What a Default Actually Is#

In corporate bankruptcy law, default triggers a defined legal process: assets are assessed, creditors are ranked by seniority, a restructuring plan is negotiated under court supervision, and the entity emerges — or is liquidated — within a bounded timeframe. The Bankruptcy Code in the United States specifies ninety days for an initial plan. Courts set timetables. Creditors have legal obligations to negotiate in good faith.

Sovereign default operates in a different world. There is no bankruptcy court for countries. There is no agreed rank ordering of creditors. There is no timetable. There is no court with jurisdiction over a sovereign state’s assets sufficient to compel a restructuring. The entire process depends on the willingness of creditors who have no legal obligation to cooperate to nonetheless cooperate — under pressure from an IMF program, peer pressure from other governments, and the reputational cost of being seen as an obstruction.

The result is a process whose duration is determined primarily by the cohesion of the creditor landscape, and the creditor landscape has, as documented in Part 2, become maximally fragmented over precisely the period when developing countries were most aggressively accessing capital markets.

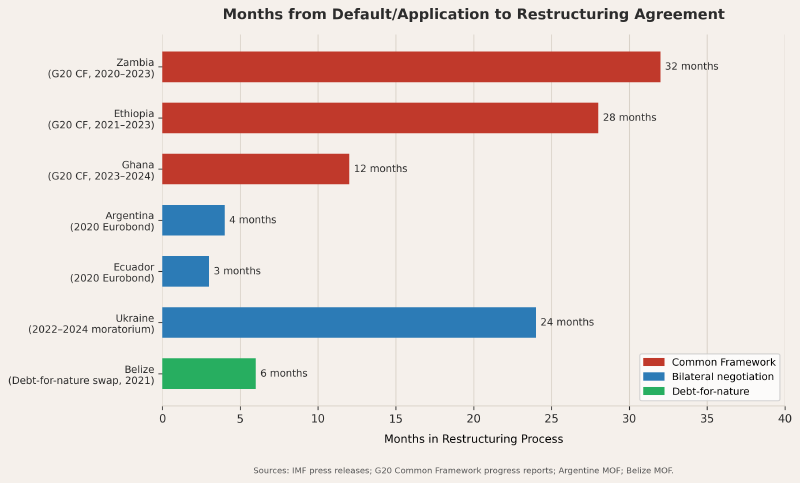

Zambia: 46 Months of Legal Limbo#

Zambia’s default on November 13, 2020, was not a surprise to anyone in the sovereign bond market. By late 2021, Zambia’s Eurobond yields had exceeded 15 percent — a level at which bond markets are effectively pricing default as more probable than continuation. The IMF had been in discussions with the Zambian government since 2020 about a program. The G20 Common Framework had been announced. The architecture for resolution existed, at least on paper.

The preliminary agreement with the Official Creditor Committee — the group of bilateral creditors including China, France, the United Kingdom, and others coordinating under the Common Framework — was reached in June 2023: thirty-two months after the application. The private creditor deal followed in September 2023: forty-six months after default.

What happened in those forty-six months is not merely the inconvenience of protracted negotiation. It is a specific and measurable set of economic consequences:

Capital market exclusion. Zambia could not issue new bonds, could not refinance maturing obligations, and could not attract international commercial investment in conditions of legal uncertainty about the final shape of its debt obligations. Infrastructure projects requiring external financing were frozen or cancelled.

Currency collapse. The kwacha fell approximately 44 percent against the US dollar during the restructuring period. For an economy that imports essential goods in dollars, this constitutes a sustained inflationary shock to every household. The poorest households, which spend the largest share of income on food and fuel, absorbed the largest proportional impact.

Institutional paralysis. Budget planning under IMF program conditions during an active restructuring requires projecting forward costs that are, by definition, unknown until the restructuring is complete. Zambia’s government was operating multi-year fiscal plans with a fundamental unknown — the final cost of debt service — at their centre.

