The President Who Read the Reports#

On February 17, 2023, Chilean President Gabriel Boric announced the nationalisation of lithium: a new policy framework that would require all future lithium exploitation in Chile to involve a majority state-owned enterprise, with CODELCO — the state copper company — and ENAMI as the designated vehicles for the state’s participation. The announcement came six months after Boric’s government had received the report of a National Lithium Commission, which had recommended that Chile capture more domestic value from its dominant position in global lithium supply. Chile holds approximately 39% of the world’s identified lithium reserves in the Salar de Atacama and is the second-largest lithium producer, after Australia, with approximately 26% of current global production.

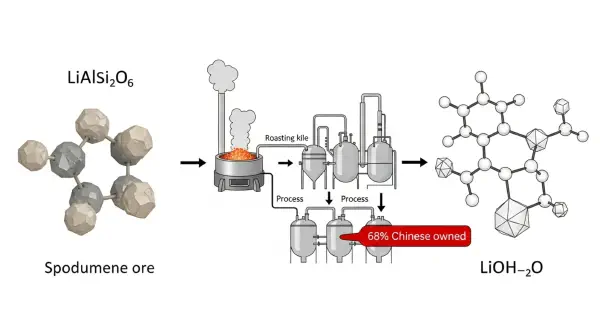

The announcement was widely covered as a nationalisation — and technically it was, in that future concessions would require state partnership. But its more consequential ambition was vertical integration: Chile’s lithium policy was not merely to ensure state participation in mining, but to develop domestic lithium hydroxide processing capacity. The Boric framework explicitly cited the processing premium — the fact that Chile was selling lithium carbonate at commodity prices while Chinese processors captured the value-added margin of converting it to battery-grade hydroxide — as the central economic rationale.

Chile was reading from a script that the IEA, the World Bank, and a generation of natural resource economists had written under the heading of the “resource curse” — the observed tendency for commodity-export-dependent economies to fail to capture the downstream value of the materials they provide. The irony in the battery mineral context is that the “cure” for the resource curse — domestic value-added processing — directly reduces the processing diversification that the Western governments’ critical minerals policies are attempting to build in non-Chinese locations. A Chile that successfully captures lithium hydroxide processing domestically is a Chile whose processing capacity is less available for Western supply chain diversification strategies.

The Cycle, Its Stages, and Its Timing#

The Anatomy of Resource Nationalism in Battery Minerals#

Resource nationalism in the extractive industries follows a documented cycle that Auty, Sachs, and subsequent analysts have characterised across oil, copper, and rare earth case histories. The cycle has five stages with characteristic timing:

Stage 1 — Discovery and Foreign Exploitation (typically 10–25 years): The mineral resource is identified and exploited primarily by foreign capital and expertise, at terms negotiated when the resource’s strategic value is not yet established. The host country receives royalties, taxes, and employment benefits. The processing value-add largely flows to offshore refiners.

Stage 2 — Revenue Coalescence (5–10 years): The resource generates visible export revenues and employment. Domestic political debate coalesces around the question of resource ownership and value capture. Civil society and legislative discourse frames existing terms as insufficiently favourable to domestic interests.

Stage 3 — Renegotiation or Nationalisation (2–5 years): Terms are renegotiated, royalty rates increased, local content requirements imposed, or majority state ownership mandated. Foreign operators either accept renegotiated terms or exit. New entrants accept higher state shares as the price of access.

Stage 4 — Processing Aspiration (5–15 years): The host government invests in or mandates the development of domestic processing capacity. This may be achievable (Chile, which has copper smelting infrastructure that provides processable analogies for lithium) or aspirational without matching industrial infrastructure (DRC, where cobalt refining requires capital and technical capacity not currently present at scale).

Stage 5 — Stabilisation or Disruption (10–30 years): If domestic processing develops successfully, the host country achieves value-added revenue and contributes to processing diversification, improving PCI for the relevant mineral. If it fails, production volumes decline, export revenues fall, and the foreign capital that a less nationalist framework might have attracted does not return on favourable terms.

Bolivia’s Lithium: Stage 4 Dysfunction#

Bolivia holds the world’s largest identified lithium reserve in the Salar de Uyuni — approximately 21 million tonnes of lithium content against Chile’s 9.3 million. Under the government of Evo Morales and subsequent administrations, Bolivia pursued an explicitly nationalist lithium strategy: no foreign ownership of lithium mining, domestic processing as a non-negotiable sovereign objective, and a series of partnership negotiations with international battery manufacturers that repeatedly collapsed when processing technology transfer terms could not be agreed.

