What should a developing country actually do, step by step, to build a competitive automotive industry without falling into either trap?

This post distills everything we have learned into a practical, phased roadmap. The advice is specific enough to guide policy, yet general enough to apply to any country with a small to medium domestic market, a willing labor force, and a government serious about industrial development.

But first, a warning.

The Preconditions That Cannot Be Skipped#

No roadmap works if the foundation is rotten. Before you even think about automotive policy, you must have:

Basic macro stability: No hyperinflation, no chronic current account crisis. Investors need predictability.

A functioning legal system: Contracts must be enforceable. Intellectual property protection, while negotiable, cannot be absent.

A meritocratic core of the bureaucracy: You do not need every official to be clean. But the economic ministries (trade, industry, planning) must be staffed by competent technocrats who can say no to political pressure. If your MITI-equivalent is a patronage dumping ground, stop reading. Fix that first.

Political will at the highest level: Industrial policy takes 15–20 years. It will outlast election cycles. The president or prime minister must champion it consistently, or it will be reversed.

Assuming you have them, here is the roadmap.

Phase 1: Foundation

Years 0–5

Attract anchor investors and establish the institutional framework

Attract anchor investors while securing technology transfer and local linkages. Establish the institutional framework.

Do:

Identify 2–3 foreign automakers willing to enter a joint venture. Do not give exclusivity to one. Competition among foreign firms gives you leverage.

Mandate 40–50% local equity in the JV. The foreign partner can hold the rest, but management must include local deputies who are being trained to take over.

Require a technology transfer plan with specific milestones: within 3 years, local engineers must be able to perform basic design changes; within 5 years, they must lead a full model adaptation. Penalties for non-compliance (e.g., higher tariffs on imported CKD kits).

Impose a local content schedule starting at 30% in year 3, rising to 50% by year 5. Critically, also provide technical assistance to local suppliers. Do not just mandate; enable. Create a supplier development fund, staffed by experienced automotive engineers.

Set export requirements from the start. The JV must export at least 20% of production by year 5, rising to 40% by year 10. Exports force quality discipline.

Build a dedicated automotive training institute in partnership with the foreign JV. Fund it through a small levy on imported vehicles. Train hundreds of welders, painters, electricians, and assembly line supervisors.

Establish an autonomous automotive agency (modeled on Korea’s EPB or Japan’s MITI). Staff it with technocrats on fixed 5‑year terms, insulated from political dismissal. Give it authority to enforce performance conditions, deny permits, and recommend tariff changes.

Don’t:

Offer unconditional tax holidays. If you give a 10‑year tax break, demand 10 years of technology transfer and export growth in return.

Allow a single national champion monopoly. License at least two assemblers, even if one is much smaller. Domestic competition is your best anti‑complacency weapon.

Create import permit systems (APs) that can be traded or sold. Permits should be tied directly to production and export performance, not to political connections.

Forget about the consumer. Protection raises prices. That is acceptable temporarily, but you need a plan to bring prices down through competition and scale.

Phase 2: Capability Building

Years 5–10

Deepen local supply chains, raise technology absorption, and begin export expansion

Do:

Increase local content requirements to 60–70%, but now focus on value‑added content, not just parts count. Encourage joint ventures between local suppliers and foreign component makers.

Launch a vendor development program with competitive bidding. Do not assign suppliers through political favor. Use quality, cost, and delivery performance as criteria. Publish scorecards.

Require the JVs to establish R&D centers locally. Start with adaptation (tuning engines for local fuel, modifying suspension for local roads), then move to design of new models for export markets.

Phase down the highest tariffs on fully built units (CBUs) from, say, 50% to 30%. Keep excise duties that favor local production, but make the excise rebate conditional on local content and R&D spending.

Begin promoting exports aggressively. Offer subsidized export credits, trade missions, and logistics support. Target neighboring countries with similar road conditions and consumer preferences.

Monitor rent‑seeking indicators closely: Are permits being traded? Are vendor contracts going to shell companies? Are customs officials extracting bribes? Publish annual audits.

Don’t:

Extend protection automatically. If a JV fails to meet its technology transfer or export milestones, raise its tariff protection or reduce its access to subsidized credit. Consequences must be real.

Allow politically connected individuals to become sole-source suppliers. Single‑sourcing should be justified by unique technical capability, not by personal relationships.

Neglect non-automotive industrial policy. Steel, plastics, electronics, and rubber all feed into cars. Coordinated development across sectors amplifies gains.

Phase 3: Integration

Years 10–15

Local firms compete regionally; protection is selectively reduced

Do:

Reduce MFN tariffs to regional levels (e.g., 10–20% on CBUs). Excise duties should also converge, but maintain a small preference (e.g., 5–10 percentage points) for vehicles with high local R&D content.

Encourage consolidation of local suppliers. Many small, inefficient vendors should merge or exit. Provide transition assistance (retraining, severance) but do not bail them out.

Push for deeper R&D: By year 12, the JVs should be filing patents locally. The national automotive institute should spin off engineering service firms that consult for the industry.

Sign strategic trade agreements that open foreign markets for your cars while giving you time to adjust. Use tariff phase‑downs of 5–10 years.

Diversify foreign partners. If you have a JV with Japan Inc., consider a second with a Chinese or European firm. Competition among partners keeps technology flowing.

Create an export‑only free trade zone for local suppliers who sell to multiple global OEMs. This encourages them to achieve world‑class quality and cost.

