The Question the Series Has Been Building To#

The previous four posts documented the mechanism: dollar borrowing by commodity-dependent economies, fragmented creditor landscapes that resist restructuring, austerity conditionality that displaces social spending, and a default process whose costs may exceed its savings. A well-constructed analysis of a trap should end not with the trap but with its exits.

There are exits. They are narrow, require specific preconditions, and are not universally available — but the evidence that they exist matters because it distinguishes structural constraints from destiny. Some countries in the same structural category as Zambia or Pakistan have not ended up where Zambia and Pakistan ended up. Understanding why is the prerequisite for designing better paths for the countries that have not yet escaped.

The Five Characteristics of Escape#

Analysis of the countries that achieved durable escape from debt distress — and maintained that escape across multiple commodity cycles and global shocks — identifies five structural characteristics that distinguish them from countries that relapsed. None of these characteristics is independently sufficient. All five operate together as a system.

1. Export Diversification Beyond Primary Commodities#

The Double Bind described in Part 1 operates specifically through commodity-price exposure: export revenues fluctuate with commodity cycles the country does not control, making debt service reliability impossible to guarantee. Countries that have diversified their export bases — adding manufacturing, services, or processed agricultural products alongside raw commodity exports — have substantially reduced this exposure.

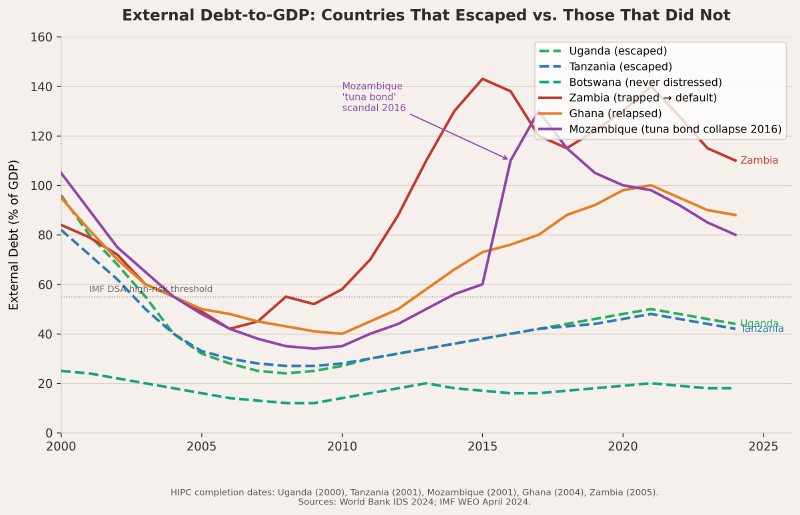

Uganda’s post-HIPC growth was built on a diversification that went well beyond coffee, its primary colonial-era export. Horticulture (cut flowers, USAID-assisted horticultural development), fish processing (Nile perch from Lake Victoria), light manufacturing, and regional services (Kampala became a significant regional financial and logistics hub) collectively reduced coffee’s share of export revenues from dominance to one significant component among several.

Rwanda took an extreme version of this path: a landlocked country with no oil, no major minerals, and a colonial legacy of subsistence agriculture, it deliberately built a services-and-technology-oriented economy — positioning Kigali as an African conference and financial services hub, investing heavily in mobile broadband infrastructure, and developing a governance-and-business-environment brand that attracts foreign direct investment. Rwanda’s top export by value is now services. This is not a replicable template for all countries, but it demonstrates that structural transformation is possible within a fifteen-year horizon.

2. Domestic Revenue Mobilization Above 18% of GDP#

The fundamental reason countries borrow externally to fund operating expenditures — teacher salaries, healthcare provision, basic infrastructure maintenance — is that domestic tax revenues are insufficient to fund those expenditures. Raising more domestic revenue reduces the volume of external borrowing required and eliminates the most fiscally dangerous form of external debt: borrowing in foreign currency to fund domestic-currency operating costs.

The threshold of 18 percent of GDP in tax revenue is identified in the development economics literature (notably Gaspar et al., 2016, IMF fiscal affairs) as the level above which countries can fund basic public services without systematic external dependence. Below it, the fiscal gap tends to be filled by external borrowing. Above it, countries have room to build domestic savings, fund investment, and manage shocks without immediate recourse to international capital markets.

Tanzania’s revenue-to-GDP ratio was approximately 10 percent at HIPC completion in 2001. By 2015 it was approximately 15 percent — still below the threshold, but rising through a sustained effort of informal sector formalization, tax administration modernization, and base broadening. Rwanda reached 20 percent by 2018 — an exceptional figure for Sub-Saharan Africa, achieved through deliberate investment in the Rwanda Revenue Authority and a political commitment to domestic resource mobilization as the foundation of development finance.

