The Leapfrog Doctrine: China’s Automotive Rise from Industrial Policy to Global Dominance

Series Summary#

| Post | Title | Focus |

|---|---|---|

| 1 | The 30-Million-Unit Machine: A Quantitative Snapshot of Global Supremacy | Establishes China’s current empirical dominance using data-dense and comparative frames. |

| 2 | From FAW to EVs: A Causal Chronology of the 70-Year Ascent | A timeline-driven narrative that segments the industry's evolution into distinct, causal phases. |

| 3 | The Strategic Mandate: Why Beijing Bet the Future on the Automobile | Explores the "Strategic Necessity" and first-order intent behind decades of government support. |

| 4 | The Execution Architecture: Engineering a "Market for Technology" | An analysis of the "Execution Architecture"—the specific policy mechanisms used to bypass Western legacy advantages. |

| 5 | Escaping the Assembly Trap: Why China Succeeded While Others Lagged | Contrasting China’s path with countries like Brazil, India, and Mexico. |

| 6 | The Friction Frontier: Overcapacity, Tariffs, and the 2030 Horizon | Addresses "systemic opportunities and constraints," moving beyond optimistic projections to analyze |

| 7 | Timeline of Main Events in China's Automotive History | A timeline-driven narrative that segments the industry's evolution into distinct, causal phases. |

Key Insights#

Scale as a Strategic Incubator: China leveraged its status as the world’s most populous nation to use its domestic market as an "initial incubator," allowing local firms to achieve economies of scale and dilute R&D costs before competing globally. This massive home demand, which reached a record 30.16 million units produced in 2023, provided a gravitational pull that forced foreign competitors to trade technology for market access.

