A Document Nobody Was Embarrassed By#

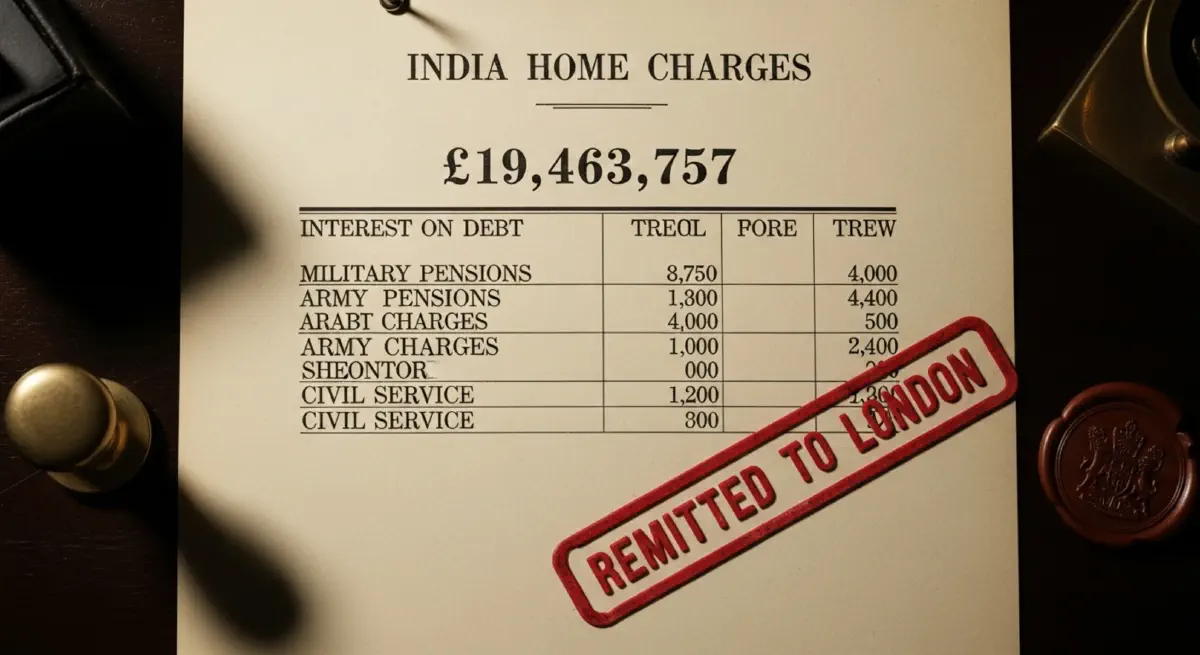

On February 19, 1906, a schedule of accounts was presented to the House of Commons. It ran to several pages of small type, organized into line items with the precision that only Victorian parliamentary accountancy could achieve. The document’s formal title was understated to the point of self-parody: East India Revenue Accounts: Schedules of Home Charges Paid from Indian Revenues, 1904–05. It was not a secret. It had been prepared and published annually for decades. Every Member of Parliament who cared to examine it could find the following entry at the top of the summary sheet: total Home Charges for the year, £19,463,757.

This was the amount India paid Britain in a single year, through a mechanism as well-designed as any fiscal transfer mechanism in modern public finance, and as thoroughly invisible to most of those who bore its costs. The sum was broken into components with the logic of double-entry bookkeeping: interest on India’s London-held debt — the debt incurred in the conquest and administration of the subcontinent — came to £9,710,000. Military charges for officers and soldiers technically assigned to India but stationed in England came to £5,870,000 in various categories. Administrative costs of the India Office in Whitehall, the salaries of officials whose “service” was conducted at their London desks, added further columns to the total. The Indian taxpayer funded all of it.

Smollett had warned in 1879 that “one-fourth of all the officers belonging to the Indian Army, for whom India is paying, are in England.” General Pears had confirmed the figure to the India Finance Committee. By 1906, the system had not contracted. It had matured.

