. In 2024 sterling, £0.078 in 1905 is roughly £10–12 per person per year, depending on the deflator used.

This number appears small — £10 per person per year — until it is placed in context. The average annual income of an agricultural laborer in rural India at this period was approximately 20–30 rupees, equivalent to roughly £1.50–£2.00 sterling at contemporary exchange rates. The Home Charges levy, translated into per-capita burden, represented approximately 0.5–0.8% of the average Indian agricultural laborer’s annual income — extracted every year, compulsorily, with no benefit returning to the payer beyond the maintenance of the administrative structure that collected the tax.

Over the period 1858–1947, accepting the broad estimates available in the secondary literature, total Indian fiscal transfers to Britain — in the form of interest on debt, military charges, civil service pensions, and India Office administrative costs — likely exceeded £1.5–2 trillion in contemporary values. Utsa Patnaik’s more comprehensive calculation, which includes not only these formal transfers but the suppressed value of trade surpluses captured through the Home Charges mechanism, estimates the total at approximately $45 trillion (USD at 2018 prices). The magnitude of the estimate depends heavily on methodology, and the precise figure is contested — but no serious economic historian contests that the direction of transfer was consistently from India to Britain over the full period.

The Compound Effect of Underdevelopment#

The Fiscal Extraction Index captures only the direct transfer. It does not capture what India did not build because the transferred resources were not available for domestic investment. The railways that British capital did build in India — those that attracted some portion of the ~3% of British private capital that went to the dependent empire — were built primarily on lines that served the extraction of primary commodities to ports, not on lines that connected Indian agricultural regions to Indian industrial centers. The consequence was a railway network optimized for colonial extraction rather than indigenous development.

The same pattern held in public works more broadly. J.K. Cross’s 1879 complaint about the reduction in Indian public works expenditure — the proposal to cut productive public works from £9.3 million to £6.5 million per year — was not an argument for Indian development as an end in itself. It was an argument that India could not afford to reduce infrastructure investment without accelerating the fiscal deterioration that was producing the crisis. But the underlying constraint Cross identified — that the Home Charges structure consumed so large a fraction of Indian revenue that no surplus was available for reinvestment — is precisely the mechanism through which extractive fiscal transfer impedes development regardless of the stated intentions of the extracting authority.

Who Bore Costs: The Three Populations#

The Indian Agricultural Population#

The primary cost-bearer of the British imperial system was the Indian agricultural population: the 200–250 million people who, through land taxes, provided the revenue base from which the Home Charges were funded. They paid the charges on the loans that had financed their own conquest. They funded the salaries of officers who administered them at British professional rates. They paid the pensions of those officers in retirement. They bore the exchange risk when the rupee depreciated against sterling — not only in the direct sense of the government needing more rupees to discharge its sterling obligations, but in the indirect sense of their export earnings being converted into sterling at rates the Government of India controlled.

They had no vote in the British Parliament. They had no effective legal recourse against the level of Home Charges. The only channels through which they could contest the terms of their taxation were the petition system, which generated eloquent parliamentary speeches, and, ultimately, the organized resistance that the imperial system called sedition and the contested history of the twentieth century evaluates more sympathetically.

The British Working and Middle Classes#

The second cost-bearing population was the British working and middle class, whose taxes funded the naval and military budget that Davis and Huttenback identify as the central subsidy to imperial investment. These are not heroic victims of the imperial system — many of them were enthusiastic supporters of empire, for reasons ranging from genuine belief in British civilizational superiority to the more immediate benefit of cheap imported food that empire helped secure. Tea, sugar, cotton textiles: the goods that cheapened the British working-class standard of living were produced under colonial conditions that suppressed the price paid to colonial producers.

But in fiscal terms, the British working and middle classes were net contributors to the defense subsidy that underpinned imperial investment returns, without being the primary recipients of those returns. The factory worker who paid income tax was funding a guarantee on the India bond held by the retired civil servant. This is not a claim that the factory worker’s life was made worse by empire in net terms — cheap tea and cotton meant something real. It is a claim that the fiscal structure transferred resources from the tax-paying population to the investing class in a way that the separate-ledgers accounting deliberately obscured.

