In 1983, Ghana was in fiscal collapse. The cocoa price had fallen by more than half over five years. Drought had destroyed food crops. The currency was worthless. Inflation exceeded 120%. President Jerry Rawlings, who had come to power in a coup the previous year, signed a structural adjustment agreement with the IMF and World Bank. Over the following decade, Ghana implemented some of the most comprehensive reforms in Sub-Saharan Africa: it liberalized its exchange rate, restructured the Cocoa Marketing Board, removed input subsidies, privatized state enterprises, and opened its markets to foreign competition. Economic growth returned. By the mid-1990s Ghana was regularly cited by the Bretton Woods institutions as a structural adjustment success story. What was less frequently cited was that by 2022, the farmgate price paid to Ghanaian cocoa farmers remained approximately 30% of the world price — a gap that had persisted through every round of reform, every wave of liberalization, and every tranche of World Bank support. The structural adjustment had reformed the state. It had not escaped the commodity trap.

Key Takeaways#

- IMF structural adjustment programs applied to commodity-dependent economies between 1980 and 2010 consistently included three elements: elimination of input subsidies for smallholder farmers, removal of agricultural marketing boards, and currency devaluation. All three reduced smallholder incomes at the same moment that commodity price collapses had already reduced them.

- The IMF’s Independent Evaluation Office’s 2019 review of its engagement with Sub-Saharan Africa found that 60% of growth projections embedded in structural adjustment programs were not met. The programs worked as fiscal adjustment instruments. They did not work as development instruments.

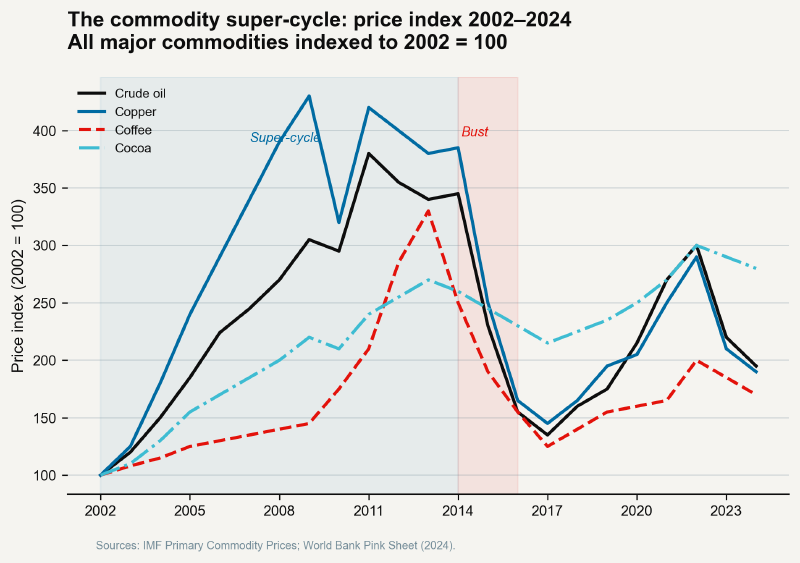

- In Côte d’Ivoire — the world’s largest cocoa producer — every major political rupture between 1999 and 2011 was directly preceded by a commodity price shock followed by a fiscal squeeze. The 1999 coup, the 2002 civil war, and the 2010–2011 post-election crisis all followed, with a lag of 12 to 24 months, from cocoa price collapses that reduced government revenues and triggered IMF-mandated austerity.

- The standard structural adjustment prescription for commodity-dependent economies required liberalization before diversification infrastructure existed. Removing the cocoa marketing board in Côte d’Ivoire exposed farmers to world price volatility before Ivorian agribusiness had developed the processing capacity, cold chain infrastructure, or value-added manufacturing that could have captured a larger share of the cocoa value chain.

- Tanzania’s structural adjustment program, beginning in 1986, eliminated the cooperative marketing structure that had buffered smallholder coffee and tea farmers from direct price risk. Coffee area under cultivation declined 15% in the decade following the reform as smallholders switched to lower-risk food crops. The adjustment had increased economic efficiency at the expense of the commodity export base it was designed to protect.

- The literature on structural adjustment and commodity economies has reached a reasonably settled conclusion: the programs were effective at restoring fiscal balance in the short term, and ineffective at producing durable economic diversification. They treated the symptom and left the cause untouched.

What Structural Adjustment Was Designed to Do#

To evaluate structural adjustment fairly, you need to understand what it was designed to solve — and why that problem is real. By the late 1970s and early 1980s, many commodity-dependent economies in Sub-Saharan Africa and Latin America had accumulated fiscal positions that were arithmetically unsustainable. State-owned enterprises ran chronic deficits. Agricultural marketing boards bought commodities from farmers at above-market prices and sold them at below-market prices — the gap financed by government borrowing. Input subsidies claimed budget shares that crowded out infrastructure investment. Exchange rates were fixed at levels that overvalued the currency, making exports uncompetitive and supporting cheap imports that damaged domestic industry.

The standard IMF diagnosis was largely correct as a description of these problems. The prescription — liberalize, privatize, cut subsidies, float the currency — was a reasonable first-order correction for some of them. The difficulty was that the prescription was applied without regard for sequencing, and without building the replacement institutions that smallholder agricultural economies required before the existing protection was removed.

The Sequencing Problem#

The sequencing problem is most clearly illustrated in Tanzania. The country’s cooperative system — KNCU for coffee, TPGA for tea — was bureaucratic, corrupt in places, and undeniably inefficient. It charged marketing margins that the farmers notionally funded. But it also provided extension services, guaranteed purchases at a floor price, and gave smallholders access to seasonal credit for inputs. When the cooperative structure was dismantled under the 1986 and 1991 structural adjustment agreements, what replaced it was — nothing. Private buyers moved into some areas; in others, farmers had no reliable buyer for their output and no reliable credit source for their inputs.

