In 1966, Botswana achieved independence as one of the poorest countries on earth. GDP per capita was approximately $70. There was one secondary school in the country. The main export was cattle, and the main employer was the colonial-era administrative apparatus being handed over to a government that had almost no civil servants trained to operate it. One year later, a geologist working for De Beers found diamonds at Orapa, in the Kalahari. The subsequent negotiations — conducted by the incoming president, Seretse Khama, and his finance minister, Quett Masire — set the ownership structure at 50% Botswana government, 50% De Beers, and established the principle that diamond revenues would be invested in infrastructure, education, and a foreign exchange reserve fund rather than distributed immediately to political constituencies. Over the following five decades, Botswana became the fastest-growing economy in the world by average annual GDP growth rate. It is still diamond-dependent. The difference between Botswana and Nigeria is not the resource. It is the deal, the institution, and what happened next.

Key Takeaways#

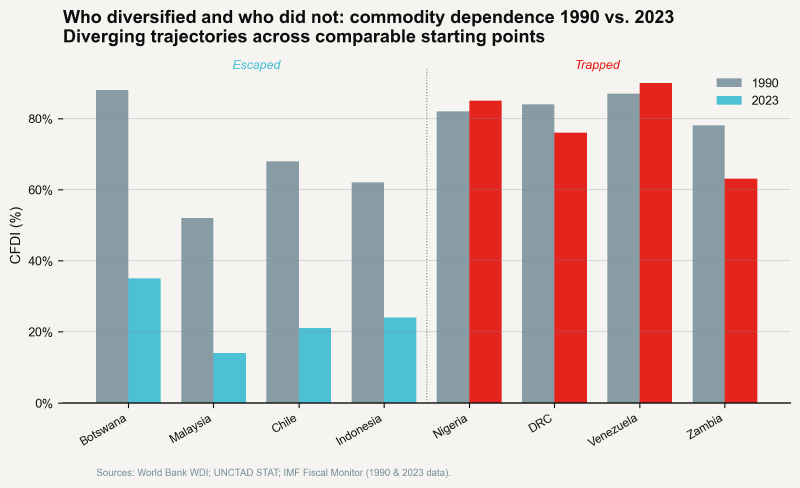

- Botswana, Malaysia, Chile, and Indonesia all began the 1970s with commodity dependence indices above 60%. By 2023, Malaysia’s CFDI had fallen to 14, Chile’s to 21, and Indonesia’s to 24. Botswana remains at approximately 35% — down from 88% at peak diamond dependence in the 1980s. All four built sovereign wealth or stabilization funds during commodity booms.

- The commodity stabilization fund is the single most consistently documented escape mechanism in the historical data. It converts a price windfall — which will end — into a permanent asset. Chile’s Copper Stabilization Fund allowed its government to run a fiscal stimulus of approximately 4% of GDP during the 2008–2009 global crisis, when commodity-dependent countries without such funds were cutting budgets.

- Malaysia’s successful diversification from rubber and tin to electronics and services between 1970 and 2000 was explicitly state-led: the New Economic Policy directed commodity revenues into manufacturing development zones, a national car project (Proton), and an engineering university built to supply the Penang electronics corridor. No market mechanism produced these outcomes. A development state designed and funded them.