The European Administrative Class#

The primary beneficiary of the imperial fiscal system, at the ground level documented in the Colonial Office Blue Books, was the European administrative class: the men who staffed the colonial civil services, the military officer corps, the judiciary, and the technical departments of colonial governments, at salary scales priced at British professional rates and funded from colonial tax bases that could not maintain those scales without British Treasury support.

This class was not large in absolute terms — perhaps 70,000–100,000 individuals in the dependent empire at peak, with a much larger network of dependents, investors, and connected commercial interests in Britain. But it was precisely positioned to shape imperial policy, because it provided the human infrastructure through which the British state administered the empire and because its members returned to Britain with the social capital, the political connections, and the personal networks that translated colonial careers into metropolitan influence.

The Mechanism: Why the System Sustained Itself#

The Absence of Consolidated Accounting#

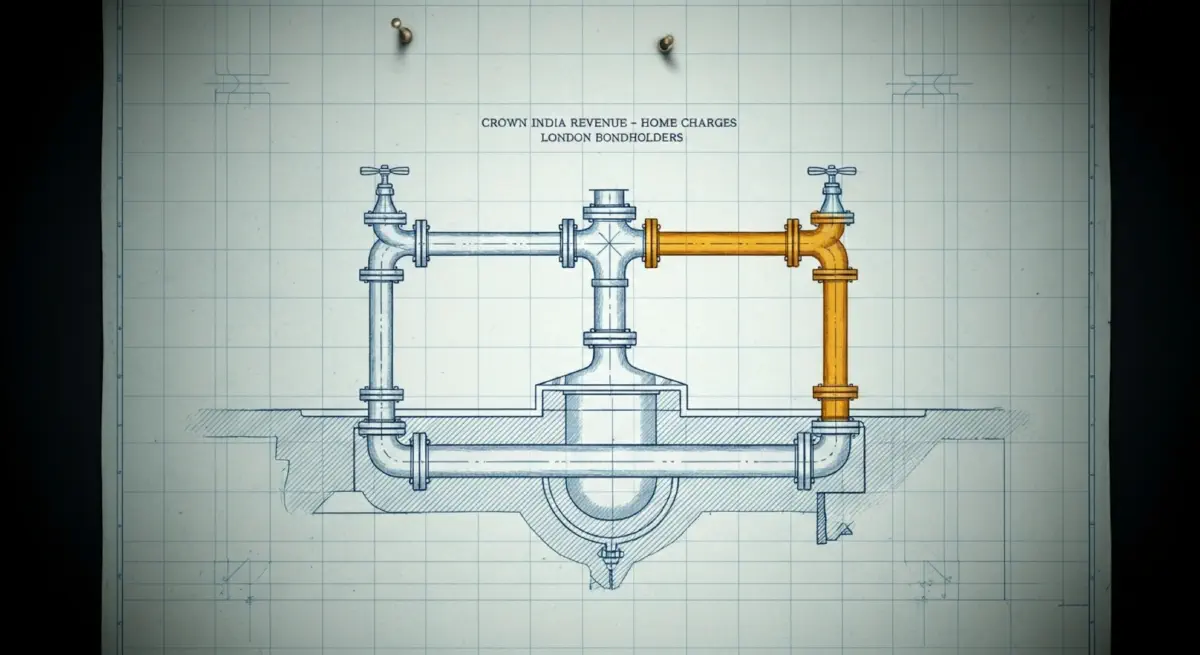

The most important structural feature of the imperial fiscal system — the element that makes the question Parliament avoided in 1879 still unanswered — was the deliberate absence of consolidated accounting. Indian revenue and British revenue were kept in separate ledgers. Defense expenditure and investment return were kept in separate ledgers. Colonial wage costs and Metropolitan salary scales were governed by separate administrative frameworks. No single document, produced by any organ of the British state at any point in the empire’s history, attempted to construct a consolidated account of what the empire cost the British public, what it returned to the British public, and who specifically was on each side of that account.