The haircut arithmetic. The final restructuring achieved a net present value reduction of approximately 18 percent. That figure compares unfavorably to the IMF’s own debt sustainability analysis, which had indicated that a deeper reduction — on the order of 40–50 percent NPV — was required to put Zambia’s debt on a sustainable trajectory. The gap reflects the negotiating position of holdout creditors and the absence of a mechanism to enforce comparability of treatment across creditor classes.

The Spread Paradox: When Restructuring Costs More Than It Saves#

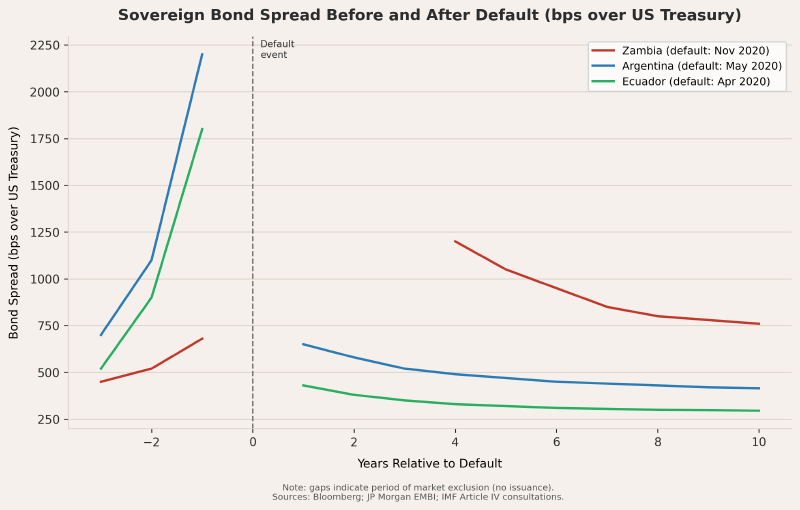

The most counter-intuitive finding in sovereign debt restructuring analysis concerns the relationship between the savings achieved in a restructuring and the costs imposed by re-entry to capital markets after the restructuring is complete.

When a country emerges from default, it is rated by credit agencies at a level that reflects the recent default event — typically a level associated with very high borrowing costs. The country’s first post-restructuring bond issuance must be priced to attract investors who are aware of the default history and demand a significant premium for the risk.

For Zambia, the anticipated first post-restructuring Eurobond issuance is projected to carry a spread of approximately 800 basis points over the equivalent US Treasury rate. At the prevailing 2025 US Treasury rate, this implies an all-in yield of approximately 12–13 percent. Zambia’s Eurobond yields before the debt accumulation crisis peaked were approximately 5.6–8.6 percent.

The NPV savings achieved in the restructuring were approximately $1.1–1.4 billion (on the $6.3 billion bilateral component alone). The additional interest cost over a ten-year period of borrowing at 800bps spread versus a hypothetical pre-crisis baseline of 600bps spread represents a figure in the same order of magnitude. The precise arithmetic depends on future borrowing volumes and rate paths, making an exact calculation impossible, but the structural principle is sound: sovereign debt restructuring saves on the stock while imposing a flow penalty that may exceed the stock savings over the borrowing horizon needed for development.

This is not an argument against restructuring. A country that cannot service its debt will default whether it chooses to or not, and an orderly restructuring is better than a chaotic one. It is an argument that the restructuring process, as currently designed, extracts costs during the negotiation period (exclusion, currency depreciation, institutional paralysis) and imposes post-restructuring costs (spread premium) that compound the damage of the original distress. A genuinely functional international debt architecture would resolve defaults faster and create conditions for faster, cheaper re-entry.

Argentina: The Country That Default Cannot Kill#

Argentina’s sovereign default history is unusual in both quantity and variety. It has defaulted in 1827, 1890, 1951, 1982, 1989, 2001, 2014, and 2020 — eight times in its national history, at an average of once every twenty-five years. Each default has been followed by restructuring, market re-entry, renewed borrowing, and eventually another crisis. The pattern has been documented so extensively that economists use Argentina as a laboratory for testing theories about sovereign debt sustainability.