The ACISA-Russia partnership announced in 2019 and the CITIC Guoan-China joint venture negotiated in 2018 both failed to reach production. The German ACI Systems (ACISA) deal — which had proceeded further than others — was cancelled in November 2019 following protests from indigenous communities in the Potosí department where the Salar is located, arguing that the community consultation process required by Bolivian law had not been adequately conducted. The YLB-CATL joint venture announced in 2023 is currently the most advanced active partnership, targeting direct lithium extraction technology that would allow battery-grade lithium extraction from brine with lower water use than conventional evaporation methods. CATL has provided technology and investment commitments. Production timeline: 2025 is the stated target; independent analysts consider 2027–2028 more realistic given infrastructure requirements.

Bolivia produces approximately 4,000 tonnes LCE per year — less than 1% of global lithium output — from the world’s largest reserve, because the nationalism architecture that seeks to extract the maximum upstream value has made operational agreements impossible to conclude and sustain at the pace that commercial deployment requires. The PCI impact of Bolivia’s resource nationalism: its lithium reserve is effectively off the global battery supply chain, eliminating what could be the most significant source of mining-stage concentration reduction available.

The DRC Cobalt Parallel: Stage 3 to Stage 4#

The Democratic Republic of Congo’s cobalt governance — approximately 70% of global cobalt mining supply — has been in a slow transition from Stage 3 renegotiation to Stage 4 processing aspiration for the past decade. The 2018 DRC Mining Code revision increased royalty rates, imposed windfall profit taxes, and required domestic processing of a minimum percentage of cobalt production. The domestic processing requirement was largely nominal in its initial form — the country’s industrial electricity infrastructure cannot support the energy-intensive hydrometallurgical refining processes at commercial scale. But the direction of policy is clearly toward Stage 4, and the Chinese investment that dominates DRC cobalt mining has partially responded by investing in primary cobalt processing infrastructure — converting ore to cobalt hydroxide at mine site rather than shipping raw ore — as a first step toward satisfying local content requirements while retaining the high-value refining step in Chinese processing facilities.

For the PCI calculation, a DRC that successfully develops cobalt refining capacity would reduce China’s processing share and lower the cobalt PCI — a genuinely positive supply chain diversification outcome. Whether the DRC’s power infrastructure, institutional capacity, and investment climate can support that development is the critical uncertainty. The trajectory through 2024 is modestly positive: DFC and EU investment vehicles have committed to DRC energy infrastructure projects that are preconditions for industrial processing scale. The timeline to production-scale cobalt refining in the DRC: 10–15 years for meaningful capacity at current investment trajectories.

The Paradox at the Series’ End#

The Rare Earth Gambit series has constructed the Processing Concentration Index, documented its application across four critical battery minerals, audited the policy response against the concentration it addresses, and traced the resource nationalism cycle that is simultaneously the course-correction for producer countries and a supply chain complication for consumer countries. The synthesis yields a genuine paradox.

The PCI would be reduced — supply chains would be less concentrated and more resilient — if lithium-producing countries like Chile, Argentina, and Bolivia captured domestic processing. The same processing diversification that reduces PCI would, if it occurs in countries that resource nationalism logic is directing it toward, produce a supply landscape with more producing nations but potentially with processing concentrations that are geographically dispersed rather than Chinese-concentrated. That is a more resilient architecture than the current one. It is also one that takes 15–25 years to develop through the resource nationalism cycle and cannot be accelerated to the 7-year timeline that the IRA’s escalating domestic content thresholds assume.

The PCI is an honest metric. It measures the concentration where concentration exists — at the processing stage — rather than at the mining stage where trade statistics are more legible. The policy response would be more effective if it targeted the PCI: funding processing capacity in FTA-partner countries at the scale required to move the PCI significantly, rather than at the scale currently being deployed; acknowledging that the domestic content compliance timeline requires either qualifying processing capacity or downward revision; and accepting that resource nationalism in producer countries is a structural feature of the transition, not an anomaly to be managed, and designing supply chain architectures that can accommodate it. The mineral beneath the ground belongs to the state that sits above it. The battery in the vehicle belongs to the manufacturer that assembled it. The supply chain between them is the gambit.