The Trade Restriction That Clarified the Architecture#

On August 1, 2023, China’s Ministry of Commerce announced export restrictions on gallium and germanium — two materials whose global processing is approximately 80% Chinese, used in compound semiconductors for radar, satellite communications, and power electronics. The announcement cited national security considerations. The market response was immediate: gallium spot prices increased approximately 50% in the two weeks following the announcement before supply diversification signals moderated the movement. The restriction was not a full embargo — it required export licences, creating administrative friction rather than supply cutoff — but it demonstrated, in a single policy action, the mechanism through which processing concentration translates to leverage.

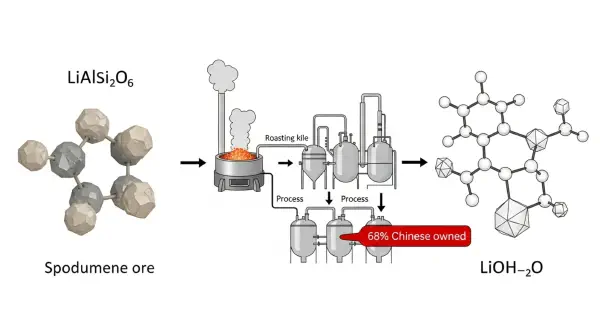

Gallium and germanium are not battery minerals. Their volumetric demand is small relative to lithium, cobalt, or nickel. But the August 2023 action served as a proof-of-concept for the battery mineral supply chain vulnerability that the IEA and USGS critical mineral assessments had been characterising in qualitative terms since 2020. China’s processing dominance in battery minerals creates a lever of the same structural type: not requiring the elimination of lithium mining in Chile, cobalt mining in the DRC, or nickel mining in Indonesia, because China does not primarily own those mining operations. The lever works at the processing stage — the stage where ore becomes battery-grade chemical compound, and where Chinese industrial policy has systematically built dominant capacity since approximately 2005.

The question that the August 2023 action raised for battery supply chains — and that the IRA’s domestic content framework must now answer — is whether the policy instrument designed to address the leverage was calibrated to the stage where the leverage actually operates.

Where the IRA Points and Where the Chokepoint Is#

The Domestic Content Architecture and Its Stage Preference#

The IRA’s Section 30D Clean Vehicle Credit, as revised by the Inflation Reduction Act of 2022, conditions the $7,500 tax credit available to EV buyers on two separate content requirements applied to battery critical minerals and battery components respectively. The critical minerals requirement — applying to lithium, cobalt, nickel, manganese, graphite, and copper in the battery — escalates from 40% of the value of qualifying minerals from “extraction or processing” in the U.S. or a free-trade agreement partner country in 2023, to 80% by 2027.

The critical minerals threshold counts both extraction and processing toward compliance. A mineral that is mined in Chile — a free-trade agreement country — and processed in China does not qualify, because China is not a free-trade agreement partner and is specifically excluded from the “foreign entity of concern” provision. A mineral mined in Chile and processed in Chile does qualify. A mineral mined in Australia and processed in Australia qualifies. A mineral mined in Australia and processed in China does not qualify.

This architecture creates a processing incentive in addition to a mining incentive — which is the right direction of policy. The critical design question is whether the compliance threshold reflects where the actual supply-chain bottleneck is. The 40%–80% threshold applies to the “value” of qualifying minerals — which is primarily determined by the processing stage, since processed battery-grade lithium hydroxide has 6–8 times the market value per tonne of lithium carbonate feedstock. This means that a relatively small volume of qualifying lithium hydroxide produced in a U.S. or FTA-partner processing facility can satisfy the critical minerals threshold even if the majority of minerals by mass flow through Chinese processing. The value-based compliance threshold maps imperfectly onto the supply security objective, because value accumulates most rapidly at precisely the concentration stage that the policy was designed to address.

The Processing Capacity Timeline and the EV Demand Curve#

The IRA’s domestic content phase-in timeline assumes that qualifying alternative processing capacity will be available as the threshold escalates from 40% in 2023 to 80% in 2027. The timeline for bringing new lithium hydroxide processing capacity to commercial production in the United States: approximately 7–12 years from feasibility study to first qualified output, based on the development timelines of the five U.S. lithium processing projects announced in 2021–2023.

Lithium Americas’ Thacker Pass lithium project in Nevada — the largest domestic lithium project in the U.S. pipeline — received its Record of Decision from the Bureau of Land Management in January 2023, after a NEPA review process that began in 2018. Permitting for the associated lithium carbonate processing facility is on a separate regulatory track. First production was targeted for 2026 at Phase 1 capacity of approximately 40,000 tonnes LCE per year — approximately 2% of the 2 million tonne LCE demand projected by the IEA for 2040. Piedmont Lithium’s North Carolina project has faced permitting delays extending its timeline to 2026 or later. Standard Lithium’s Arkansas brine project is in the pilot phase. The aggregate U.S. domestic lithium hydroxide production capacity that will be available and qualified for IRA domestic content compliance by 2027 — when the 80% threshold takes effect — is, on the most optimistic current project timeline assessments, approximately 8–12% of anticipated U.S. EV battery demand at that date.

The IRA created demand signals and investment incentives. It did not accelerate the regulatory timelines, environmental permitting processes, or physical construction timescales that determine when capacity reaches production. The gap between the 80% compliance threshold that takes effect in 2027 and the qualified domestic processing capacity likely to exist in 2027 will be bridged either by FTA-partner processing — putting Australia and Chile in the critical path — or by Treasury interpretive guidance that defines “processing” more permissively than the statute’s language indicates. Neither approach resolves the core mismatch between the policy’s timeline and the industry’s physical development cycle.

The Rare Earth Magnet Case: Where PCI Is Most Extreme#

The PCI analysis reaches its most acute expression in rare earth permanent magnets: neodymium-praseodymium magnets of the NdFeB (neodymium-iron-boron) type used in the permanent magnet synchronous motors of most high-performance EV drivetrains. An NdFeB motor in a Tesla Model 3 uses approximately 3–4 kg of permanent magnets containing roughly 1 kg of neodymium-praseodymium alloy. At current EV deployment trajectories, permanent magnet demand from EV motors will increase approximately 5× by 2035.

China mines approximately 58% of global rare earth elements and processes approximately 90% of global rare earth oxide output. The PCI for NdFeB magnet precursor processing: applying the same formula, $s_{China} = 0.90$, $p_{China} = 0.90/m_{China} = 0.90/0.58 = 1.55$. China’s PCI contribution: $0.90^2 \times 1.55 = 0.81 \times 1.55 = 1.255$. With no other nation contributing more than approximately 5% of processing capacity, total PCI ≈ 8,800. This is the most concentrated critical supply chain in the battery and EV ecosystem — a single-country processing dominance approaching monopoly levels, achieved through a combination of natural endowment (the Bayan Obo deposit in Inner Mongolia is the world’s largest REE deposit) and deliberate industrial policy that subsidised processing capacity buildup from the early 2000s onward.

No equivalent to the IRA critical minerals domestic content provision currently addresses rare earth permanent magnet supply security for U.S. motor manufacturers. The Advanced Manufacturing Production Credit (Section 45X) provides production credits for battery components but does not extend to rare earth magnet processing. The EV motor that houses those magnets is not covered by any domestic content requirement in the current IRA framework. The most concentrated supply chain in the EV ecosystem is the only one without a domestic content policy response.

The next post examines how resource nationalism cycles have historically interacted with processing concentration dynamics — and what the emerging nationalisation pressures in lithium-producing countries mean for both the mining HHI and the PCI as the EV transition enters its high-volume deployment phase.