Timeline of Main Events in China's Automotive History

Timeline of Main Events in China's Automotive History#

1945–1952

China focuses on rebuilding basic industrial capacity following post-war constraints.

1949–1979

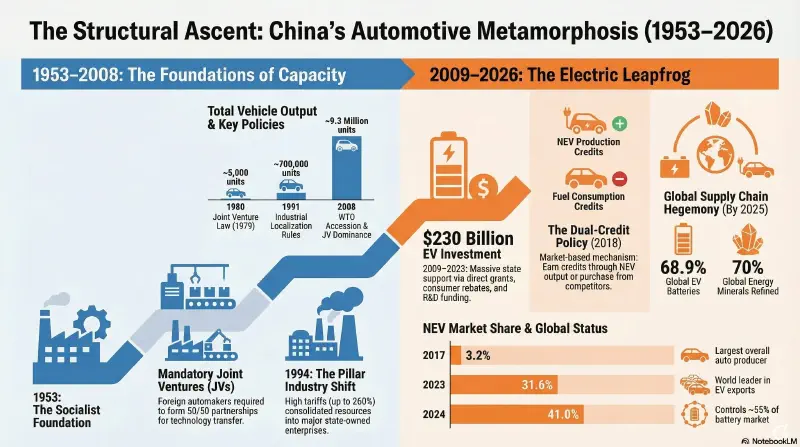

**Central Planning Phase** – nascent industry with total vehicle output of ~5,000 units by 1980.

1953

FAW Group

First Auto Works (FAW) established with Soviet assistance under the First Five-Year Plan. Average yearly production: 3,206 units (1953–1957).

1953–1978

Production remains centrally planned, focused on domestic models like the Shanghai and Red Flag for state officials.

1955

SAIC Motor and GAC Group are established.

1958

BAIC Group is established.

1969

Dongfeng Motor is established.

July 1979

Market for Technology

China enacts the Law on Joint Venture Using Chinese and Foreign Investment, opening the door for foreign capital and technology. Foreign ownership capped at 50%.

Early 1980s

High protectionist trade barriers: import tariffs on vehicles reach 250–260%.

1983

First Sino-foreign JV

Beijing Jeep (BAIC / AMC) established. AMC invests USD 16 million for a 31.35% stake.

1984

SAIC-Volkswagen joint venture formed (initial capital RMB 160 million). Great Wall Motor founded.

1986

The 7th Five-Year Plan declares the automotive industry a **"pillar industry"** for the first time.

1994

Automobile Industry Policy

Formalisation of the “Market for Technology” strategy, 50% foreign ownership cap, and minimum 40% local content requirement for joint ventures.

1995

BYD founded as a battery manufacturer.

1997

Geely established; SAIC-GM joint venture formed.

2000

Annual vehicle production reaches approximately **2 million units**.

2001

WTO Accession

China joins the WTO, leading to phased tariff reductions (import tariffs fall to 25% by 2010). The 10th Five-Year Plan first emphasises New Energy Vehicles (NEVs).

2003

BYD enters passenger vehicle production; FAW-Toyota and Changan-Ford joint ventures established.

2009

World's Largest Auto Market

China surpasses the U.S. to become the world's largest automotive market and producer. Government launches massive EV subsidies and the “1,000 EVs in 10 cities” pilot.

2009–2023

State-led investment in the NEV sector totals an estimated **$230.9 billion** through subsidies, tax cuts, and industrial master plans.

2010

Geely acquires Volvo Cars for $1.8 billion.

2014

EV startup NIO is founded.

2015

The **"Made in China 2025"** initiative identifies NEVs as a strategic sector for global dominance.

April 2018

Dual-Credit Policy

The Dual-Credit Policy (CAFC and NEV credits) replaces direct subsidies. Foreign ownership caps for NEVs are lifted, enabling Tesla’s wholly owned Shanghai plant.

2020

The **Hefei Model** of state investment is highlighted by the city’s 7‑billion‑yuan rescue of NIO.

2023

China produces a record **30.16 million vehicles** and becomes a leading global exporter with **4.91 million units** shipped.

2024

NEVs reach approximately 41% of the domestic market share; public charging points exceed 2.5 million.

2025

EV Battery Dominance

Six Chinese manufacturers control 68.9% of the global EV battery market (led by CATL at 38.1%), and 90% of rare earth refining.

2026

Huawei and Xiaomi emerge as major disruptive forces in the tech-led “New Force” of automotive manufacturing.

The Leapfrog Doctrine: China’s Automotive Rise From Industrial Policy to Global Dominance -

This article is part of a series.

Deconstructs the myth of the sticker price, revealing how automakers and financial systems profit from the long-tail costs of depreciation, financing, and maintenance.

Exposes the engineered economics of vehicle repair, from proprietary software and parts locking to the systematic dismantling of the independent repair sector.

Analyzes how industrial power, policy, and planned technological turnover conspire to accelerate vehicle replacement cycles, creating a perpetual motion machine of consumption.