In the opening scene of Mission: Impossible III, the audience learns for the first time what the acronym IMF stands for in the film series: the Impossible Mission Force. It was a long-standing puzzle. In a franchise built on the implausible, the name of the agency conducting the implausible missions had been, for decades, left unexplained.

The real IMF — the International Monetary Fund — has a different kind of impossibility attached to it. In Seoul in late 1997, as a currency crisis that began in Thailand swept through South Korea, the country signed an agreement with the Fund that required, among other things, generating a budget surplus equivalent to 1% of GDP. The economy was already contracting sharply. Firms were failing at the rate of more than a hundred a day. Unemployment was about to nearly triple. In these conditions, Korean housewives launched a campaign of voluntary austerity — cooking smaller meals at home to reduce household spending and stabilize the national accounts. A Financial Times correspondent covering Korea dismissed the campaign as economically illiterate, explaining that such spending cuts would deepen the recession by further reducing demand. The correspondent was right. The IMF was requiring the Korean government to do, at a national scale, exactly what the housewives were doing voluntarily.

Key Insights#

- During Korea’s financial miracle years, average annual inflation was 17.4% in the 1960s and 19.8% in the 1970s — rates higher than several Latin American countries at the time — and per capita income grew at 7% annually throughout this period.

- Brazil grew at 4.5% per capita annually in the 1960s–70s with average inflation of 42%; after adopting IMF-style macroeconomic orthodoxy in the 1990s, it averaged 7.1% inflation and only 1.3% per capita growth.

- World Bank research confirms no systematic negative correlation between inflation and growth below 40%; below 20%, higher inflation is actually associated with higher growth in some periods.

- South Africa’s real interest rates of 10–12% in the late 1990s and early 2000s reduced the investment rate from 25% to 15% of GDP; since most non-financial firms earn profit rates of 3–7%, real interest rates above that threshold make borrowing to invest economically irrational.

- When Korea signed an IMF agreement in December 1997, it was required to generate a budget surplus despite being in deep recession; Koreans began calling the IMF “I’m Fired” as unemployment nearly tripled in early 1998.

- When Sweden faced a comparable financial crisis in the early 1990s — caused by the same mechanism of premature capital market opening — it ran budget deficits equivalent to 8% of GDP; Korea was permitted deficits of only 0.8%.

- Between 1960 and 1973, the peak of the post-war growth boom, average real interest rates in rich countries were below 3% in Germany, France, the USA, and Sweden, and negative in Switzerland.

The inflation numbers do not match the theory#

The standard neo-liberal argument against inflation is simple and, up to a point, correct. Very high inflation — above, say, 40% per year — makes rational long-range calculation impossible, destroys confidence in the currency as a unit of account, and discourages the investment on which growth depends. This was Argentina’s experience in the late 1980s, when annual inflation reached 20,000% during one twelve-month period and supermarkets used chalkboards instead of price labels because prices changed too quickly to print. That kind of inflation is genuinely destructive.

But the argument that lower inflation is always better — that a 1–3% target is superior to a 5% target, which is superior to a 10% target, and so on — is not supported by the data. World Bank economists Michael Bruno and William Easterly examined the relationship between inflation and growth across a large sample of countries and found no systematic negative correlation below 40%. Below 20%, higher inflation was actually associated with higher growth during some periods. These findings did not produce a revision of the standard prescription.

Brazil grew at 4.5% per capita annually during the 1960s and 1970s, when its average inflation rate was 42% per year. South Korea grew at 7% per capita annually during its miracle decades, with inflation averaging 17–20%. In the 1960s, Korea’s inflation rate was higher than five Latin American countries. In the 1970s, it was higher than Venezuela, Ecuador, and Mexico. None of this accords with the cultural stereotype of the disciplined, prudent East Asian economy versus the reckless Latin one. The stereotype is a post-hoc narrative applied to the outcome; it does not describe the conditions that produced the outcome.

Figure 1: The horizontal axis shows average annual inflation rate; the vertical axis shows per capita growth. High-growth periods cluster across a wide range of inflation rates — from Japan at 5.5% to Brazil at 42% — while low-growth periods cluster at lower inflation. The critical observation is that Brazil and South Africa’s low-growth periods coincide with lower inflation than their high-growth periods, directly contradicting the prediction that lower inflation produces higher growth. The dashed lines at 3% (IMF target) and 40% (estimated harm threshold) frame the policy-relevant zone.

High real interest rates kill investment#

The mechanism through which tight monetary policy damages growth is not difficult to identify. Most non-financial firms earn profit rates of 3–7% on their capital. If real interest rates — the nominal rate minus inflation — are above that level, it is economically rational to put capital in the bank rather than invest it in a productive enterprise. The management problems, delivery failures, and worker disputes involved in running a factory are significant; if the bank offers a risk-free return that exceeds the factory’s expected profit, only the factory will attract committed capital.

