What a Vehicle Is Worth When It Stops Being a Vehicle#

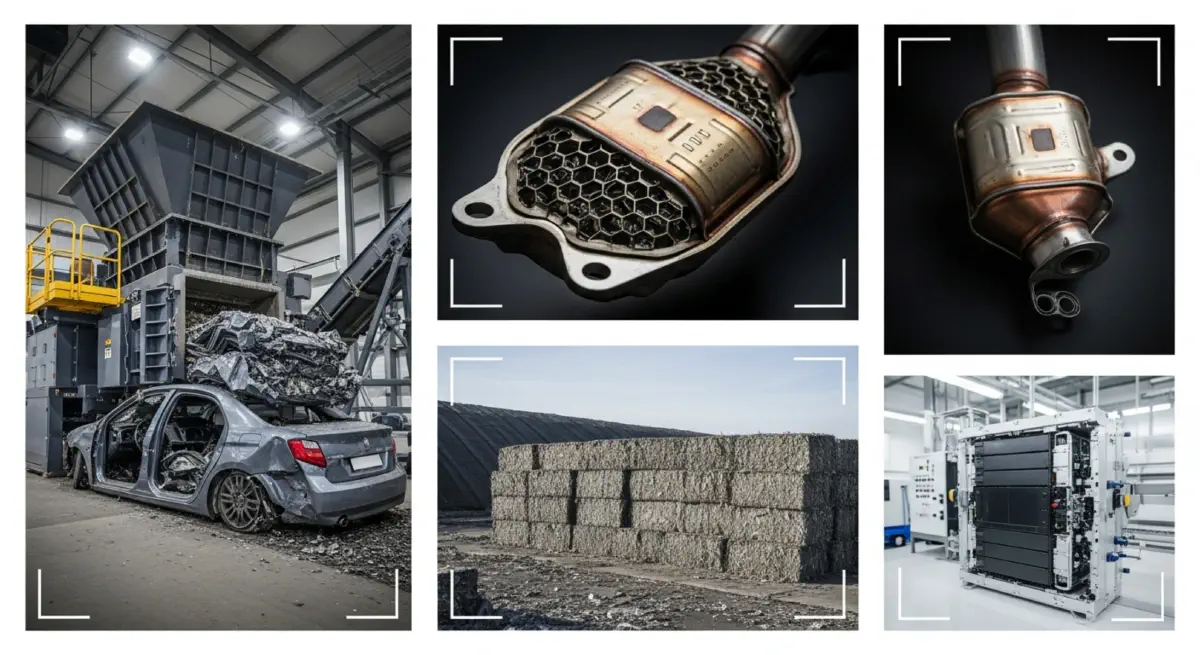

In Granite City, Illinois, the Alter Scrap Processing facility runs a Newell shredder rated at 4,000 horsepower. The shredder accepts end-of-life vehicles at an intake rate of approximately 450 vehicles per day — flattened, drained of fluids, and delivered by tow truck from regional salvage dealers who have already stripped the high-value components: the catalytic converter, the alternator, the alloy wheels, the infotainment screen and sensors. The remaining carcass, predominantly structural steel with some residual aluminium, copper wiring, glass, plastic, rubber, and foam, passes through the shredder in approximately 45 seconds. The output is a magnetic ferrous fraction, a light non-ferrous fraction, and shredder residue — the fraction that the metal recovery process cannot reach.

The shredder is the formal endpoint of the domestic end-of-life vehicle stream. It is also the point at which the economics of vehicle disposal reveal a structural contradiction: the valuable materials in the vehicle — precious metals in the catalytic converter, engineered metals in the drivetrain — have already left before the shredder receives the carcass, either through legal pre-processing or through a parallel, illegal economy that extracts the same value faster and with no accountability. And the material that remains after the shredder — approximately 3–7 million tonnes per year in the United States alone — is an engineered composite that no shredder can separate and no recycling process currently accepts at scale.

The Economics of Destruction#

The Catalytic Converter: Price Signal That Built a Criminal Market#

The automotive catalytic converter requires platinum-group metals — platinum, palladium, and rhodium — as catalytic surfaces. These metals are among the rarest naturally occurring elements accessible by conventional mining. They are extracted almost exclusively from two geographic concentrations: the Bushveld Igneous Complex in South Africa, which supplies approximately 70% of global platinum and rhodium; and the Norilsk deposits in Russia, which supply a substantial share of global palladium. Combined, South Africa and Russia account for approximately 80–85% of annual platinum-group metal mining supply.

The spot prices of these metals generated a criminal economics that any pricing model should have anticipated. Palladium averaged approximately $500/troy oz in 2016. By March 2022, it reached $3,440/troy oz, driven by tightening emissions standards requiring higher platinum-group metal loading and by Russian supply concerns following geopolitical disruption. Rhodium's price trajectory was more extreme: from approximately $690/troy oz in 2016 to a peak of approximately $29,200/troy oz in May 2021, the highest recorded price for any traded metal, before retracting to approximately $4,500/troy oz in 2024.

A catalytic converter from a Toyota Tacoma contains approximately 3–8 grams of palladium and 3–7 grams of rhodium, plus platinum. At 2021 peak prices, the metal value of that single converter exceeded $1,000 — accessible with an angle grinder and a reciprocating saw in approximately 90 seconds. The National Insurance Crime Bureau reported that catalytic converter thefts in the United States increased from approximately 1,300 incidents in 2018 to approximately 64,000 incidents in 2021. The National Equipment Finance Association estimated the total theft market at approximately $1.6 billion in 2022. The vehicle models most affected — Toyota Prius, Toyota Tacoma, Honda Element — are those with higher platinum-group metal loading in their converters, which are higher precisely because those vehicles have historically achieved better emissions compliance.