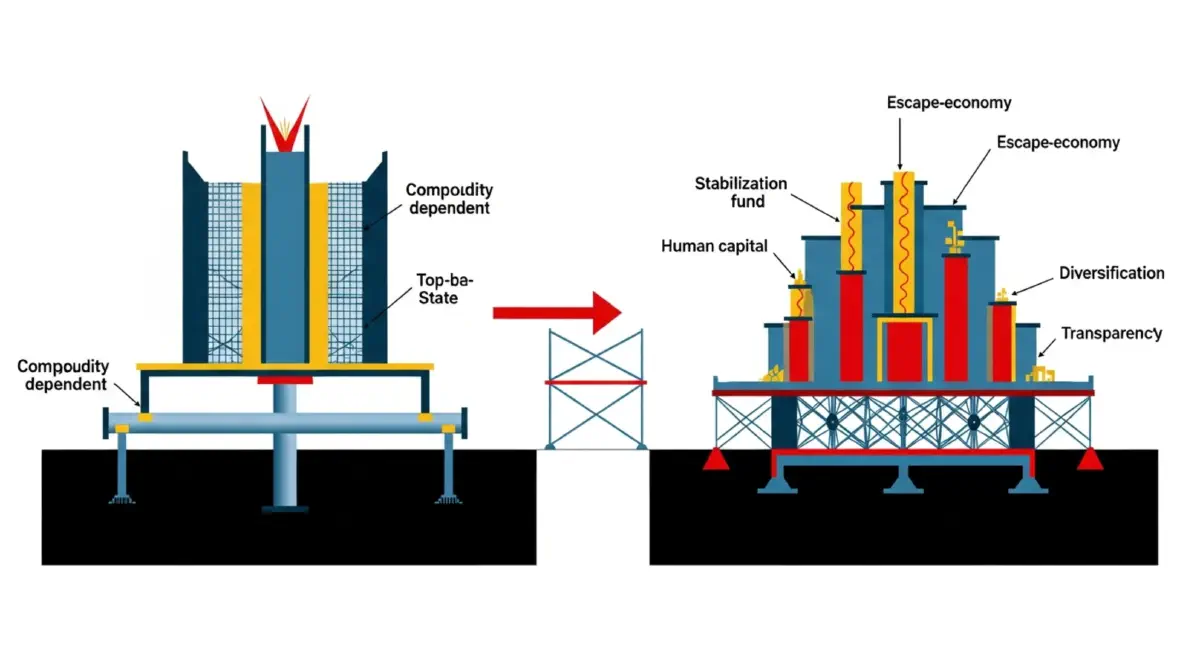

- The five conditions consistently associated with durable escape from commodity dependence are: (1) a commodity revenue stabilization mechanism established during the first windfall; (2) non-commodity domestic revenue mobilization above 18% of GDP; (3) human capital investment sustained above 5% of GDP throughout the transition period; (4) export diversification into at least two non-commodity sectors before the first major price collapse; and (5) transparent revenue management, measured by functional compliance with EITI standards or equivalent.

- Democracy is a correlate but not a strict prerequisite of escape. Botswana has been consistently democratic since independence. Chile escaped under Pinochet’s dictatorship — a fact that complicates any simple institutional narrative. Malaysia escaped under Mahathir’s semi-authoritarian development state. The causal mechanism appears to be accountability for commodity revenue use, not the specific institutional form through which that accountability operates.