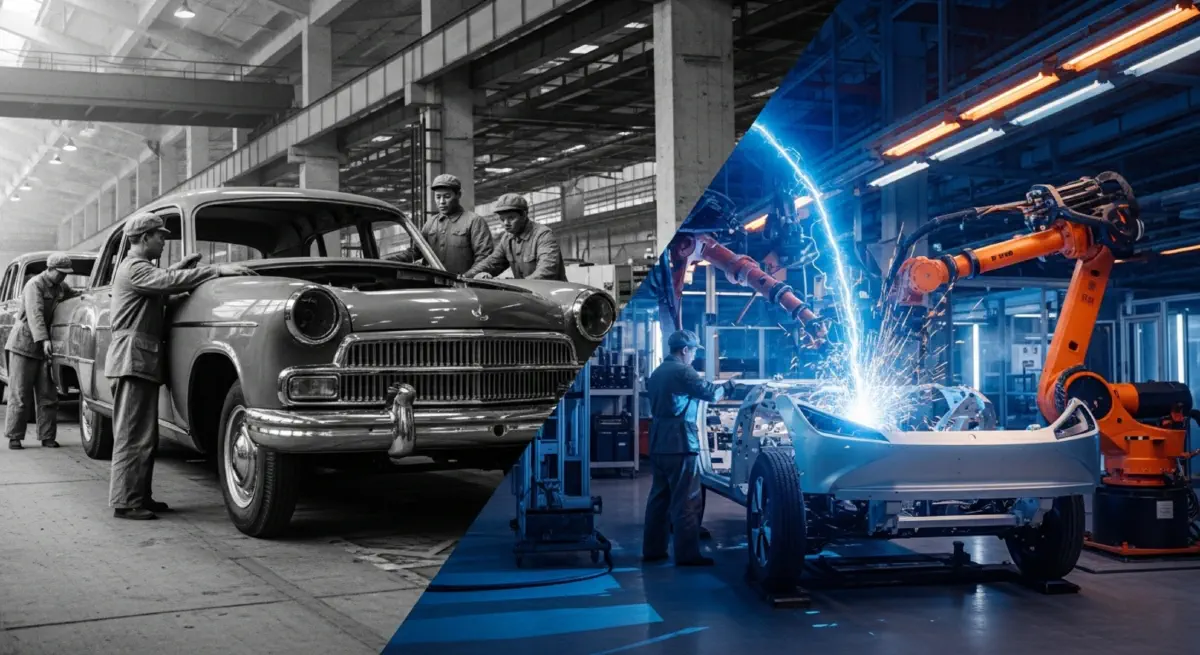

The Leapfrog Doctrine: Recognizing it could not overcome decades of Western and Japanese patent protection in internal combustion engine (ICE) technology, Beijing executed a strategic "leapfrog" by pivoting aggressively to New Energy Vehicles (NEVs). This technological reset rendered legacy expertise in powertrains and gearboxes obsolete, allowing Chinese firms to compete on a level playing field centered on battery chemistry and software.

Upstream Supply Chain Sovereignty: China’s dominance is anchored not just in vehicle assembly, but in comprehensive control of the value chain; as of 2025, it refines approximately 70% of the world’s energy-related minerals. This includes a 90% share of rare earth elements and an 85% share of graphite, creating a "technological moat" that global competitors cannot easily replicate.

The "Market for Technology" Mandate: Through "Obligated Embeddedness," China avoided the "Mexican Syndrome"—where a country becomes a passive assembly hub without indigenous brands—by mandating 50/50 joint ventures and strict local content requirements. These JVs acted as conduits for systemic industrial upgrading, raising the performance standards of the entire Chinese supplier ecosystem by decades.

State-as-Venture-Capitalist Governance: Beyond central planning, the "Hefei Model" revolutionized local governance by transforming state investment platforms into venture capital firms that take equity stakes in high-risk startups like NIO. This is complemented by the "Chain Leader" system, where high-ranking officials personally resolve administrative bottlenecks to ensure entire value chains develop in concert.

Battery and Infrastructure Hegemony: By late 2025, six Chinese manufacturers, led by CATL and BYD, controlled 68.9% of the global EV battery market. This physical lead is supported by the world's most expansive charging network, with over 2.5 million public charging points by 2024, providing double the per-vehicle capacity of the United States.

The Structural Overcapacity Crisis: The success of China’s industrial policy has generated a "structural overcapacity," with annual manufacturing capacity estimated at 50–60 million vehicles—nearly double the current domestic demand. This surplus is a primary driver behind China’s surge to become the world’s leading exporter, as firms are forced to vent excess production into international markets.

The Silicon Ceiling and Trade Barriers: Despite its lead, the industry faces critical technological bottlenecks in high-end automotive chips, with self-sufficiency in computing and control chips remaining below 1%. Simultaneously, rising trade barriers—including 100% tariffs in the US and Canada and new EU duties—are forcing a shift in strategy from direct exports toward overseas Foreign Direct Investment (FDI) and localized manufacturing.

References#

- Andreoni, A., & Tregenna, F. (2020). Escaping the middle-income technology trap: A comparative analysis of industrial policies in China, Brazil and South Africa. Structural Change and Economic Dynamics, 54, 324-340. https://doi.org/10.1016/j.strueco.2020.05.008

- AutoIndustry News South Africa. (2026, February 20). How China built a global automotive powerhouse.

- Chen, Y., Dai, X., Fu, P., & Shi, P. (2024). A review of China's automotive industry policy: Recent developments and future trends. Journal of Traffic and Transportation Engineering (English Edition), 11(1). https://doi.org/10.1016/j.jtte.2024.09.001

- CICC Research, CICC Global Institute. (2024). The Reshaping of China’s Industry Chains. Springer Nature. https://doi.org/10.1007/978-981-97-1647-0

- Covarrubias, A. V., & Ramírez Perez, S. M. (Eds.). (2020). New Frontiers of the Automobile Industry: Exploring Geographies, Technology, and Institutional Challenges. Palgrave Macmillan. https://doi.org/10.1007/978-3-030-18881-8

- Feng, J., Cai, M., Dai, F., & Lu, X. (2025). Data-driven supply chains mapping and disruption analysis: The case of automotive SoC enterprises in China. Computers and Industrial Engineering, 198. https://doi.org/10.1016/j.cie.2025.110897

- Fred Gao. (2026, March 31). How the Hefei Model works in Chinese. Inside China.