The theft market demonstrated something that the formal recycling economy confirms more quietly: the catalytic converter is the most valuable recyclable component in a modern vehicle by weight, worth substantially more per kilogram than structural steel, aluminium, or copper. The legal catalytic converter recycling sector — which processes end-of-life converters from authorised dismantlers — turned over approximately $2.8 billion in 2022, according to industry estimates compiled by ICMR. The illegal market captured, at its peak, a value roughly comparable to the legal processing sector's total output.

Shredder Residue: The Fraction That Cannot Be Recycled#

After a vehicle has been dismantled, catalytic converter recovered, and ferrous body shredded, the shredder residue — the fraction remaining after magnetic and eddy current separation — represents approximately 200–350 kg per vehicle. Its composition varies by vehicle vintage: older vehicles generate carcasses with higher rubber and fabric content; newer vehicles have proportionally more engineering polymers, foam, glass fibre, and composite materials that are mechanically inseparable in the shredder.

Shredder residue is classified in most jurisdictions as a hazardous waste, because it contains residual fluids — oils, brake fluid, coolant — from incomplete pre-processing, along with heavy metals from paint and electronic components. U.S. disposal is primarily landfill-based, at a tipping fee of approximately $50–$80 per tonne, depending on the facility. Total annual U.S. shredder residue generation: approximately 3–7 million tonnes. Annual disposal cost: approximately $150–$560 million for landfill tipping fees alone.

The EU End-of-Life Vehicles Directive, originally enacted in 2000 and applicable in its 2003 implementation, mandated reuse and recovery targets progressing to 95% recovery and 85% reuse/recycling by weight by 2015. The 2023 revised ELV Regulation (proposed) extends these targets and adds novel requirements on recycled content and design for disassembly. The critical definitional issue in these targets is that "recovery" includes energy recovery — burning shredder residue in energy-from-waste facilities. Several EU member states count energy recovery toward the 95% target. Under a strict material-recycling interpretation, European shredder residue actual recovery rates are closer to 70–75%, with the gap filled by incineration counted as recovery.

The EV Battery Residue Problem and the Amplification Ahead#

The shredder residue problem is a static engineering challenge for conventional ICE vehicles. For battery-electric vehicles, it becomes a substantially larger challenge as the current EV fleet ages into end-of-life cycles in the 2030s and 2040s. A 75 kWh lithium-ion battery pack weighs approximately 400–650 kg. It contains engineered composite materials — the electrode architecture, the separator, the electrolyte, the cell casing — that are not separable by conventional shredding. Hydrometallurgical battery recycling processes that recover lithium, nickel, cobalt, and manganese are technically feasible and commercially operating at modest scale, but the process economics are highly sensitive to the price of the recovered metals at the time of processing: when palladium or cobalt prices fall, the economics of recycling versus shredding and landfilling change correspondingly.

EU Battery Regulation 2023/1542 mandates minimum recycled content for new batteries from 2031: 6% recycled lithium, 6% cobalt, 6% nickel, 12% lead. These targets create a demand signal for battery recycling infrastructure. They do not ensure that the end-of-life volume from first-generation EV deployments in the late 2020s has the processing infrastructure to match — Benchmark Mineral Intelligence's analysis suggests the recycling capacity commissioned through 2024 can handle approximately 35–40% of anticipated end-of-life battery volume by 2030.

The Complete Scrappage Circuit#

The four posts in this series have constructed a single analytical framework for evaluating scrappage economics across their full spatial and temporal reach. The SDR captures the cross-border emissions displacement that domestic carbon accounting misses. The southern flow maps the three primary export vectors — European diesel to West Africa, Japanese JDM to Southeast Asia and the Pacific, North American light-trucks to Latin America — and their regulatory bypass architectures. The informal economy section established that ECU-governed vehicles are now arriving in destination markets with maintenance requirements that exceed local diagnostic capacity, shortening service lives and compounding both the displacement harm and the economic harm to the purchasing household.

The shredder economics complete the circuit: the high-value fraction of the vehicle — the precious metals in the catalytic converter — has already been extracted by the time the formal recycling stream reaches the vehicle, either through authorised dismantling or through theft. What the formal stream processes is the devalued remainder, from which it must cover disposal costs for the shredder residue fraction that no current recycling technology can economically recover.

The Scrappage Displacement Ratio, applied consistently, does not argue that vehicle scrappage is environmentally counterproductive in all cases. It argues that scrappage programmes that calculate their environmental benefit only on the domestic emissions saving — and award subsidies or carbon credits to that calculation — are measuring a fraction of the outcome and calling it the whole. The SDR provides the denominator against which the domestic saving should be compared: not to veto scrappage policy, but to design it honestly. A policy instrument that requires an SDR calculation before subsidy allocation would produce substantially different programme designs: higher destruction verification requirements, binding export standards, repairability assessments for destination-market conditions, and end-of-life responsibility frameworks that follow the vehicle rather than stopping at the export dock.

The vehicles do not disappear when they cross the border. Their carbon does not disappear either. The accounting system that claims they do is the fundamental problem this metric was designed to name.