The 2001 default — $100 billion, the largest in history at the time — was the product of a convertibility regime (a fixed 1:1 exchange rate between the peso and the dollar) that had been imposed in 1991 to end hyperinflation and that had eliminated the country’s ability to adjust its exchange rate in response to the worsening terms of trade during the 1990s commodity downturn. When the regime collapsed, devaluation was approximately 70 percent, savings held in dollar-pegged pesos were converted to devalued pesos (the corralito bank freeze), and the political system cycled through five presidents in two weeks.

The subsequent restructuring took until 2005, with a second exchange in 2010, and achieved a haircut of approximately 70 percent in NPV terms — among the largest in sovereign debt history. The holdout litigation led by NML Capital (discussed in Part 2) blocked Argentina from capital markets for fourteen years. When Argentina settled with holdouts in 2016, it did so by borrowing $16 billion in new Eurobonds — the largest single EM bond issuance in history — to pay off creditors who had refused to accept the restructuring. The fiscal cost of the holdout settlement exceeded the NPV savings of the haircut achieved in the restructuring itself.

By 2020, Argentina was defaulting again — this time on $65 billion in bonds issued in the aftermath of the previous restructuring, in a process that completed in four months because the lessons of 2001 had been sufficiently internalized by both debtor and creditors to allow a faster process. The 2020 restructuring is genuinely regarded as a functional example of how a large sovereign debt negotiation can work when creditors are primarily private bondholders rather than bilateral governments: concentrated, represented by banks that understand the process, and motivated to resolve quickly rather than litigate.

The problem is that Argentina’s success in completing the 2020 restructuring quickly was a function of the composition of its creditor base — predominantly private — in a way that is not replicable for countries like Zambia, where the creditor base is fragmented across bilateral and private categories with different legal positions and different incentives.

The HIPC Relief Illusion#

The Heavily Indebted Poor Countries (HIPC) Initiative, launched in 1996 and expanded in 1999, was the most comprehensive sovereign debt cancellation program in history. By 2006, it had cancelled approximately $130 billion in debt for thirty-nine countries, reducing their debt-to-GDP ratios to levels the IMF assessed as sustainable.

By 2015, seventeen of the thirty-nine HIPC graduates had re-accumulated public debt above 50 percent of GDP — the lower end of the IMF’s high-risk threshold range. The IMF’s own 2016 retrospective assessment of the HIPC Initiative attributed the reaccumulation to “renewed external borrowing at commercial terms, often in foreign currency, to fund infrastructure and budget support in the context of commodity price-driven revenue growth that subsequently reversed.”

This is an accurate description and a revealing one. The reaccumulation followed the same structural logic as the original accumulation: commodity-dependent revenue, dollar-denominated borrowing, external rate setting, exposure to commodity and currency shocks. Cancelling the debt stock without addressing those structural dynamics produces a debt-free version of the same structure — which generates new debt by the same mechanism within a decade.

The HIPC Initiative was the most generous act of collective creditor action in sovereign debt history. It was not sufficient because relief without structural change does not alter the path that produced the distress.

References#

- IMF. “Zambia: Request for an Extended Credit Facility Arrangement.” IMF Country Report No. 22/292, 2022.

- IMF. “G20 Common Framework — Status Reports.” 2022–2024.

- Southern District of New York. NML Capital Ltd. v. Republic of Argentina. 2012.

- Argentine Ministry of Finance. “2020 Debt Restructuring.” Press releases, 2020.

- IMF Independent Evaluation Office. “The IMF and the Crises in Greece, Ireland, and Portugal.” 2016.

- IMF. “HIPC Initiative: Status of Implementation.” Various years. https://www.imf.org/external/np/hipc/

- Reinhart, Carmen M., and Kenneth S. Rogoff. This Time Is Different. Princeton University Press, 2009.

- Eurodad. “The Debt Trap: How Zambia’s Debt Crisis Unfolded.” 2022.

- JP Morgan. EMBI+ Sovereign Spread Data (via Bloomberg terminal), 2019–2025.