The Committee That No Longer Exists#

Between 1956 and 2000, when a developing country faced a sovereign debt crisis, the international response followed a predictable architectural logic. The debtor would approach the Paris Club — an informal group of creditor governments meeting in the French Treasury building — which would agree to restructure bilateral debt on standard terms. The Paris Club agreement would then serve as a precedent that private creditors were expected to follow under the “comparability of treatment” principle. The IMF would provide a stabilization program. Multilateral creditors (World Bank, regional development banks) would provide new concessional lending. Within eighteen to twenty-four months, a restructuring would typically be complete.

That architecture no longer describes the world it was built to govern.

The Transformation of the Creditor Landscape#

Paris Club in Decline#

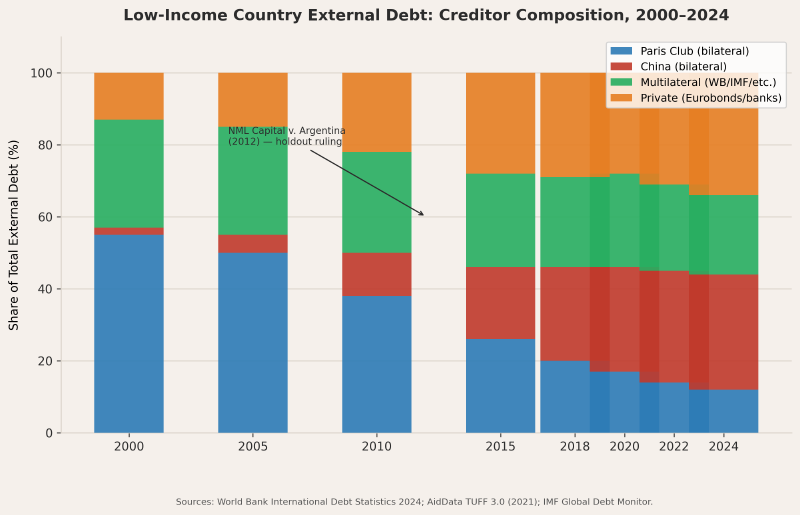

The Paris Club held approximately 55 percent of low-income country external debt in 2000. That share has declined every year since. By 2024 it stood at approximately 12 percent. The decline reflects two developments: the graduation of many countries from bilateral dependence on Western aid-linked loans as they accessed capital markets, and the entry of a new bilateral lender on a scale that the Paris Club has no precedent for absorbing.

The Paris Club’s institutional authority derived from its comprehensiveness. When it set terms, it was setting terms for the majority of bilateral creditors simultaneously. Comparability of treatment was enforceable because Paris Club members held most of the debt. When Paris Club members hold 12 percent of the debt, comparability of treatment becomes a request, not a mechanism.

China’s Bilateral Lending Architecture#

AidData’s “Banking on the Belt and Road” dataset — a compilation of 13,427 Chinese-financed development projects between 2000 and 2021, drawn from official records, parliamentary filings, and procurement databases across 165 countries — provides the most detailed available picture of how Chinese development finance works.

The aggregate figure is $843 billion across two decades. The average interest rate on Chinese bilateral loans, where disclosed, is approximately 6.0 percent — compared to approximately 1.1 percent for Western Official Development Assistance. The average maturity is approximately ten years, compared to approximately twenty-eight years for traditional Paris Club bilateral loans. Those two facts alone — three times the interest rate at less than half the maturity — produce a substantially higher annual debt service burden than equivalent amounts borrowed under Paris Club terms.

The contractual structure of Chinese loans has features that the AidData analysis describes as “unusual by international standards.” Fifty-two percent of the loan contracts it analyzed include cross-default clauses, under which default on any Chinese loan triggers default on all Chinese loans simultaneously — a provision that limits the debtor’s ability to prioritize urgency in a crisis. Thirty-seven percent include confidentiality clauses that prohibit the borrowing government from disclosing the terms of the loan to other creditors — a provision that directly obstructs the transparency required for coordinated restructuring.

These are not evidence of malice. They are evidence of a lending architecture designed for a bilateral relationship between China and individual countries, without reference to the multilateral creditor coordination framework that the Paris Club represents. China lends through policy banks — China Development Bank, China Export-Import Bank — that are not members of the Paris Club, have no institutional history of multilateral debt restructuring, and have no legal obligation to participate in it.

The Private Creditor Revolution#

Private bondholders — investment banks, asset managers, hedge funds — held approximately 8 percent of low-income country external debt in 2000. By 2024 that share had risen to approximately 34 percent, driven by the Eurobond market boom of the 2010s.

The expansion was encouraged by the international financial architecture itself. The IMF’s Debt Sustainability Analysis framework, in the years after the HIPC Initiative reduced debt burdens, signaled that many African countries had “improved” their debt profiles. International credit rating agencies issued investment-grade or near-investment-grade ratings. Sub-Saharan African countries issued $100 billion in Eurobonds between 2007 and 2019. The market described it as “frontier market growth.” The debtor countries described it as access to capital at last.

The terms were not favorable in the way that access-to-capital language implies. Ghana’s first Eurobond in 2007 carried a yield of 8.5 percent over ten years. Zambia’s 2012 issuance carried 5.6 percent — but its 2015 issuance carried 8.97 percent and its 2021 issuance was trading at yields exceeding 15 percent before default, meaning the market was pricing default as highly probable for at least a year before it occurred.