This was not accidental. The administrative complexity of empire provided genuine reasons why consolidated accounting was difficult. But the specific design choices — charging Indian military pensions to Indian revenue, managing Home Charges through the Council Bill mechanism rather than direct appropriation, separating defense expenditure from investment return — were consistently made in the direction of opacity rather than transparency. When Smollett in 1879 accused the previous administration of “cooking the accounts,” he was identifying not fraud but something more structural: a system of classification that made fiscal reality legible only to those with the expertise and motivation to aggregate across accounts that were never intended to be read together.

Gladstone’s Unrealized Warning#

Gladstone warned in 1879 that unless Parliament acted with “adequate and effectual remedies,” the course of events would bring Britain to “the question of assuming responsibility for Indian Expenditure as a charge upon the British Treasury.” The contingency he feared — that the Indian fiscal crisis would become a British fiscal crisis — was averted not by the retrenchment he called for, but by the opposite: by tightening the fiscal transfer mechanism, reducing Indian public works expenditure (as Cross opposed), and extracting greater revenue from the Indian tax base at the cost of increasing economic distress in the agricultural population.

The Home Charges continued to rise after 1879. The structure that generated them continued until 1947. Gladstone’s remedy — real retrenchment, real reform, real reduction in the administrative class’s claims on Indian revenue — was implemented piecemeal, decades late, and never at the scale he had specified as necessary. The system was not reformed because reform would have required the administrative class to accept a reduction in the claims it held on Indian revenue, and the administrative class was the class that administered the reform process.

The Structural Verdict#

What the Balance Sheet Shows#

The consolidated verdict, assembled across four posts from primary sources and the best available secondary analysis, can be stated in terms of the three questions posed in the opening post.

On the treasury question: the British state’s fiscal position was not straightforwardly improved by empire. The Home Charges generated a flow of transfers to London-based investors, officers, and administrators, but these did not accrue to the British Treasury as general revenue. The Treasury’s direct benefit was in reduced domestic political pressure — cheap imported food, employment for the administrative and officer classes — rather than in fiscal surplus. In the peripheral territories like Basutoland, the Treasury was a net contributor. In India, the formal accounts showed a large flow of transfers, but much of that flow bypassed the Treasury and went directly to bondholders and pension recipients.

On the distributional question: the gaining class was specific and identifiable. It consisted of holders of India Office stock and imperial corporate bonds; retired Indian Army and civil service officers; the families from which these officers were recruited and to which they returned; and the commercial houses that operated within the trade structures the colonial administration maintained. The cost-bearing class was equally specific: the Indian agricultural taxpayer; the British working-class taxpayer who funded the defense subsidy; and the colonial native worker whose wage was administratively suppressed below European professional rates.

On the opportunity cost question: the capital and political energy devoted to imperial expansion was not available for domestic infrastructure investment, public health reform, or the social programs that the late nineteenth and early twentieth centuries increasingly demanded. This is the hardest cost to quantify, but it is not zero. The political economy of empire — the need to maintain the officer class, fund the navy, defend the frontier — was consistently prioritized over the domestic social expenditure that the same period’s growing labor movement was demanding.

The Design That Persists#

The structure described in this series is not a relic. The mechanism — costs socialized through general taxation, gains concentrated through private investment, administrative complexity deployed to prevent consolidated accountability — appears in recognizable form in post-colonial economic arrangements. The structural adjustment programs of the 1980s and 1990s, the debt architectures that extract fiscal transfers from low-income country governments to international creditors, the investment protection treaties that guarantee investor returns while socializing political risk — these are not direct descendants of the Victorian Home Charges, but they operate through the same structural principle that Davis and Huttenback identified in 1986: bad business for the nation, good business for certain classes.

The question Parliament avoided in 1879 was not really a question about the exchange rate or the value of the silver rupee. It was a question about whether the costs and gains of a large fiscal system should be made legible to those who bear them. Gladstone recognized the stakes: if the true condition of Indian finance were made visible, the political pressure for reform would become “imperative.” The system’s architects had made it sufficiently complex that this pressure could always be deferred through another commission, another speech, another night of eloquent debate before the procedural resolution and the adjournment.

The ledger has never been fully opened. This series is one attempt to read the entries that are already there.