South Africa from 1994 to the early 2000s illustrates this clearly. The new ANC government adopted IMF-style macroeconomic policy to demonstrate fiscal responsibility to investors. Real interest rates reached 10–12%. Inflation was brought down to 6.3% annually. The investment rate fell from 20–25% of GDP (and once above 30%) to around 15%. Per capita income grew at 1.8% annually — the government’s own projections required 6% growth to make a meaningful dent in unemployment of 26–28%. The costs of tight monetary policy were borne entirely by those who needed jobs.

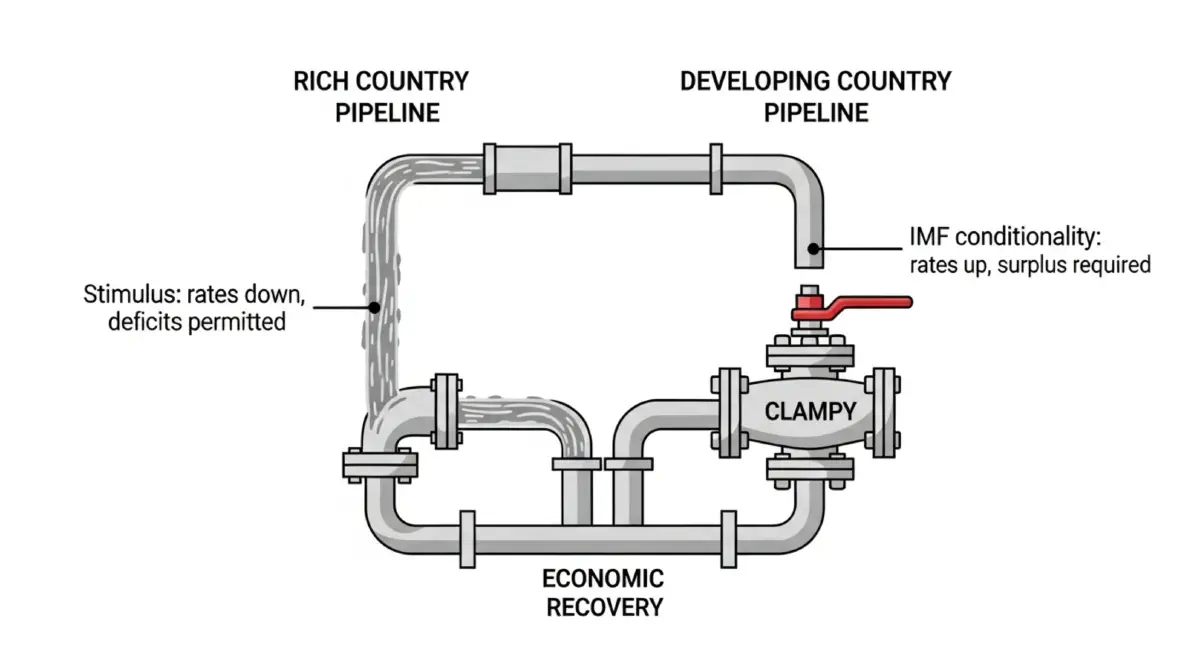

During the same period, the rich Bad Samaritan countries responded to their own economic downturns with policies that were the precise opposite of what they prescribed. After the dot-com crash and the September 2001 attacks, the George W. Bush administration — self-identified as fiscally conservative and anti-Keynesian — ran budget deficits of nearly 4% of GDP. Between 1991 and 1995, Sweden ran deficits of 8%, the UK 5.6%, Germany 3%. No rich-country finance minister raised interest rates during a recession. The prescription was Keynesian at home and monetarist abroad.

The playing field was never level#

The IMF conditions imposed on Korea during the 1997 crisis are the clearest statement of the double standard. At the time Korea signed its agreement, it had one of the smallest government debt stocks in the world as a proportion of GDP — smaller than most rich countries. The economy was in free fall, driven by capital outflows that a decade of premature financial liberalization, partly under US pressure, had made structurally possible. The correct macroeconomic response — the response any rich-country government would have applied to itself — was deficit spending to stabilize demand and low interest rates to support investment. The IMF required the opposite.

The result was described by the Korean public with a bitter acronym: IMF stood for “I’m Fired.” Over a hundred firms a day went bankrupt in the early months of 1998. Unemployment nearly tripled. The economy contracted sharply. Only when the spiral appeared genuinely uncontrollable did the Fund relent and permit small deficit spending. When Sweden had faced a comparable crisis in the early 1990s — produced by the same mechanism of premature capital market opening — it had run budget deficits of 8% of GDP. Korea was permitted 0.8%.

Figure 2: The horizontal axis shows budget deficit as a percentage of GDP; the vertical axis lists five countries. Korea’s IMF-permitted deficit (0.8%) is visually dwarfed by the actual deficits run by Sweden (8%), the UK (5.6%), and Germany (3%) during comparable financial crises. No economic theory explains the asymmetry.

Conclusion#

The macroeconomic policy that the IMF prescribes to developing countries in crisis is not the policy it implicitly endorses for rich countries facing identical circumstances. The difference is not one of economic theory — it is one of power.