The Structure of the Drain#

The term “drain” appears throughout the secondary literature on British India, most prominently in the work of Dadabhai Naoroji, the first Indian elected to the House of Commons, whose 1901 book Poverty and Un-British Rule in India traced what he called the “Home Charges” as a systematic extraction of Indian wealth. The academic consensus, refined by B.R. Tomlinson, Utsa Patnaik, and others, is that Naoroji was substantially correct: the Home Charges constituted a transfer mechanism without analogy in modern fiscal systems, in which the taxed population had no parliamentary representation and no legal recourse against the rate of transfer.

But the term “drain” carries a connotation of accident or overflow — water escaping through a crack. What the 1906 accounts reveal is something more deliberate: a carefully itemized system of scheduled transfers, established in treaty and administrative law, operating transparently, and contested only by a small number of Indian politicians and a handful of dissenting British MPs whose speeches, however acute, made no impression on the rate at which the transfers proceeded.

The Components: Who Got What#

The largest single component of India’s Home Charges in 1904–05 was interest on debt: £9,710,000. This requires a moment’s attention to the history that generated it. India’s London-held public debt was the accumulated borrowing of the colonial government — borrowing to finance the wars of conquest, the railway infrastructure built primarily for strategic and commercial extraction rather than native welfare, and the deficits generated when revenues fell short of administrative expenditure. The interest was contractually due in London, in sterling. India earned sterling through its export surplus, which it used to purchase the Council Bills through which the Home Charges were remitted. The entire circuit was closed: India’s agricultural exports funded the interest on the debt its conquest had generated.

The second major component was military charges. The 1906 accounts listed £4,413,000 for non-effective military services — pensions for retired officers and soldiers who had served in India. These men were entitled to their pensions; the question was who paid them. The answer that Parliament had established, and that the India Finance Committee of 1873 confirmed, was that India paid. Officers who had commanded Indian soldiers, administered Indian districts, and retired to English country houses continued to receive salaries paid from Indian tax revenue for the remainder of their lives. The 1879 debate had revealed that a quarter of all officers on the Indian Army establishment were physically in England at any given time — and India was paying their effective-service charges as well.

Beyond military pensions, the accounts itemized “army effective charges” — costs related to British troops formally assigned to the Indian Army but stationed in Britain. J.K. Cross had calculated in 1879 that the cost of recruiting a single British soldier for India had risen from £42 per head under the East India Company to £82 per head under Crown administration — a near-doubling with no corresponding improvement in military effectiveness. Every recruit, every billet, every uniform and ration purchased in England was charged to the Indian exchequer.

The Trade Balance That Wasn’t a Balance#

Cross identified in the 1879 debate a dimension of the Home Charges mechanism that the formal accounts did not capture: the conversion of India’s export surplus into charges rather than returns. India sent, he said, “nearly £20,000,000 a-year more” to Britain in exports than Britain sent to India in imports. In any ordinary commercial relationship, this surplus would reflect India’s wealth — its ability to produce more than it consumed in the bilateral trade. It would generate purchasing power that cycled back into the Indian economy.

But the surplus was not India’s to deploy. The mechanism by which Indian exporters were paid — in rupees, from Indian Government accounts — and by which the equivalent sterling was remitted to London as Home Charges meant that the export surplus did not function as income for the Indian economy. It functioned as a transfer. The British merchant who bought Indian cotton paid in sterling; that sterling was credited to the India Office; the Indian weaver was paid in rupees drawn from Indian Government funds. The sterling never crossed the other direction. This was not a trade relationship; it was fiscal extraction wearing the appearance of commerce.

The Home Charges as a Percentage of India’s Revenue#

A Rising Share of a Fixed Tax Base#

The most revealing figure in the 1879 debate was not the absolute level of the Home Charges — large as that was — but its proportion of India’s available revenue. Cross had access to the India Finance Committee evidence and to the accounts then available, and he stated the arithmetic with precision. In 1868, the Home Charges required 84.97 million rupees to discharge. India’s net land revenue that year was approximately 195 million rupees. The Home Charges consumed 43.5% of it.

By 1879, the Home Charges had risen to 189 million rupees. India’s net land revenue had not grown proportionately; the land tax was extracted from a largely static agricultural economy, and the famines of 1876–78 had reduced actual collections. The Home Charges now consumed the equivalent of the entire net land revenue of India. Every rupee the farmer paid as land tax — the most ancient and politically sensitive of all Indian levies — was, in effect, remitted to London before any Indian public expenditure could draw on it.