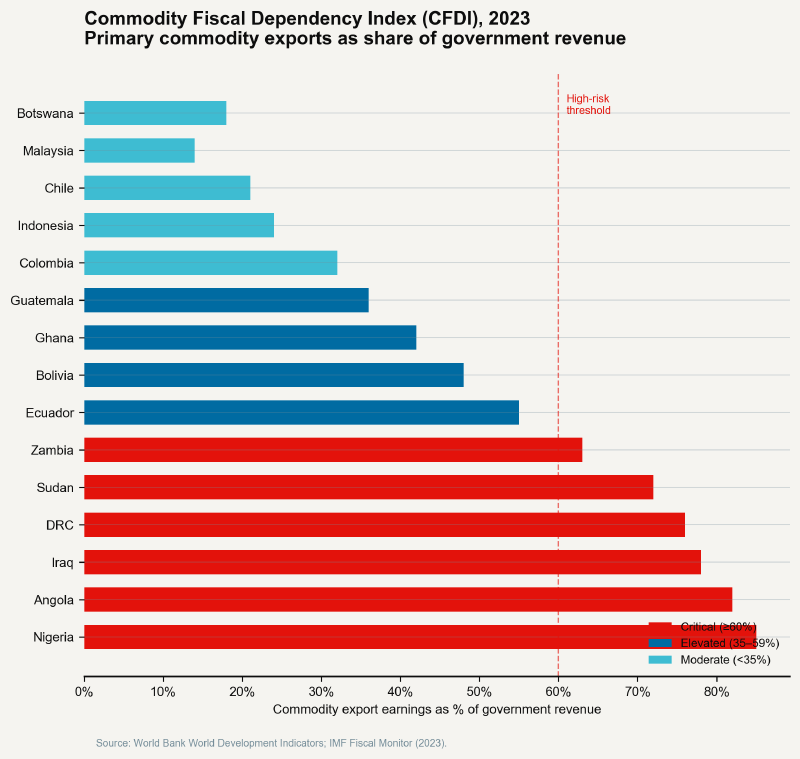

- The EITI (Extractive Industries Transparency Initiative), which requires member countries to publish reconciled data on what governments receive from extractive industries versus what companies report paying, is correlated with a 25% reduction in commodity revenue leakage among full-compliance members. Transparency alone does not produce escape. But its absence reliably produces the full commodity trap.

What Botswana Did Differently on the First Day#

The decision that set Botswana on a different trajectory from resource-rich neighbors was not made in a flash of civic virtue. It was made under specific political and institutional conditions that need to be accurately identified if the lesson is to be transferable.

Seretse Khama negotiated the Debswana joint venture from a position of near-total weakness. De Beers held all the technical knowledge, all the capital equipment, and all the marketing infrastructure. Botswana held the land and the legal sovereignty — which, in 1967, was not obviously valuable. Khama did four things that, individually, were not unprecedented, but in combination produced an outcome no Sub-Saharan African commodity economy had previously achieved.

He established a 50% government ownership stake from the beginning, rather than accepting the royalty-only arrangement De Beers initially offered. He deposited diamond revenues into a dedicated Pula Fund rather than the general budget. He contracted technocrats from Botswana’s small civil service — supplemented, in the early years, by expatriate economists from the World Bank and UK — to manage the fund according to explicit rules rather than political direction. And he built a political coalition that treated the diamond revenue as national patrimony rather than factional spoils.

None of these decisions were costless. The 50% ownership stake reduced Botswana’s immediate revenue in the early years, because De Beers retained 50% of profits during the capital-intensive development phase. The Pula Fund delayed consumption spending that could have generated immediate political support. The technocratic management structure created a class of public servants more accountable to macroeconomic rules than to the incumbent political faction — a constraint Khama accepted because the alternative, visible in neighboring Zaire, was worse.

The Chilean Model: Rules, Not People#

Chile’s escape from copper dependence took a different institutional form — one that demonstrates that the mechanism can operate under very different political regimes. Chile’s copper sector was nationalized by Allende in 1971, initially celebrated as a break from the commodity trap. CODELCO, the state copper company that emerged, did indeed capture more of the copper rent for the Chilean state than the pre-nationalization royalty structure. But the question of what the state would do with the rent remained open and politically contested.

The decisive innovation was the Structural Fiscal Balance Rule, enacted in 2000 under President Ricardo Lagos but building on framework thinking developed through the 1990s. The rule requires the Chilean government to set its annual budget based on the long-run structural level of copper revenues — not the actual price. When copper prices are above the long-run trend, the surplus goes into the Economic and Social Stabilization Fund. When prices are below trend, the Fund can be drawn down to maintain spending commitments. The rule depoliticizes the copper windfall: neither the mining ministry nor the finance ministry can decide to spend the excess. The mechanism makes that decision automatically.

The practical consequence was visible during the 2008–2009 global financial crisis. When commodity prices collapsed and global demand contracted, Chile — unlike virtually every other commodity-dependent economy in Latin America — was able to increase government spending by approximately 4% of GDP without issuing debt. The Stabilization Fund had accumulated $20 billion during the preceding copper boom. Chile ran structural counter-cyclical policy because its fiscal rules preserved the option to do so.

Malaysia: The State That Diversified Itself#

Malaysia’s trajectory is the most instructive for lower-income commodity-dependent countries because it demonstrates that diversification does not require democratic accountability of the Chilean or Botswanan type. What it requires is a state capable of making long-run investment decisions against immediate political pressures — and willing to absorb the short-run costs of protecting infant industries.

