The Partnership That Met Seven Times and Produced No Tonnes#

The Minerals Security Partnership — announced by the U.S. State Department in June 2022 and including fourteen countries comprising Australia, Canada, Finland, France, Germany, India, Italy, Japan, Norway, South Korea, Sweden, the United Kingdom, the United States, and the European Union as an institutional partner — was described at its launch as a mechanism to “catalyse public and private investment in critical minerals supply chains.” By the end of 2023, the MSP had held seven forum meetings, issued multiple communiqués identifying supply chain vulnerabilities, facilitated eighteen projects across member countries, and secured approximately $3.5 billion in commitments across its project portfolio.

The global critical minerals processing market it is designed to address turns over approximately $280 billion annually. China’s processing capacity investment in battery minerals between 2010 and 2023, which established the processing dominance the PCI metric quantifies, totalled approximately $90–120 billion in documented industrial policy support, infrastructure, and preferential financing. The MSP’s $3.5 billion in commitments — across 14 countries, over 18 months — represents approximately 3–4% of what China invested in building the concentration the MSP was formed to address, spread across a partnership with structurally different state-investment mechanisms, permitting timelines, and industrial policy coordination than the centralised system that built the Chinese processing capacity.

None of this makes the MSP useless. It represents genuine political will and some meaningful project facilitation. It does not, at its current scale and velocity, constitute a supply chain resilience programme commensurate with the vulnerability it was designed to address.

The Instrument Gap Between Announcement and Production#

Three Mechanisms and Their Structural Limitations#

The U.S. government’s critical minerals supply chain diversification effort operates through three primary mechanisms: the IRA domestic content framework (addressed in Post 2), the Defense Production Act Title III authorities that allow the Department of Defense to fund critical mineral production capacity on national security grounds, and the Export-Import Bank and DFC (Development Finance Corporation) financing facilities for critical mineral projects in partner countries.

DPA Title III has historically been the most flexible rapid-deployment instrument: it allowed the Pentagon to fund rare earth processing capacity through MP Materials at Mountain Pass, California — the only current significant U.S. rare earth mining and initial processing facility — as a national security measure outside the normal appropriations process. MP Materials received approximately $35 million in DPA Title III funding in 2020 for separation facility expansion. The facility produces rare earth carbonate concentrate and, since 2023, separated rare earth oxides — but not the NdFeB magnet alloy powder used in final motor production, which remains a processing step completed in Japan, China, and Germany. The DPA investment advanced the supply chain two steps. It did not reach the processing step where the PCI is most concentrated.

The DFC’s critical mineral lending — authorised to provide up to $60 billion in guarantees, loans, and equity investments globally — has funded lithium projects in Argentina (Lithium Americas’ Cauchari-Olaroz project, now producing), cobalt and copper projects in the DRC (Ivanhoe Mines’ Kamoa-Kakula project), and nickel processing in Canada. These are substantive investments in the mining and processing supply chain. Their output is raw or intermediate material, not battery-grade processed compound. The final refining step — conversion to battery-grade lithium hydroxide, battery-grade cobalt sulphate, or battery-grade nickel sulphate — in each of these projects is still predominantly performed in Asian processing facilities, including Chinese ones where no alternative exists at the required scale and specification.

The FTA Architecture and Its Processing Blind Spot#

The IRA’s free-trade agreement framework for critical minerals compliance — identifying the countries whose mining and processing can count toward domestic content thresholds — includes Australia, Chile, Japan, South Korea, and the European Union among its most relevant partners for battery minerals. This architecture was designed to expand the geographic scope of qualifying suppliers beyond the U.S. domestic production base, which is inadequate to meet projected battery demand on any timeline through the 2030s.

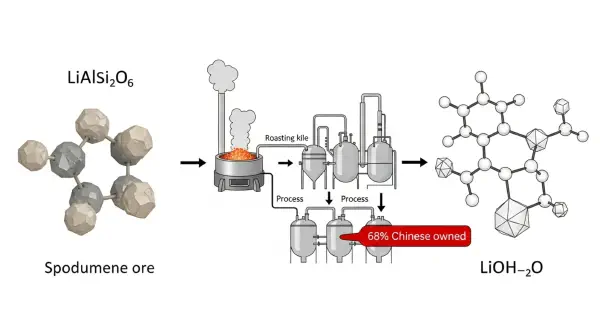

Australia qualifies as an FTA partner and is the world’s largest lithium spodumene miner. Australian lithium project operators — Pilbara Minerals, Core Lithium, IGO, Albemarle’s Greenbushes operation — export spodumene concentrate from Australia. The concentrate is then shipped to China for lithium hydroxide conversion, with a small but growing fraction going to processing facilities in Australia itself (the Kemerton lithium hydroxide plant), South Korea, and Japan. When spodumene mined in Australia is processed in China, it does not qualify for IRA critical minerals compliance, regardless of the Australian mining origin. When it is processed in Australia or a qualifying partner, it does.

The processing capacity in qualifying FTA-partner countries for lithium hydroxide as of 2024: the Kemerton facility in Western Australia (capacity approximately 50,000 tonnes LCE/year), the Kwinana facility (30,000 tonnes, under commissioning), and planned capacity in Japan and South Korea (approximately 40,000 tonnes combined, under development). Total qualifying non-Chinese lithium hydroxide processing capacity foreseeable by 2027: approximately 120,000–150,000 tonnes LCE/year. U.S. EV battery demand at 80% IRA compliance threshold by 2027, given Department of Transportation EV adoption projections: approximately 350,000–450,000 tonnes LCE/year. The qualifying processing capacity will cover approximately 30–40% of the compliance requirement at most. The remainder will require either Chinese-processed materials (disqualifying the EV’s IRA credit), broader Treasury interpretive guidance, or acceptance that the 80% threshold will not be achievable on schedule for vehicles using standard battery chemistries.

What the Policy Response Achieves#

The critical minerals policy response of 2021–2024 — IRA domestic content, MSP formation, DPA investments, DFC lending, and the EU Critical Raw Materials Act — represents the most systematic Western government engagement with battery supply chain vulnerability in the history of the industry. It is substantially inadequate in scale relative to the concentration it addresses, structurally miscalibrated in the IRA’s preference for mining origin over processing concentration, and chronologically misaligned with the EV deployment volumes it will be needed to support.

What the policy response achieves is a beginning: the institutional acknowledgment that supply chain concentration is a strategic vulnerability, the initial financing of non-Chinese processing capacity that did not previously exist, and the creation of market signals through domestic content requirements that will, over time, stimulate additional processing investment. The Australian lithium hydroxide processing sector is expanding precisely because the IRA created a demand signal for qualifying material. The South Korean battery manufacturer supply chains are restructuring to position qualifying material as a competitive differentiator.

The PCI metric provides the framework for evaluating whether the policy is addressing the right chokepoints at the right scale. Applied to the current investment portfolio, the verdict is that the policy is pointing in approximately the right direction — toward processing rather than only mining — but at a fraction of the capital intensity required. The next post examines what happens when the countries where mining is concentrated begin exercising the same industrial logic that China exercised with processing: resource nationalism cycles that attempt to capture the processing value-add domestically, moving both the mining HHI and the PCI simultaneously as nationalisation compounds concentration.