3. Local-Currency Bond Market Development#

A government that can borrow in its own currency to fund its domestic operations has eliminated the currency mismatch that is, as Part 1 documented, one of the primary drivers of the Double Bind. Local-currency debt obligations are payable with locally generated revenue. Dollar appreciation does not increase their real cost. Dollar depreciation does not reduce the government’s capacity to service them.

Building a functioning local-currency bonds market requires several preconditions: macroeconomic stability sufficient to make long-term kwacha or shilling yields attractive to domestic savers and institutional investors; a pension fund sector large enough to absorb sovereign paper; a functional primary dealer system; and financial sector supervision capable of managing the systemic risks of concentrated government bond holdings in the banking system.

Botswana built this infrastructure deliberately from the 1980s forward, alongside its sovereign wealth fund management. Rwanda developed its local bond market as a deliberate component of its financial sector development strategy. Tanzania has made significant progress. What consistently distinguishes these countries from the relapsers is the treatment of local-currency bond market development as a medium-term fiscal infrastructure priority rather than an aspiration.

4. Transparent Debt Management#

The Mozambique case is instructive in a negative direction. Mozambique completed HIPC in 2001 and was, through 2015, widely cited as a successful post-conflict development story: GDP growth of approximately 7.4 percent per year, declining debt-to-GDP, improving social indicators. In 2016, it emerged that the Mozambican government had contracted approximately $2 billion in hidden loans — the so-called “tuna bonds” — through state-owned enterprises, on behalf of fishing and maritime security projects, at commercial rates, without disclosing the obligations to the IMF, the World Bank, or donor governments that had been providing budget support on the assumption that the government’s fiscal position was as reported.

The hidden debt represented approximately 11 percent of GDP. When it emerged, donor support collapsed, the metical depreciated sharply, and Mozambique entered a debt crisis from which it has only slowly recovered. The crisis was not caused by the commodity price cycle or dollar appreciation or IMF conditionality. It was caused by the absence of transparent debt management — a single institution, with legislative authority, responsible for tracking, reporting, and approving all government borrowing.

The World Bank’s Debt Management Facility (DMFAS program) exists precisely to build this capacity in developing countries. The countries that avoided the Mozambique failure had invested in this infrastructure as a precondition for sustainable borrowing, rather than as an afterthought.

5. Concessional Borrowing Discipline#

The final characteristic is the most straightforwardly behavioral: access to concessional financing (IDA credits at approximately 1.25 percent, African Development Bank loans at 1–3 percent, bilateral ODA) carries significantly lower interest costs than commercial Eurobonds. Countries that have maintained discipline about using concessional sources first — and accessing commercial markets only for projects that generate sufficient returns to cover commercial borrowing costs — have avoided the primary driver of debt accumulation in the relapse cases.

Ghana’s reaccumulation problem began precisely when it substituted Eurobond issuance (at 8.5–10 percent) for IDA credit (at 1.25 percent) for the same classes of expenditure — partly because IDA financing comes with procurement and fiduciary conditions that limit the speed and discretion of disbursement, and partly because commercial markets were available and welcoming after the HIPC success. The regulatory architecture of concessional borrowing is not designed for convenience. It is designed for sustainability. Substituting away from it for convenience trades long-term fiscal stability for short-term political flexibility.

Debt-for-Nature Swaps: A Structural Tool, Not a Niche Instrument#

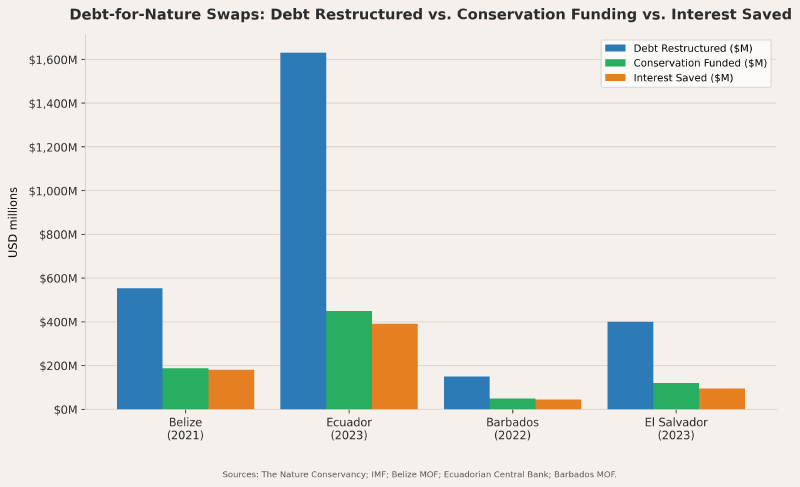

Debt-for-nature swaps have existed since the 1980s as a marginal instrument, used primarily by bilateral creditors and conservation organizations to redirect small amounts of bilateral debt toward environmental programs. The Ecuador Galápagos transaction of 2023 represents a significant evolution of the instrument into something with genuine scale potential.

