The Alchemist in the Mint#

In 1893, the British administration in India performed a radical act of monetary engineering: they closed the mints to the free coinage of silver. Up until that moment, the Indian rupee had been a “full-bodied” coin—its value as money was equal to the value of the silver it contained. By ending free mintage, the government artificially restricted the supply of currency, causing the rupee’s value to diverge from its bullion content. The rupee became a “token coin,” or as a young John Maynard Keynes described it, “a note printed on silver”.

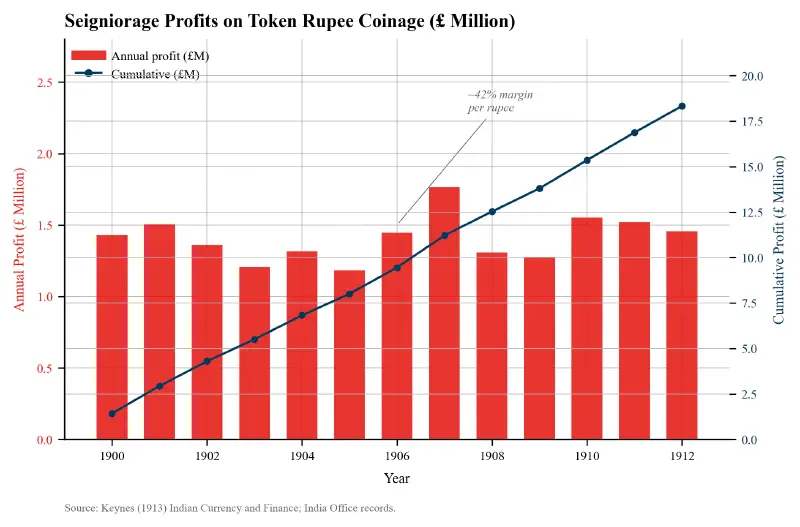

This transition allowed the British to capture the “seigniorage”—the difference between the cost of the raw silver and the face value of the finished coin. When the rupee was fixed at 1s. 4d., and silver was cheap, the profit on each coin was nearly 42%. This was not just an administrative fee; it was a massive, recurring windfall for the state. Between 1900 and 1912, the aggregate profits from this “manufactured” coinage amounted to about £18,600,000. In today’s money, that is $3.96 billion in pure seigniorage profit.

The Architecture of the Gold-Exchange Standard#

The closing of the mints created the “Gold-Exchange Standard,” a system that allowed India to use silver internally while maintaining a fixed value against gold internationally. It was a pioneer of modern currency management, yet it was designed primarily to protect British interests from the fluctuations of the silver market.

The Council Bill Siphon#

The lynchpin of this system was the “Council Bill”. The Secretary of State for India sold these bills in London to merchants needing rupees. Because the government controlled the supply of rupees, they could set a price that was slightly cheaper than shipping physical gold to India. This effectively “pre-empted” gold exports to the subcontinent. Instead of India receiving gold in exchange for its massive trade surpluses, it received more paper and silver tokens, while the physical gold stayed in London to strengthen the Bank of England’s reserves.

The Reserve Diversion#

The profits from this coinage were not reinvested into Indian industry. Instead, they were channeled into the “Gold Standard Reserve,” which was kept almost entirely in London. By 1912, this reserve stood at nearly £20,000,000 (roughly $4.26 billion today). These funds were invested in British government securities or lent out to financial houses in the City of London at low interest rates. This provided a “large masse de manoeuvre” that British authorities used to support the sterling system, keeping London at the center of global finance using Indian assets.

The Elasticity Paradox#

Because the rupee supply was determined by the Secretary of State’s bill sales rather than the internal needs of the Indian economy, the currency was “internally inelastic”. During the harvest seasons, when demand for cash was high, interest rates in Bombay and Calcutta would skyrocket to 8% or 9%, while the government sat on massive cash balances in London. The system favored the smooth remittance of the “Home Charges” over the commercial health of the Indian domestic market.

The Seigniorage Model#

The falsifiability of this critique depends on whether the coinage profits were a necessary cost for currency stability. If the Gold-Exchange Standard had provided a more stable trade environment than a pure gold standard, the seigniorage might be justified as an insurance premium. However, the system broke down during World War I, forcing India back onto a silver standard and leading to massive inflation. The seigniorage was a “tax on the circulation,” where the state profited from the very act of providing a medium of exchange.

| Coinage Arithmetic (1910-1912) | Value | Today’s Value ($) |

|---|---|---|

| Gross Coinage Profits | £18.6M | $3.96 Billion |

| Annual Average Profit | £1.55M | $330 Million |

| Bullion Cost of Rupee (Silver at 24d/oz) | 9.18d | – |

| Face Value of Rupee | 16d | – |

| Profit Margin per Rupee | ~42% | – |

The Manufactured Dependency#

Keynes argued that the Gold-Exchange Standard was “the system of the future” because it economized the use of gold. But in the Indian context, it was an instrument of dependency. By preventing India from transforming its trade surpluses into physical gold reserves, the India Office kept British interest rates lower than they otherwise would have been. English banks could borrow from these Indian funds at 2% and reinvest them at 3%, a direct transfer of liquidity from the periphery to the core.

The “Token Coin” was the physical manifestation of a monetized empire. It was a currency whose value was determined in a London boardroom and whose profits were spent on British bonds. India became a “buffer at the base of the world economy,” absorbing depreciating silver while exporting its real production at stable gold prices for the benefit of the British consumer.