Don’t:

Liberalize completely. Full free trade with large competitors (e.g., China, India, Thailand) can wipe out your industry if done prematurely. Phase liberalization over a decade, not a year.

Keep local content rules that are no longer needed. Once suppliers are competitive, let them win business on merit. But keep rules that prevent pure assembly of imported kits.

Ignore the political economy of liberalization. Workers and owners in protected sectors will resist. Have a compensation plan (retraining, diversification subsidies) ready.

Phase 4: Maturity

Years 15–20+

The industry is globally competitive; government becomes a facilitator

The automotive industry is globally competitive. Government shifts from protector to facilitator.

Do:

Bring tariffs down to near zero for all trading partners, consistent with WTO and regional commitments. Excise duties should be uniform for all vehicles, regardless of origin.

Phase out local content requirements completely. Let global supply chains decide. Your local suppliers should now be exporting on their own.

Focus government support on pre‑competitive R&D (batteries, lightweight materials, autonomous driving) rather than protecting assembly. Shift from tariffs to innovation grants.

Maintain a small, agile automotive agency that monitors global trends, negotiates mutual recognition agreements, and helps local firms attend international trade shows.

Allow foreign majority ownership if the investor commits to keeping R&D and high‑value production in the country. At this stage, you want their capital and technology, not just their assembly plants.

Don’t:

Abandon the industry after liberalization. Even advanced countries (Germany, Japan, US) have industrial policies. But they are subtle: R&D tax credits, export finance, infrastructure.

Let rent-seeking return. Once institutions are strong, guard them. Anti‑corruption agencies must remain independent and well‑funded.

Assume the job is done. The global automotive industry is transforming (EVs, software‑defined vehicles, autonomous driving). Your country must keep learning or fall behind again.

The Red Lines: When to Sound the Alarm#

Even with the best roadmap, things can go wrong. Here are four warning signs that your country is drifting toward a trap:

| Warning Sign | Indicates | Action |

|---|---|---|

| A single politically connected family controls most vendor contracts | Capture trap | Mandate open bidding, publish contract winners, launch anti‑corruption investigation |

| Exports stagnate below 20% of production after 10 years | Complacency | Withhold subsidies, raise export targets, threaten to reduce protection |

| Foreign partner refuses to train local engineers or blocks them from R&D | Technology transfer failure | Invoke contract penalties, seek alternative partner, raise local content requirement |

| AP or import permit holders are selling permits rather than using them | Rent‑seeking | Abolish the permit system immediately, compensate only genuine productive users |

If you see any of these, pause the roadmap. Fix the problem before proceeding. Half‑measures will not work.

The Single Most Important Lesson#

We have covered many policies, timelines, and warnings. But if you remember only one thing from this entire series, let it be this:

You must protect your infant industry. Every successful industrializer did. But protection must be conditional, temporary, and linked to verifiable performance: exports, technology transfer, local content, R&D.

And you must open your market eventually. Every successful industrializer did. But opening must be gradual, strategic, and sequenced, not a sudden flood that drowns local firms.

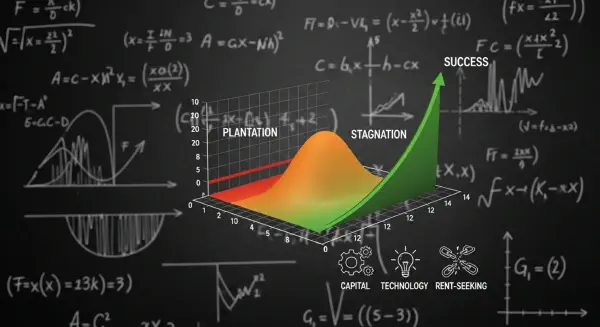

The narrow corridor between the plantation cliff and the capture cliff exists. Japan, Korea, and China walked it. Mexico and Malaysia fell off on either side.

Now, a new developing country can choose its path.

A Final Word on the Model and the Math#

We built a mathematical model, simulated three scenarios, and derived optimal control conditions. But do not mistake the map for the territory. Real countries are messier than any equation. Politics intervenes. Leaders change. Shocks happen.

The value of the model is not in its precise numbers. It is in the structure it reveals:

- Policy stringency and institutional quality are complementary. You cannot have one without the other.

- High initial rent‑seeking creates a trap that is very hard to escape. Prevention is far easier than cure.

- The optimal path is high‑then‑gradually‑down, not constant or low‑and‑slow.

Use the model as a thinking tool, not a oracle. Adjust parameters to your country’s reality. Run your own simulations. But never forget the human element: the engineers, the factory workers, the honest bureaucrats, the visionary politicians. They are the ones who actually build industries.

Equations describe. People act.

What Comes After This Series#

This is the final post of the series. But the conversation does not end here. If you are a policymaker, an economist, a business leader, or a student of development, I invite you to:

- Run the model with your own country’s data. The Python code is open source.

- Adapt the roadmap to your specific context. What works in a coastal nation with a large port may differ from a landlocked country.

- Share your experiences : successes, failures, and surprises. Industrial policy is not a solved problem. We learn by doing.

Thank you for reading. Now go build something that lasts.

Next post: “The United States as a Warning – When the Richest Country Behaves Like a Rent‑Seeking State. The final case study: how the US, with all its wealth and institutions, is now exhibiting signs of capture and stagnation in its own automotive industry – and what that means for the future of industrial policy globally.