In 1970, rubber and tin accounted for 52% of Malaysian export earnings. The New Economic Policy, launched that year, was prompted by the 1969 race riots — but its economic logic was explicitly developmental: use commodity revenues to build a manufacturing base that would eventually replace commodity dependence. The Penang Industrial Zone, established in 1970, attracted Intel, Motorola, and National Semiconductor — companies that would not have come without the infrastructure investment, the industrial policy protection, and the engineering university that supplied skilled labor.

Proton, the Malaysian national car company established in 1983, is routinely cited as an example of failed industrial policy. By pure market efficiency metrics, the critique is fair: Proton cars were more expensive and technically inferior to Japanese imports for most of their history, and the protection they received imposed real costs on Malaysian consumers. But the critique misses the function. Proton built an automotive engineering ecosystem in Malaysia — suppliers, toolmakers, calibration labs, engineers — that existed because the state decided it should exist and financed its creation. Malaysia today exports $82 billion annually in electrical and electronic products. The Proton engineers and their suppliers helped build that ecosystem.

The Five Conditions and What They Actually Require#

The data on successful commodity exits converges on five structural conditions. None of them are impossible. All of them require political decisions that the immediate incentive structure in a commodity-dependent state works against.

The first condition — a commodity stabilization fund established during the first windfall — is politically costly precisely when it is most necessary. During a commodity boom, the pressure to spend current revenue is intense: debts need servicing, political coalitions need material rewards, infrastructure backlogs need addressing. The fund represents a refusal of these claims in the short term in exchange for fiscal flexibility in the long term. Governments that can make this refusal have generally done so because institutional rules — like Chile’s structural balance rule, or Botswana’s Pula Fund mandate — make the refusal automatic rather than discretionary.

The second condition — non-commodity domestic revenue mobilization above 18% of GDP — is the most technically demanding. Building a tax administration capable of assessing and collecting corporate income tax, VAT, and personal income tax from a predominantly informal economy requires a decade of institution-building. Countries that invested in this during commodity booms — Botswana, Chile, Malaysia — found that when commodity prices fell, they had a revenue base that did not disappear with the price. Countries that did not invest — Nigeria, Zambia, Sudan — found that their fiscal systems were co-terminous with the commodity cycle.

The remaining three conditions — human capital investment, export diversification before the first price collapse, and transparent revenue management — share a common feature: they all require deferring immediate political rewards for future economic resilience. The commodity curse is, at its root, a problem of political time horizons colliding with economic time horizons. The politicians who make the investments necessary for escape will generally not be in office when the diversification delivers its returns. The structure of democratic and authoritarian accountability alike produces incentives oriented toward short-term distribution. Escape requires building institutional mechanisms that outlast and constrain the politicians within them.

That Botswana, Chile, Malaysia, and Indonesia all found their different paths to those mechanisms — through different political systems, different historical moments, different cultural contexts — is the most important data point in this entire series. The commodity curse is not destiny. It is a structure. Structures can be built differently.

References#

Acemoglu, D., Johnson, S., & Robinson, J. A. (2003). An African success story: Botswana. In D. Rodrik (Ed.), In search of prosperity: Analytic narratives on economic growth (pp. 80–119). Princeton University Press.

Frankel, J. A. (2011). A solution to fiscal procyclicality: The structural budget institutions pioneered by Chile. NBER Working Paper No. 16945. https://doi.org/10.3386/w16945

Jomo, K. S. (1990). Growth and structural change in the Malaysian economy. Macmillan Press.

IMF. (2012). Macroeconomic policy frameworks for resource-rich developing countries. International Monetary Fund. https://www.imf.org/en/Publications/Policy-Papers/Issues/2016/12/31/Macroeconomic-Policy-Frameworks-for-Resource-Rich-Developing-Countries-PP4702

Extractive Industries Transparency Initiative. (2024). EITI global data. https://eiti.org/data

World Bank. (2024). World development indicators: Malaysia, Chile, Botswana, Indonesia 1970–2023. https://databank.worldbank.org

Rodrik, D. (2007). One economics, many recipes: Globalization, institutions, and economic growth. Princeton University Press.

UNCTAD. (2023). State of commodity dependence 2023. https://unctad.org/publication/state-commodity-dependence-2023