By 1904–05, the formal accounts showed a total of £19,463,757. India’s total revenue in that year was approximately £51 million. The Home Charges represented approximately 38% of total revenue — a figure that had barely moved from Smollett’s 1879 alarm, despite three decades of warnings, commissions, and speeches.

What the Trend Line Showed#

The trajectory from 84.97 million rupees in 1868 to 189 million rupees in 1879 was not the result of any sudden policy change. It was the compound effect of decisions made across decades — to expand the Indian Army on British model terms, to borrow in London rather than Calcutta, to treat retired officers’ pensions as an Indian liability rather than a British one, and to price Civil Service appointments in India at rates designed to attract the sons of the British professional class rather than the most qualified available administrators.

Each of these decisions had a reasonable bureaucratic justification in isolation. Taken together, they constituted a fiscal architecture whose direction of transfer was fixed: outward from India to Britain, structured so that no single line item was large enough to provoke political crisis, while the aggregate was large enough to generate existential danger to Indian public finance whenever revenue fell short of projection.

Gladstone saw the architecture even if he could not name it precisely: “I confess I am very jealous of mere professional delegations on these subjects. What I most earnestly of all desire is that this body of the Representatives of the people of England should fully and clearly understand that they are approaching, and are called upon to deal with, no remote or secondary matter of the interest of a Dependency.”

The Question of Benefit: Who in Britain Received the Transfer#

The Interest Recipients#

The £9.71 million paid annually as interest on India’s London debt was not dispersed across the British public. It was paid to the holders of India Office stock and India Council Bills — a relatively small class of investors concentrated in the City of London and the professional and landowning classes who held government securities as a standard form of wealth management. These investors received a guaranteed return on instruments backed by the credit of the Government of India — which is to say, by the agricultural taxation of 250 million Indian peasants. The risk was borne by the Indian taxpayer; the return was received by the British bondholder.

This structural relationship — tax risk socialized onto a colonized population, investment return privatized to a metropolitan creditor class — is the central mechanism of what the next post examines more broadly across the entire empire. It is not a conspiracy. It is a system. The debt was real; the interest was contractually due; the process was legal. The question the 1906 schedule raises is simply: who voted to establish this arrangement, and who bore its cost?

The Absentee Soldier#

The military pension and effective charges are perhaps the most direct transfer in the Home Charges accounts. An officer who served twenty years in India, commanded Indian soldiers, and retired to Bath was thereafter supported by Indian tax revenue for the remainder of his life. His pension was not paid from British military funds; it was an Indian liability. The Indian population had no mechanism to contest this, and no forum in which to argue that the cost of maintaining the retired British officer class was not properly a charge against Indian agricultural tax revenue.

Cross’s data on the doubling of recruitment costs — from £42 to £82 per head — pointed toward the same dynamic. The expansion of the bureaucratic military-administrative class in India, trained in England, staffed from English families, and retiring to England, was not a cost that the Indian economy generated internally. It was a cost imposed from outside, priced at English professional-class rates, and extracted from an Indian tax base whose capacity to bear such charges was the subject of the 1879 alarm.

The Formal and the Real#

The India accounts were not doctored. The line items were accurate. The totals were correct. What Smollett had called “cooked accounts” in 1879 was a different accusation — not that the numbers were falsified, but that the classification of productive public works as “recoverable assets” had systematically concealed the true state of Indian fiscal affairs from Parliament for a decade. By 1906 the accounting had been cleaned up sufficiently that no such charge was plausible. The Home Charges schedule was frank: it listed exactly what India paid, to whom, and under what authority.

What the formal accounts could not reveal — and what this series reconstructs from Hansard debate and secondary analysis — was the distributional reality on both sides: who in India bore these costs (the land tax-paying agricultural population), and who in Britain received these transfers (the investor, pensioner, and administrative-officer class). When those two distributions are made visible simultaneously, the 1906 schedule reads not as bureaucratic accounting but as the fiscal anatomy of a transfer system designed to be indefinitely sustainable as long as the two populations remained politically separated.

The next post asks the question the 1906 accounts could not answer: given that Britain was receiving these transfers, who within Britain was on the receiving end — and who was paying the costs of the empire on the other side of the ledger?