- Gallagher, K. P., & Shafaeddin, M. (2010). Policies for industrial learning in China and Mexico. Technology in Society, 32(2), 81-99. https://doi.org/10.1016/j.techsoc.2010.04.002

- Gasgoo. (2026, March 18). Chongqing automotive industry cluster at a glance. Autonews (Gasgoo).

- Gasgoo. (2026, March 31). China Zhejiang’s automotive industry cluster at a glance. Autonews (Gasgoo).

- Gereffi, G. (2009). Development models and industrial upgrading in China and Mexico. European Sociological Review, 25(1), 37-51. https://doi.org/10.1093/esr/jcn034

- Greitemeier, T., Kampker, A., Tübke, J., & Lux, S. (2025). China's hold on the lithium-ion battery supply chain: Prospects for competitive growth and sovereign control. Journal of Power Sources Advances, 34. https://doi.org/10.1016/j.powera.2025.100173

- Kang, L. (2026, February 4). Global EV battery market share in 2025: CATL 39.2%, BYD 16.4%. CnEVPost.

- Lüthje, B., & Zhao, W. (2025). Between Covid and Geopolitics: Emerging Production Networks in the New Energy Vehicle Industry in China. Palgrave Studies of Internationalization in Emerging Markets. https://doi.org/10.1007/978-3-031-80641-4_9

- MarkLines Co., Ltd. (2024). China: Flash report, automotive production volume, 2023. MarkLines Automotive Industry Portal.

- Phoon, M. (2024, June 22). CSIS study finds China’s EV industry boosted with US$230 billion in support. EV.com.

- Reuters. (2025, September 17). China is sending its world-beating auto industry into a tailspin. Reuters Investigations.

- Richardson, J. (2026, January 25). Over 20 million EV chargers operating in China now. CleanTechnica.

- State Council, PRC (Xinhua). (2026, January 21). China operates world’s largest EV charging network.

- Volgina, N. A., & Wang, Y. (2022). China’s position in the global automotive production and exports, 2018–2020. Research in Economic Anthropology, 42, 137-160. https://doi.org/10.1108/S0190-128120220000042002

- Wang, J., Chen, Y., Wang, L., & Qiang, Q. (2025). Research on the evolving patent landscape and innovation trends of critical automotive technologies in China for 2024. Proceedings of CISAI 2025. https://doi.org/10.1145/3773365.3773540

- Xu, Y., Li, J., Gao, F., & Li, Z. (2023). Reshaping of automotive industry pattern under the wave of electrification and intelligence. Journal of Automotive Safety and Energy, 14(6). https://doi.org/10.3969/j.issn.1674-8484.2023.06.001

- Xue, D., Tao, Z., Ding, Q., & Du, Y. (2024). AFV industry expanding overseas along the Belt and Road. In The Belt and Road Initiative at ten: From macro, financial and industrial trends. Springer. https://doi.org/10.1007/978-981-97-4468-8_12

- Yuan Jia-Zheng & Carles Brasó Broggi. (2025). The metamorphosis of China’s automotive industry (1953–2001): Inward internationalisation, technological transfers and the making of a post-socialist market. Business History, 67(1), 211-238. https://doi.org/10.1080/00076791.2023.2247366

- Zhang, Q., Huang, Z., Liu, B., & Ma, T. (2025). Sustainable lithium supply for electric vehicle development in China towards carbon neutrality. Energy, 312. https://doi.org/10.1016/j.energy.2025.135243

- Zhang, R. (2024, January 11). CAAM: China’s 2023 auto sales, output both hit record highs. Mysteel News.

- Zhao, M., Fang, Y., & Dai, D. (2023). Forecast of the evolution trend of total vehicle sales and power structure of China under different scenarios. Sustainability, 15(5), 3985. https://doi.org/10.3390/su15053985