Tanzanian smallholder coffee area under cultivation fell an estimated 15% between 1990 and 2000. This was not because coffee was uneconomic. It was because the marketing risk, which had previously been borne collectively by the cooperative, was now borne entirely by individual smallholder farmers who did not have the financial resilience to absorb price shocks. The rational response — growing cassava instead — was individually sensible. It was also collectively devastating to foreign exchange earnings, which fell, which tightened the fiscal position, which triggered the next round of adjustment measures.

The Côte d’Ivoire Pattern#

Côte d’Ivoire provides the most politically consequential illustration of what happens when commodity price shocks interact with structural adjustment in a setting where no alternative fiscal base has been developed. The country is the world’s largest cocoa producer, accounting for approximately 40% of global supply. When the global cocoa price fell sharply in 1987, and again in the early 1990s, the government of Félix Houphouët-Boigny used price support schemes — exactly the kind of intervention the World Bank was recommending against — to buffer farmers from the impact. The schemes were expensive, and they contributed to the debt accumulation that ultimately forced liberalization.

When liberalization came in 1999 — the Caistab, the cocoa and coffee marketing board, was abolished that year under World Bank pressure — the Ivorian economy was exposed to raw cocoa price volatility without the processing and value-added infrastructure that would have allowed the country to capture a larger share of the value chain. Côte d’Ivoire grows 40% of the world’s cocoa but manufactures approximately 6% of the world’s chocolate. The value addition occurs in Switzerland, Belgium, and the Netherlands. The adjustment did not change this ratio.

What the 1999 liberalization did change was the government’s fiscal position following each cocoa price movement. Within months of the reform, the government faced a revenue shortfall it could not absorb through price support. In December 1999, a military coup removed President Henri Konan Bédié — the first democratic transfer in Ivorian history reversed. The coup was triggered by a salary dispute with military officers. The salary dispute was a fiscal dispute. The fiscal dispute was rooted in cocoa.

The IMF’s Own Assessment#

It is worth noting that the most damaging critique of structural adjustment’s results in commodity-dependent economies does not originate with development economists hostile to the Bretton Woods institutions. It originates from the IMF’s own Independent Evaluation Office, which reviewed the institution’s engagement with Sub-Saharan Africa in 2019.

The IEO found that in 73 programs implemented in commodity-dependent Sub-Saharan African economies between 1990 and 2015, the median growth projection embedded in program documents exceeded actual growth outcomes by 2.1 percentage points per year. Over a five-year program, this compounds to a growth shortfall of approximately 10 percentage points. The fiscal targets were met more often than the growth targets — the programs were effective at reducing government deficits. But fiscal consolidation achieved by cutting health and education expenditure is not a development strategy. It is an accounting correction.

The IEO report noted that programs routinely required reductions in the social spending that provided the human capital investment commodity-dependent economies needed to diversify. The average health and education spending reduction across the 73 programs was 2.8% of GDP — a number that sounds modest until you note that many of these countries were already spending less than 5% of GDP on health and education combined. A 2.8-point cut from a 4-point base is a 70% reduction in the fiscal space available for human development.

The Problem Is the Diagnosis#

The structural adjustment era’s fundamental error was not the specific policy instruments — some of which were genuinely necessary — but the implicit diagnosis that animated them. The programs treated commodity dependence as a consequence of bad policy: excessive state intervention, overvalued currencies, market-distorting subsidies. Remove the bad policy, the diagnosis suggested, and the underlying economy would diversify through the market mechanism.

The historical evidence does not support this diagnosis. Commodity dependence is not caused by bad policy. It is a structural feature of an economy’s position in the international division of labor — a position shaped by colonial-era specializations, geographic endowments, global demand patterns, and the capital and technology requirements of the manufacturing sector that diversification requires. Removing the marketing board does not spontaneously generate the manufacturing base. Floating the currency does not automatically make exports competitive if no manufactured exports exist to compete. Cutting fertilizer subsidies does not make smallholder farmers less dependent on commodity prices; it makes them more vulnerable to them.

The countries that escaped the commodity curse — the subject of Part 5 — did not escape through deregulation. They escaped through deliberate, state-led construction of alternative economic bases, funded during commodity booms, institutional development during stability, and protected through mechanisms that the structural adjustment prescription explicitly forbade.

References#

IMF Independent Evaluation Office. (2018). Structural conditionality in IMF-supported programs: Evaluation update. IEO. https://ieo.imf.org/en/evaluations/updates/structural-conditionality-in-imf-supported-programs-eval

Stiglitz, J. E. (2002). Globalization and its discontents. W.W. Norton.

Fairtrade International. (2022). Monitoring the scope and benefits of Fairtrade: Cocoa data 2022. Fairtrade International.

Mkandawire, T., & Soludo, C. C. (1999). Our continent, our future: African perspectives on structural adjustment. IDRC/CODESRIA.

World Bank. (2024). Côte d’Ivoire: GDP growth and fiscal balance 1985–2000. World Development Indicators. https://databank.worldbank.org

Chang, H.-J. (2002). Kicking away the ladder: Development strategy in historical perspective. Anthem Press.

Loxley, J. (1990). Structural adjustment in Africa: Reflections on Ghana and Zambia. Review of African Political Economy, 17(47), 8–27.

IMF. (2014). Government finance statistics manual 2014. International Monetary Fund. https://www.imf.org/en/Publications/Manuals-Guides/Issues/2016/12/31/Government-Finance-Statistics-Manual-2014-41592