Ecuador restructured $1.6 billion in existing debt — its largest-ever single debt transaction — through a mechanism that refinanced at 5.6 percent (from the existing blended rate of approximately 10.7 percent) via a blue bond issued by the Inter-American Development Bank, with a guarantee from the US International Development Finance Corporation (DFC). The difference in interest rates — approximately 5.1 percentage points on $1.6 billion — generates approximately $450 million in savings over the bond’s life, directed to a trust fund for the Galápagos Marine Reserve. Ecuador reduced its annual interest payments, extended its fiscal space, and funded the conservation of one of the world’s most significant marine ecosystems simultaneously.

The instrument requires three preconditions: a willing bilateral creditor or multilateral guarantor, a credible conservation governance institution to manage the environmental expenditure, and a legal structure that makes the conservation commitment binding. These preconditions are not universal. But the candidate universe is larger than the four deals completed to date. The World Wildlife Fund, The Nature Conservancy, and the IMF’s own resilience and sustainability facility have all identified a pipeline of potential transactions across the Caribbean, Pacific, and Sub-Saharan Africa.

The significance of the swap mechanism is not primarily environmental. It is structural: it demonstrates that sovereign debt obligations can be restructured at lower cost than commercial restructuring through a public guarantee mechanism, generating fiscal space while meeting a policy objective that bilateral creditors and multilateral institutions have independent reasons to support. It is a template for debt relief that does not require the G20 Common Framework’s coordination challenges because it is negotiated bilaterally between the debtor and a single guaranteeing institution.

What Rwanda Tells Us About Possibility#

Rwanda has no oil. It has no significant mineral resources. It is landlocked, in a region with persistent regional insecurity, in a country that experienced the continent’s most documented genocide in 1994. It had, in 1995, approximately 5.5 million surviving citizens, a destroyed administrative infrastructure, and an external debt of approximately $1 billion — inherited largely from the pre-genocide government.

As of 2024, Rwanda’s GDP per capita is approximately $940 — still low in absolute terms, but among the fastest-growing in Sub-Saharan Africa for the past twenty years. Its debt-to-GDP ratio is approximately 65 percent — elevated but stable. Its SSDR is 0.27 — meaning it pays $0.27 in debt service for every dollar it spends on health and education combined. Its tax revenue is 20 percent of GDP. It has a functioning domestic bond market. Its debt management office has transparent reporting that has consistently satisfied IMF and World Bank monitoring.

Rwanda is a limited model for democratic governance — the RPF government’s consolidation of political control raises human rights concerns that serious analysis cannot omit. But as an economic argument that the structural challenge of debt sustainability in a low-income country can be addressed through deliberate institutional investment, revenue mobilization, and export diversification, Rwanda is one of the clearest empirical demonstrations available.

The escape from the debt architecture is possible. It requires twenty years of sustained institutional investment, fiscal discipline, and a government willing to accept the constraints of concessional borrowing rather than the convenience of commercial markets. It requires export diversification into sectors where commodity price cycles do not determine fiscal capacity. And it requires, at the international level, the infrastructure described across this series: a faster restructuring mechanism, an SSDR-aware conditionality framework, and a guarantee architecture that makes debt-for-nature swaps replicable at scale.

The countries that have escaped did not wait for the international architecture to be reformed. They built internal alternatives to it. The question the series ends on is whether the international community is prepared to reform the architecture to make those alternatives available to countries that have not yet found them — or whether the displacement of social spending by debt service will continue to be documented, assessed, and left in place.

References#

- World Bank International Debt Statistics 2024. https://data.worldbank.org/topic/external-debt

- IMF WEO April 2024. https://www.imf.org/en/Publications/WEO/weo-database/2024/April

- The Nature Conservancy. “Ecuador Blue Bond for Ocean Conservation.” 2023. https://www.nature.org

- Gaspar, Vitor, et al. “Tax Capacity and Growth: Is There a Tipping Point?” IMF Working Paper 16/234, 2016.

- World Bank Debt Management Facility (DMFAS). https://www.worldbank.org/en/topic/debt/brief/debt-management-facility

- Rwanda Revenue Authority. Annual Reports 2018–2023. https://www.rra.gov.rw

- Belize Ministry of Finance. “Blue Bond for Ocean Conservation.” 2021.

- IMF. “Mozambique: Hidden Debt and Its Aftermath.” Article IV Consultation, 2018.

- Reinhart, Carmen M., and Clemens Graf von Luckner. “The Return of Global Inflation.” IMF Finance and Development, 2022.

- Human Rights Watch. “Rwanda.” World Report 2024. https://www.hrw.org/world-report/2024/country-chapters/rwanda