Private creditors have no obligation to participate in Paris Club restructuring. They have no obligation to participate in the G20 Common Framework. Their restructuring obligation is purely contractual — what the bond indenture specifies and what a court will enforce. And courts will enforce it.

The NML Capital Decision and Its Consequences#

In 2001, Argentina defaulted on $100 billion in sovereign debt — the largest default in history at the time. Over the following decade, Argentina restructured approximately 93 percent of that debt through two exchange offers that gave creditors reduced-value bonds in exchange for old bonds. Most creditors accepted. Some did not.

NML Capital, a hedge fund, purchased Argentine bonds at a deep discount in the secondary market after the default and refused to participate in either restructuring. It then sued Argentina in US federal court for full face value plus interest, under the pari passu clause standard in sovereign bond contracts.

In 2012, Judge Thomas Griesa of the Southern District of New York ruled that Argentina could not make payments to the restructured bondholders — those who had accepted the haircut — without simultaneously paying NML Capital in full. Argentina’s bonds were cleared through US financial infrastructure, and Judge Griesa had jurisdiction over that infrastructure. Argentina was effectively locked out of the US financial system for fourteen years. The restructured bondholders, who had accepted haircuts in exchange for debt service payments, received nothing either.

The ruling established that holdout litigation is viable as a strategy for private creditors. A fund that buys distressed debt at ten cents on the dollar, refuses to participate in a restructuring, and sues for par value can in principle receive a multiple of its investment, enforced by a US court, against a country with no mechanism to compel the holdout to participate. The calculus for hedge funds acquiring distressed sovereign debt changed permanently.

The practical consequence is not only the holdout threat itself but the shadow it casts over restructuring negotiations. Debtor countries know that agreeing to a haircut with 90 percent of creditors does not solve the problem if the remaining 10 percent can sue in New York or London and block payments to the cooperating majority. Getting every creditor class to agree to the same terms simultaneously — across Paris Club members, Chinese policy banks, and private bondholders with different legal rights and interests — is the challenge the Common Framework was created to solve.

It has not solved it.

The G20 Common Framework: 32 Months for Zambia#

The G20 Common Framework for Debt Treatments Beyond the DSSI was announced in November 2020. It was designed to coordinate debt restructuring across all creditor classes — bilateral creditors including China, private creditors, multilateral institutions — in a single process, rather than the sequential bilateral negotiation that the transformation of the creditor landscape had made unworkable.

As of March 2026, four countries have applied: Chad, Ethiopia, Zambia, and Ghana. The results tell a story about institutional design.

Zambia applied in November 2020. A preliminary restructuring agreement with official creditors (the “Official Creditor Committee,” including China) was reached in June 2023 — thirty-two months later. The final deal with private creditors followed in September 2023, forty-six months after the application. During those forty-six months Zambia was locked out of international capital markets, could not issue bonds, could not attract commercial investment in conditions of legal uncertainty, and watched its currency depreciate 44 percent.

Ethiopia applied in February 2021, complicated by a civil war that made revenue projections unreliable. A preliminary agreement was reached in December 2023 — thirty-four months.

Ghana applied in January 2023. A bilateral creditor agreement was reached in January 2024 — twelve months, faster than its predecessors, partly because the process had been somewhat refined by experience.

Chad entered the process in 2021 for oil-collateralized debt to Glencore — a commodity trader, not a traditional creditor — and reached an initial agreement by 2022, though subsequent complications required further negotiation.

The eighty or more countries eligible for the Common Framework but not applying have their reasons. The IMF conditionality attached to the program is the primary deterrent: applying triggers an IMF program, and the conditions attached to IMF programs are contractionary by design, at precisely the moment when contraction is most politically difficult. The stigma of applying — the market signal that a country is in distress — increases borrowing costs even before restructuring is complete. And the process takes too long to be practically useful for a country facing a liquidity crisis that could be resolved faster through bilateral negotiation.

The Common Framework is not a failure in the sense of having been designed wrong. It is a failure in the sense of having been designed for a creditor landscape that had already ceased to exist by the time the framework was launched: one in which bilateral creditors coordinate swiftly, private creditors follow their lead, and the debtor’s primary concern is negotiating the size of the haircut rather than the number of months in legal limbo.

The architecture that replaced the Paris Club was built for bilateral relationships. It produces bilateral outcomes, bilateral timelines, and bilateral costs — while the debtor cannot borrow, cannot plan, and watches its SSDR rise.

References#

- AidData. “Banking on the Belt and Road: Insights from a New Global Dataset of 13,427 Chinese Development Projects.” William & Mary, 2021. https://www.aiddata.org/publications/banking-on-the-belt-and-road

- Gelpern, Anna, et al. “How China Lends.” AidData / PIIE / Kiel / CGD, 2021. https://www.aiddata.org/publications/how-china-lends

- World Bank International Debt Statistics 2024. https://data.worldbank.org/topic/external-debt

- IMF. “G20 Common Framework for Debt Treatments — Progress Reports.” 2022–2024.

- Southern District of New York. NML Capital Ltd. v. Republic of Argentina. 699 F.3d 246 (2d Cir. 2012).

- Eurodad. “Story of a Debt Crisis: Zambia’s Road to Default.” 2021. https://www.eurodad.org

- Paris Club. Official website and treatment statistics. https://www.clubdeparis.org

- IMF. “How the IMF Supports Countries’ Fight Against Debt Distress.” 2023. https://www.imf.org